Crypto & Forex

Is the US Dollar Losing Its Grip? GBP/USD Surges as Markets Signal a Surprising Shift—What Investors Need to Know Now!

Ever noticed how the GBP/USD pair can feel like that stubborn friend who bounces back…

Crypto & Forex

OpenSea’s SEA Token Launch Scrapped—Is This Market Meltdown a Canary in the Crypto Coal Mine?

So, here we are again—OpenSea's SEA token launch, a much-anticipated moment in crypto circles, gets…

Travel

How I Uncovered a Hidden Disney World Hack That Slashed $783 Off My Family Vacation—And How You Can Too

They call it "The Most Magical Place on Earth," but anyone who’s ever tried to…

Men's Lifestyle

Unlock the Power of These 12 Zip-Up Sweaters That Every True Menswear Champion Swears By—Are You Ready to Dominate Your Style Game?

Ever find yourself rummaging through endless racks of zip-up sweaters, wondering if any of them…

Women's Lifestyle

This Season’s Feather Trend on the Oscars Red Carpet Is About to Transform Your Wardrobe—Here’s How to Wear It Like a Pro

Ever noticed how some nights at the Oscars feel like stepping into a secret aviary,…

Men's Health

Unlock Your Best Spring Body Yet: The Secret Walmart Finds Fitness Gurus Swear By

Ever noticed how the start of a new season sparks that sudden urge to push…

Women's Health

Pope Leo’s Shocking Take on Cosmetic Surgery Sparks Fierce Debate Among Top Plastic Surgeons—What You Need to Know!

So here’s a curveball for you: the Vatican just dropped a 5-minute read that’s got…

WEALTH

How Stan Barnes’ Bold Move to Head Aviation Advisory at BDO Ireland Could Redefine the Industry’s Future—Are You Ready for the Shift?

When it comes to aviation finance, appointing the right leader isn’t just a routine shuffle—it's…

Men's Lifestyle

Unmasking the Secret Playbook: How Modern Millionaires Flex Their Wealth Across the Globe Like Champions

Ever wonder how the ultra-rich manage to keep their fortunes ticking across borders—and no, it’s…

Crypto & Forex

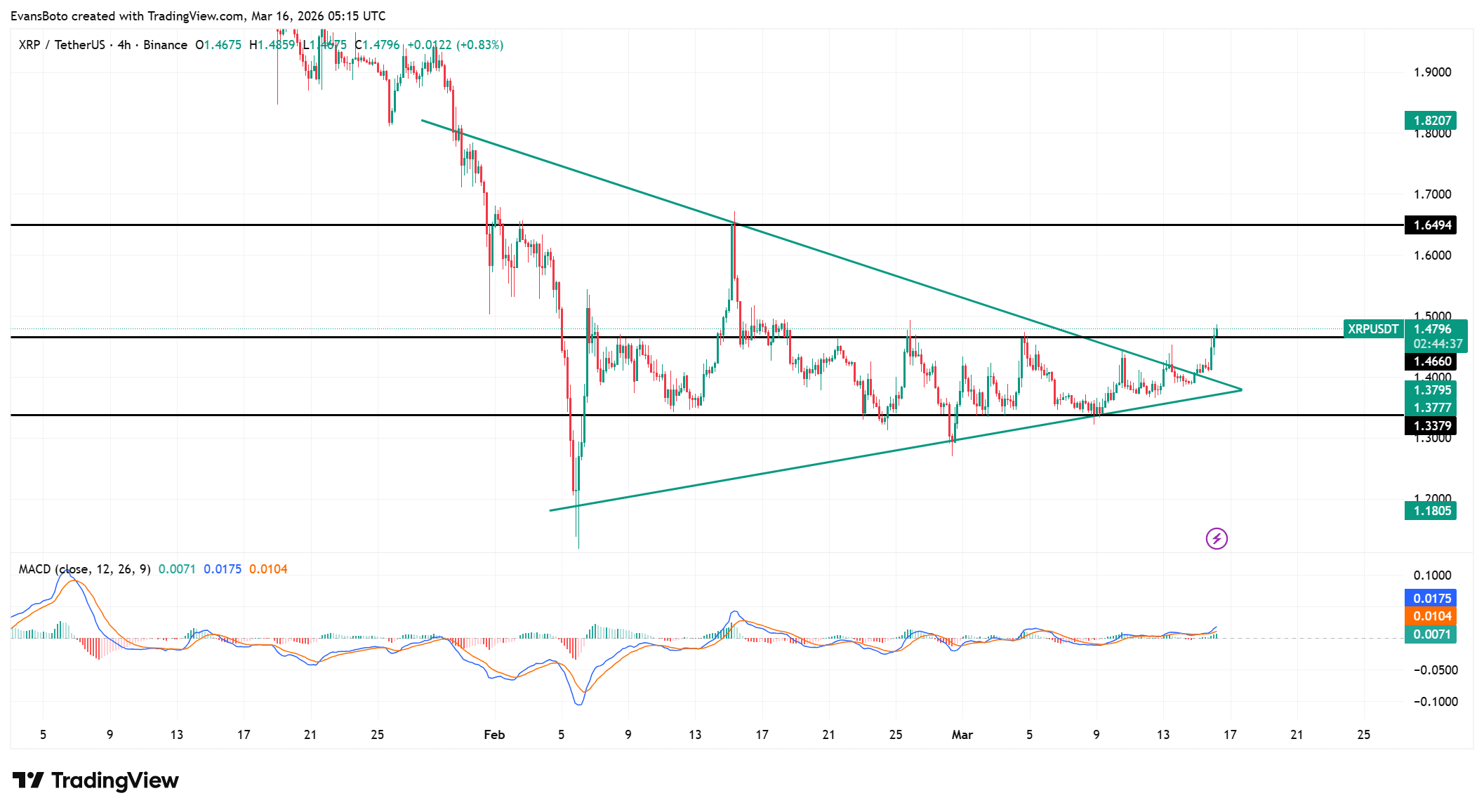

XRP Leverage Skyrockets 16%—Is $1.64 the Breakout Level That Will Ignite Massive Bull Profits?

Is XRP gearing up for a thrilling breakout, or is this just another blip in…