Why Commodities Are Quietly Becoming the Ultimate Goldmine Amid Market Chaos—And What You Need to Do Now

Is it just me, or do the echoes of the 1970s seem to be blasting through our times again? Claudia Winkleman’s rockin’ those flares while the oil crisis shadows our horizon — feels like we’re queuing up for petrol and lighting candles any day now. But here’s the twist: while it’s a downright nightmare for ICE car owners and geopolitical hot spots, it’s turning into a turbocharged moment for commodities investors. Natural gas futures have shot up like a missile since conflict ignited, and broad commodities ETFs are quietly flying under the radar with solid gains. In a world where equities are scrambling for cover and inflation’s gnawing at your wallet, commodities are flexing their muscle as a strategic piece you might’ve overlooked. No, this isn’t some blind “commodities cheerleading” — it’s about recognizing real opportunities amid chaos, and why now might just be the time to dive back in or take a fresh look. Curious about the nitty-gritty behind these shifts and how to harness them in your portfolio? LEARN MORE

This was to be a Mavens member post explaining how commodities work in a portfolio and why that time is now. But given how fast events are moving, we’ve pulled it forward to give non-members a taste of what’s behind our paywall. Please do consider signing up for more!

Is it me or are the 1970s back? Apparently Claudia Winkleman was spotted in flares, plus there’s an oil crisis inbound. (You might have noticed?)

Personally I can’t wait to queue around the block for petrol and use candles for lighting again.

But while it’s a bad time to be the owner of an ICE car – or a leader of Iran – it’s an excellent time to be a commodities investor.

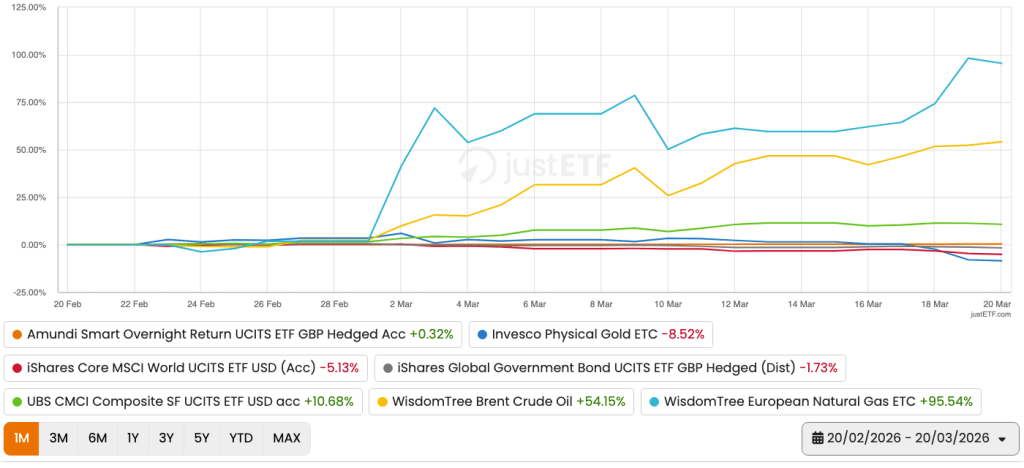

The vertical take-off vehicle in the chart below is the sight of a natural gas ETC going up like an interceptor, once the missiles started flying. See the light blue line:

Chart from justETF. March 2026. justETF charts show nominal total returns (GBP).

The gas futures tracker is 92% to the good since 2 March (the first day of trading after the war began).

It’s as if people think bombing gas fields is gonna put up the cost of energy or something.

Whizzing along at a slightly lower altitude is Wisdom Tree’s Brent Crude Oil ETC (yellow line, 54% gain).

Finally, UC15 – my fave broad commodities ETF – flies under the radar with an 11% gain (green line).

