The Hidden Traps That Cause Universal Life Policies to Lapse—And How to Outsmart Them Before It’s Too Late

So, imagine this: you’ve just dumped a big wad of cash upfront into a universal life insurance policy, thinking you’ve sealed the deal, locked it in forever — no more payments, right? Yet somehow, months or years down the line, you hear the dreaded news: the policy’s lapsed. Wait… how does that happen when you’ve paid EVERYTHING in one go? Well, that’s the million-dollar question I got from a fellow Telegram member recently — and it’s a perplexer worth unpacking. Universal life policies aren’t just about the upfront cash; they’re like a relentless, ever-hungry kid demanding a growing allowance from your investment portfolio hidden inside the policy. If the investments stumble or if you’re pushing for too much coverage with too little premium — the “multiplier” game — this kid’s appetite might just outpace what you’ve put in, causing the policy to fizzle out before its time. In this deep dive, we’re unraveling the why’s and how’s — navigating through costs, charges, and age-related stealthy expenses that nibble away your policy’s value silently. Ready for an eye-opener? Let’s dive in and decode the curious case of universal life policies that can sleep with the fishes even after a fat premium payment. LEARN MORE

img#mv-trellis-img-1::before{padding-top:87.326732673267%; }img#mv-trellis-img-1{display:block;}img#mv-trellis-img-2::before{padding-top:40.625%; }img#mv-trellis-img-2{display:block;}img#mv-trellis-img-3::before{padding-top:89.6197327852%; }img#mv-trellis-img-3{display:block;}img#mv-trellis-img-4::before{padding-top:88.163265306122%; }img#mv-trellis-img-4{display:block;}

I was discussing privately with a Telegram group member who was telling me that he has this wish to buy a couple of universal life policy.

Somewhere in the conversation, he asked: “Why would the policy lapse if I have paid up all the premium in a single premium upfront?”

A universal life policy will lapse if the current value of the policy is insufficient to pay for the charges.

I don’t want to go into a full explanation of a universal life (let me know if you guys are interested though), but if I were to boil down to the main reasons it is:

- You push the multiplier too high. This means you try to pay very little initial premiums to get the max coverage.

- The underlying investments fail to perform long term.

It is a combination of these two reasons.

My reader asked a good question because all he sees is that the money is paid, but the best way to visualize a universal policy is like… your income portfolio to pay for your demanding kid.

The kid is the insurance company.

The income portfolio has to keep providing the kid allowance and yet it has to grow over time. If the kid is less demanding and ask for less money, your portfolio has significantly less stressful growth.

But the unique thing is that this kid will get more and more demanding as you age, and so it may start asking for more and more money if you are not careful.

The kid’s allowance if we go back to insurance are:

- The Policy Charge that will be deducted like $2.50 per $1000 sum assured for the first 10-18 years (depending on policy).

- The Fund Charge or Account charge that is ongoing that can be low or now 1% per year for the Indexed portion of the indexed universal life (if you only select 50% to be based on Indexed instruments then this cost is lower perhaps half)

- The Cost of Insurance which is the insurance coverage. This is based on the age. The older you are the more it cost.

- I could add in some internal fund fees. This likely show up as a reduction in returns.

So this is really like your retirement income planning. Does sequence of return matters? Yes it does but that is a story for another day.

Why Does the Coverage Will Potentially Kill the Universal Life Policy?

Let us use an example:

Suppose you are nearer to 57 years old and you wish to cover $5.8 million. This means that you buy this universal life, any time you passed away, there is a $5.8 million payout for the people you nominate for the policy. If no nomination, then this policy is available for your estate to which the executor of your estate would divide based on your will.

But based on the proposal, you only need to pay $1 million in a single premium or one time. In this thingy, the insurance company and the adviser would typically earn 6-7% of this premium which is paid by the insurance company to the advisory firm.