Run for cover

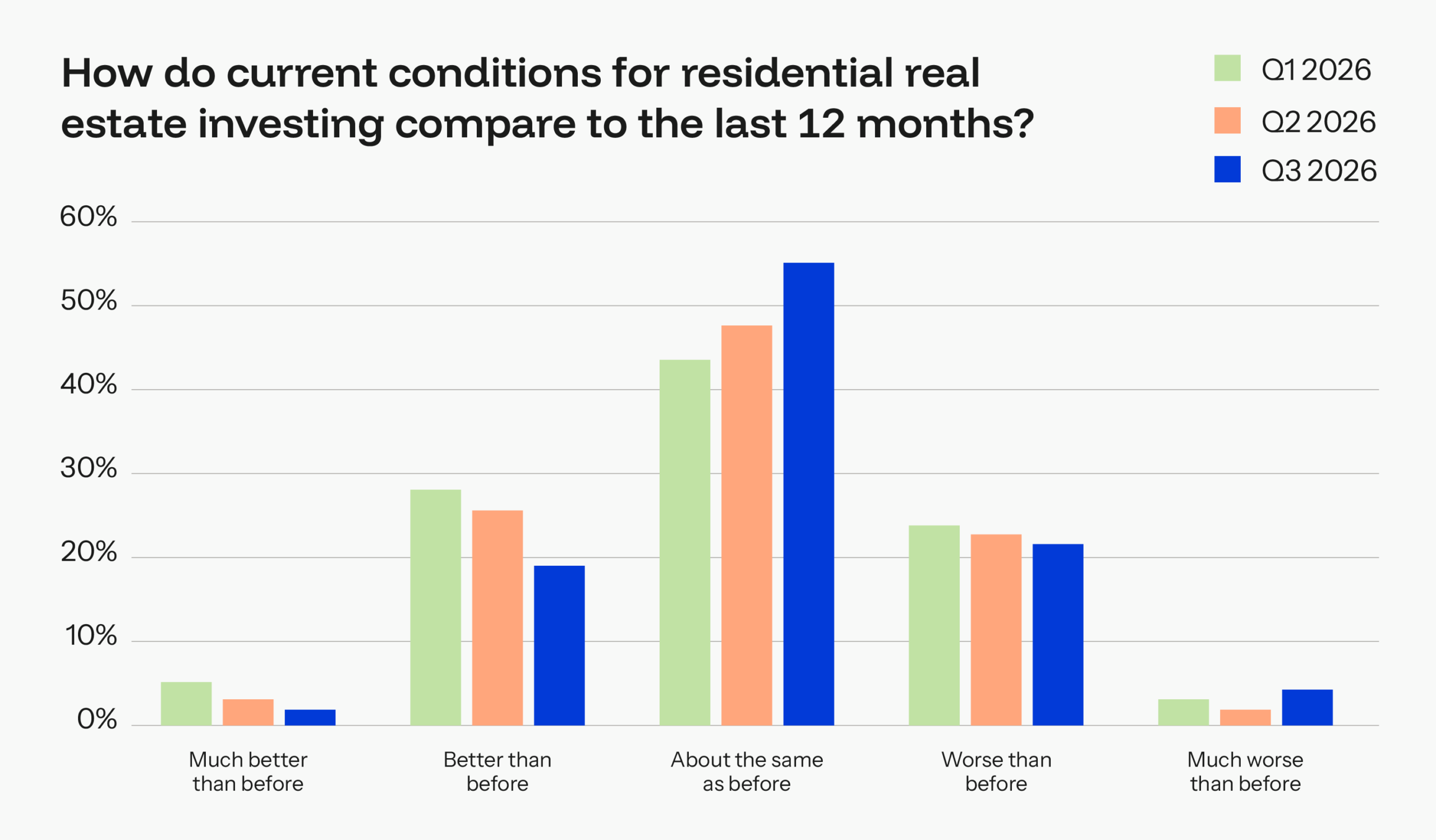

The next chart contrasts the response of equities, gold, bonds, money market, and commodities to the current crisis:

Yes, every other asset class is retreating like a Dubai-domiciled influencer bar docile cash (orange blip) and the aforementioned commodities (the investment that loves it when physical stuff gets scarce).

But don’t worry, this is not a “Commodities Ra-Ra!” post.

The point is that DIY investors are naturally sceptical about commodities. The asset class is sickeningly volatile and many recall how it fell into a doom spiral after the Global Financial Crisis.

Yet the counterpoint is that commodities are often upstanding – and sometimes outstanding – when other asset classes hide under the table.

Especially during the supply shock crises that wrack the world periodically. Which – unless Trump steps off his golden escalator soon – is exactly what the current contretemps could trigger.

Hopefully sanity will prevail. But it can take a while before the hard-of-sanity see sense.

That’s why commodities deserve another look. Especially given how other assets struggle to cope with highly inflationary conditions. Gold may perform but it’s a highly unreliable bedfellow (as its current 12% drop-off since 2 March is currently reminding us…)

Commodities: the good, the bad, and the downright ugly

I’m not a stooge in the pocket of ‘Big Raw Materials’ who pay me in bushels of wheat for every new convert. Honest!

What follows is intended as a relatively quick and digestible account of the reasons why you might want to hold commodities as a strategic diversifier. It includes reasons why you might skip it as well.

Just so you know where I’m coming from, I don’t advocate dipping in and out of Brent Crude ETCs depending on how histrionic Pete Hegseth appears today.