(Note: read the example for its meaning not the actual numbers. Your mileage may vary. I use $5.8 mil because my simulator defaults to that after not using for a while and likely this is for a policy that is much younger like 50 years old. So don’t go asking the person that sells you the policy why I put in $1 mil at 57 I can only get $4 mil coverage. )

The insurance company over time would extract the policy charge, fund charge, cost of insurance from the universal life policy. This takes place within the policy.

Now it looks like a good deal to pay $1 mil to cover $5.8 mil.

Some adviser even more hor seh will ask you to not pay $1 million but to leverage up. But that is the story for another day.

Now if you take $5.8 mil divide by $1 mil it is about 5.8 times and this is what I call the multiplier. It kind of shows you how explosive or “worth” it is the policy.

For little you can cover a lot to expand your estate. Put in $1 mil you have $5.8 mil to split between your two sons.

A very common selling point.

The Difference Between the $5.8 mil and $1 million is the Sum-at-Risk Insurance

If you take $5.8 mil – $1 mil = $4.8 mil this is roughly the insurance portion of the policy. Can say the $1 mil is the equity value. (I am diluting the details but usually if you put in $1 mil, the first day equity value is usually about 20% less but lets just go with this example)

The premiums, or the cost of insurance is extracted from that $1 million in equity policy value. If the cost is low then small amount is extracted. If the cost is high then a significant amount is extracted.

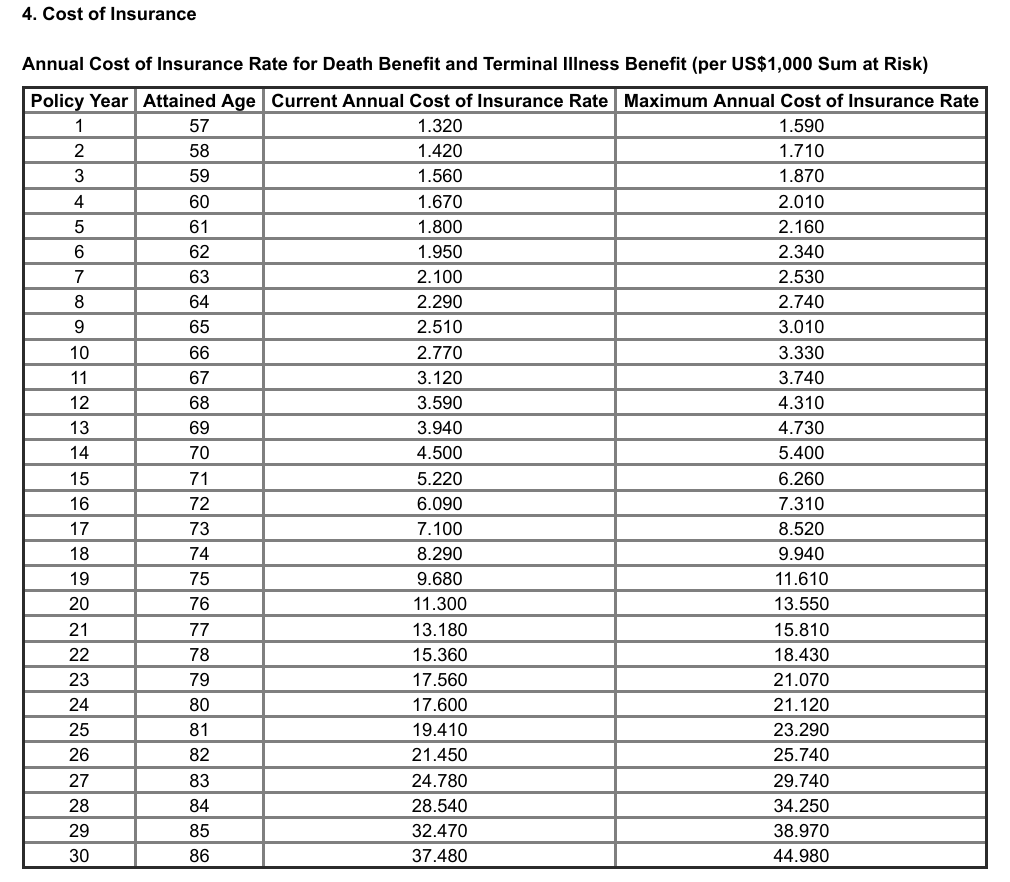

Let me bring out the cost of insurance table of one of Singlife Universal Life policy:

The cost you pay is based on the amount and your age. If your health is different there might be some loading on top of this.

So you can see for a 58 year old its $1.42 per US$1000 sum at risk insurance.

Since we say its $4.8 mil and we divide by 1000 its $4800 and times $1.42 we get $6,816. This $6816 will be deducted from the current policy value (now at $1 mil). That is about 0.68% of the equity portion.

Say at Age 83, the Policy Value Grows to $5.5 Million.

The policy invest in something and in recent years what is pretty popular are these fancy structured index products that tout 7% or 9% p.a. crediting rate.

The value of the $1 million should grow over time.

Lets say the equity value of that $1 million grows to $5.5 million.

The sum at risk then is $5.8 mil – $5.5 mil = $300k

Now if you read the table the 83 year old will be $24.78 per $1000. No longer $1.42!

So the annual cost of insurance premium is $300 x $24.78 = $7,434.

This looks big until you take this divide by the equity value of $5.5 mil and its 0.13%.

You don’t have a sequence of return risk there.

What if the Policy Value only Grows to $3 Million at Age 83?

The sum at risk then is $5.8 mil – $3 mil = $2.8 million.

This means the cost of insurance still needs to cover a significant amount.

So the annual cost of insurance premium is $2800 x $24.78 = $69,384.

If you take this divide by the equity value of $3 million, the current cost of insurance percentage is 2.3%

2.3% is still okay actually but you can actually see the burden if your policy does not appreciate its value successfully over time.

The Older the 83 Year old Gets (Without Dying), the More Burden/Stress it Places on the Policy if Investments Don’t do Well.

Since this cost of insurance is constantly extracted from the policy (unless the UL equity grows well above 5.8 mil in that case the sum-at-risk is zero and there is no cost of insurance) and this places stress.

If the policy gets to $3.5 mil at 90 years old, the cost of insurance premium is $137,379 for that year.

This ends up being 3.9% of the equity value.

I think in this illustration it should last till 100 but think you get the idea.

Visually Illustrating the Policy Growth and How Returns and Costs Affect the Policy.

Since I build some internal simulators, this may be how a policy will visually look like if you graph it out:

Let me try to explain what you are seeing.

Let’s start with the top chart labelled Policy Value and Sum-at-Risk. This is the policy that assures $5.8 million in the event the policy owner passes away. The premiums that you put in is $1 mil, but in this illustration the equity policy value starts below that due to the costs the insurance company takes out.

The yellow shaded area will show you the sum-at-risk or the amount of insurance that you are paying for. Notice that the yellow area ends near age 80.

What happen there?

The equity portion of your equity value grew well overtime such that by age 80/81, the difference between sum assured and policy value is less than zero. There is no insurance and therefore you do not have to pay for the insurance component any more.

Does that mean I won’t have to incur any of the high cost of insurance due to age then?

Yes.

I use a 50% equity and 50% fixed income portfolio return to illustrate, but you will drop the question “But Kyith, I cannot find a universal life policy with this kind of portfolio profile. Why are you showing me this?” Well, one answer is you also don’t know the portfolio allocation of the insurer that drives the traditional crediting rate (pretty opaque in Singapore if you ask me) and secondly, wouldn’t be you expect this kind of performance from your Indexed universal life at least?

This illustration shows a positive sequence out of many potential sequence, based on the historical data of the past. And for sure, it is only fair for me to show you a negative sequence later.

Now, let me explain the bottom panel.

The bottom panel shows the various costs that gets taken out from the policy monthly/annually. The green shaded area is the fund charge, and you can see it ongoing. This is an annualized 1% p.a. because we are assuming that for this policy its fully using a non-traditional return and thus a 1% fee is charged. The yellow sharded area is the policy expense, which is $2.5 per $1000 of sum assured. This runs for 15 years. Finally the red/brown shaded area shows the cost of insurance paid on the sum-at-risk insurance coverage.

You can observe the green is ongoing, but after 15 years, the policy expense goes away. The cost of insurance stops the moment the sum-at-risk goes to zero.

Now you would notice if we stack all 3 together, these costs work out to be about an annualized 3% of the Prevailing policy value. In this case it stays constant over time.

These costs are taken out from the policy but yet you can see this policy manage to grow its value over time.

This is what you positively expect.

How does a Negative Return Universal Life Insurance Sequence look like?

Out of all the historical 50% equity 50% fixed income sequence I picked one out not far from the years of success previously and we have this:

First thing you should notice is that the yellow and green shaded area stop at age 90. What happen?

The green shaded area or the policy value goes to zero.

The policy lapse lor so you don’t have coverage anymore.

So if you passed away after that only, your estate gets zero.

Before that the sum assured is $5.8 mil.

The bottom panel shows the costs.

Notice that the costs seem higher. If we stack them up its 4% of the prevailing policy value. How come not 3%? Policy drops in value, and never recovered.

Notice those cost percentage just goes up over time with it going crazy after 73 years old.

The red area or the cost of insurance became a real drag as the policy hold grows older.

But its not just the cost but the policy holder faced an unfortunate market return sequence.

These two sequence are the same policy but you can imagine them as different version of the same policy holder based on the luck they draw.

But Kyith Would the Downside Protection of an Indexed Universal Life Policy that Keeps Lowest Yearly Return to 0% Improve the Outcome?

The insurer assumes a certain crediting rate be it 7%, or 8% when crafting the projection of benefit and surrender value that you see.

You got to ask your adviser what is the basis of that 7% and 8%.

It is kind of interesting that for the same or different indexed S&P 500, different insurers would assume different crediting rates.

So are they using a median expected crediting rate returns projection or a more pessimistic crediting rate returns projection?

How long of a time period did they use to compute that crediting rate returns projection?

Whether there is 0% downside protection or not, traditional or indexed, there is a range of market returns that dictate the growth of your wealth and my wealth. Whether you buy a universal life policy or not.

Say it after me: There is a range of returns and therefore there is a range of outcome.

If there is only one outcome, if I am the insurer I will tell you this is a guarantee return already.

But why am I not telling you that?

Your outcome for every product, based around risk assts, is always a range!

Even with the put option bought within the indexed product, the returns are a range and your question is for this range is there some outcomes, in the range of outcome that would put pressure on the policy that will lapse the policy.

You can ask this to the person trying to sell your universal life and see what kind of creative answer the person gives you haha.

Kyith, Going by this Dynamics, Wouldn’t that Mean a Lower Crediting Rate Universal Life be Under More Pressure?

It depends.

If the crediting rate is lower, the insurer might assume that based on the underlying return dynamics, the returns is going to be lower.

The sum assured, relative to the initial premiums you pay is also lower, meaning the multiplier effect is more muted. But is the crediting rate actually safer and the range of future outcomes be smaller, relative to an indexed universal life?

It is possible.

In most of the underlying portfolio that I managed to suss out, they are pretty fixed income heavy and the range of outcomes is lesser.

But since they are more fixed income heavy, I felt the upside is also capped in a certain way.

A lower volatility return with a greater proportion of guaranteed crediting rate would ensure that the policy holder faced less negative sequence of return risks.

The indexed universal life policy tries to do the same (protect against seriously negative sequence of returns) by engineering downside protection via put options within the index product or dynamic asset allocation to reduce the allocation to high volatility risk assets when risks picks up.

But the most important thing is, those mumbo jumbo works well in theory, but how do they perform in real life execution? =)

How Can Make Your Universal Life Plan Safer?

I said the risks earlier:

- You push the multiplier too high. This means you try to pay very little initial premiums to get the max coverage.

- The underlying investments fail to perform long term.

You cannot control the market returns and your outcome in the future is a single draw, out of many possibilities that may mirror the many sequences in the past. This means you can’t control #2.

But you can actually control your sum assured and the premium you start with.

A couple of the costs is actually based on sum assured value:

- Policy expense or an equivalent name for your insurance plan. In the case of this Singlife Universal Life that I take reference from, this is $2.50 per $1000 sum assured and last for the first 15 years.

- The cost of insurance is based on the sum assured.

One of the big selling point is you put in $1 mil and you cover for $5.8 mil. Greatly expand your estate.

If your eventual return performs like the median, you get what you want but what if it falls short?

Uncertainty.

You can don’t go so crazy with the sum assured relative to the premiums.

- If your eventual returns is great or better than median: Your policy doesn’t lapse and policy value builds wealth.

- If your eventual returns are not great or worse than median: You placed less pressure on the policy in terms of the costs relative to policy value, and greatly improves the policy survivability.

You expose the universal life to higher expected returns but be conservative with your planning.

Kyith, What About Leverage?

What about it?

If you add leverage, you add one more component to the complexity then I don’t want to think liao.

But in effect you can think this way:

- If the next 40-50 years the interest rate environment results in lower than expected interest rates: Then good outcome lor.

- If the next 40-50 years the interest rate environment results in higher than expected interest rates: Your whole product + leverage under more stress lor.

Perhaps now you want me to predict the interest rate for the next 50 years and if so I will ask you first: You are a business man knowing your industry well and I want you to accurately tell me how the industry will be in 20 years time (not even 40/50). If you are wrong, you eat a bullet for me.

What will your answer be?

You probably get how ridiculous these things are but sometimes you will still ask this of me.

Epilogue – Hope the Person Selling You the Universal Life is Enlightening You Well.

Whether it is universal life or investments, what eats people alive is when the reality (when they live their lives) is so different from their expectations.

And the expectations of investment or products is set by themselves, driven by the sales process.

Usually, some understands the reality, felt the real worry only when they realize there can be potential downside or volatiltiy.

After 3,000 words this is not saying universal life is not useful or no place in your financial plan.

It’s more like with the right explanation you can see a more balanced view.

If you find yourself potentially interested in such products, and wish for clarity over how the product can help you, you might want to speak with the folks at Havend. You be able to discuss with them whether these universal life plan fits your needs and clarify some of the mumbo jumbo that I present today.

If you want to trade these stocks I mentioned, you can open an account with Interactive Brokers. Interactive Brokers is the leading low-cost and efficient broker I use and trust to invest & trade my holdings in Singapore, the United States, London Stock Exchange and Hong Kong Stock Exchange. They allow you to trade stocks, ETFs, options, futures, forex, bonds and funds worldwide from a single integrated account.

You can read more about my thoughts about Interactive Brokers in this Interactive Brokers Deep Dive Series, starting with how to create & fund your Interactive Brokers account easily.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Fee-only Wealth Advisory Firm Providend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith’s current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

Wall Charger, Surge Protector, QINLIANF 5 Outlet Extender with 4 USB Ports | 1680 Joules, 3-Sided Power Strip, Multi Plug Wall Outlet Adapter Spaced for Home Travel Office, White

$9.99 (as of August 7, 2026 02:59 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Milk-Bone Original Medium Dog Biscuits, 10 lb Box | 280+ treats, classic meaty taste, crunchy dog treats for dogs 20-50lbs, 15% protein, 12 vitamins & minerals, made in the USA

$14.97 (as of August 7, 2026 02:53 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

FlavCity Vanilla All in One Protein Shake Powder - On the Go Meal Alternative + Collagen Peptides, Reishi & Cordyceps - Focus, Skin, Hair & Joint Support - 100% Grass Fed Whey, 20 Servings

$59.99 (as of August 7, 2026 03:04 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

GHOST Energy Drink, Zero Sugars, 12-Pack, Welch's Grape, 16oz | Energy & Focus Pre Workout Drink, No Artificial Colors, Gluten-Free, Vegan - 200MG Natural Caffeine, L-Carnitine, Taurine

$29.99 (as of August 7, 2026 02:53 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Post Comment