However, I do hold a broad commodities ETF (Ticker: UC15) as a portfolio diversifier and bulwark against inflationary shocks.

BCOM again

Now, about that commodities bear market…

The commodities index I benchmark against (BCOM) has still not recovered the market high it achieved in June 2008.

From that perspective, the asset class has spent almost 18 years underwater! That’s absolutely hideous if you were sucked in by the Noughties’ run-up in commodities. (An ascent often attributed to the rapid growth of China and other emerging economies at the time.)

However commodities look perfectly respectable from other starting points.

For instance, here’s the annualised returns over the past ten years for the main asset class ETFs I charted earlier in the article:

| Asset class | 10-yr annualised return (%) |

| Gold | 14.6 |

| World equities | 12.9 |

| Broad commodities | 10.1 |

| Money market | 2 |

| Global government bonds | 0.3 |

Nominal annualised total returns (GBP) from justETF, 20 March 2016-20 March 2026. I’ve replaced iShares Global Government Bond ETF (IGLH) with XGSG because IGLH does not have a ten year track record. Both are GBP hedged.

On this view, commodities don’t look so bad. In fact, they’ve done extraordinarily well during a period in which gold and equities have been blinding.

Moreover, they’ve produced a great result for a diversifying asset. There’s not much point holding raw materials to deflect rogue waves of inflation if it’s a deadweight the rest of the time.

(Reminder: for real returns, subtract average UK inflation of about 3.5% for the period.)

Commodities for the long run

The long-term real return of broad commodities stacks up nicely, too:

Data from AQR , Summerhaven , BCOM TR, MSCI, Before the Cult of Equity , A Century of UK Economic Trends , Robert Shiller, The Big Bang , Bank of England, and ONS. March 2026. Monevator sourced returns in this article are inflation-adjusted annualised total returns (GBP).

World equities index – Pre-1970 World equities monthly returns are not available in the public domain. To facilitate long-term comparisons, I’ve used market-cap weighted UK and US monthly returns to stand in for World equities from 1900 to 1970. The MSCI World equities index covers the period from 1970 until the present day. The UK / US market cap varied from approximately 55% to 84% of World equities up to 1970.

The long-run view shows that commodities are not a basket case. Indeed, their average return is more than fine (and compares favourably with other defensive diversifiers):

- Broad commodities (blue line in chart above): 4.6% annualised real total return (GBP)

- World equities (red line): 5.9% annualised real total return (GBP)

My chart annotations spotlight commodities’ handy habit of peaking when inflation runs amok. Unsurprisingly really, because they’re the feedstock of the price index itself.

As such, the historical record shows that raw materials are the asset class most likely to beat inflation when it’s eating your purchasing power alive.

Two caveats though.

Firstly there are some enormous bears lurking in the commodities return undergrowth. We’ll wince at those shortly.

Secondly, the chart’s biggest commodity booms are associated with the early Twentieth Century industrialisation of the US (see 1900 to 1909 on the chart) and the double-hit of post-war inflation and reconstruction (1945 to 1950).

If you don’t think the transition to a decarbonised economy built around the electric tech stack will have quite the same impact, then we should discount commodities’ long-run average growth rate.

For example, fund manager Research Affiliates’ offers 3.1% as its 10-year real expected GBP return for commodities.

Either way, on balance I think it’s reasonable to believe commodities can make a positive contribution to the growth of a diversified portfolio.

Material gain

For my money, the real win isn’t the future return of commodities. It’s the damage limitation role they can play when equity performance is grim.

The next chart contrasts World equities and commodities returns during the biggest stock market routs of the past 126 years:

On average, commodities outperformed equities by 46.1% per bear. Remember that’s an inflation-adjusted return, too.

As you can see, commodities didn’t always produce a positive return. However, they did deliver a better return than equities. Every time.

The table below offers a quick summary of the action above:

Diversification score card

| Equity bear market performance | World equities | Commodities |

| Positive return | 0 | 4 |

| Better negative return | 0 | 5 |

| Best overall return | 0 | 9 |

Pretty compelling, eh? The table is telling us that commodities always improved portfolio performance when investors desperately needed a life belt to cling onto.

Indeed I think I should write up a post repeating this score card for the other key portfolio diversifiers available to us – and that can also be tested against a diverse range of economic conditions. Namely, cash / money market funds, government bonds, and gold.

Without checking, however, I bet the others will struggle to do as well as commodities. Simply because runaway inflation is the spark most likely to torch UK investors’ portfolios.

This is at odds with the US downside experience, which is dominated by demand-led recessions like the Great Depression.

That’s partly why commodities have been given short shrift. They don’t thrive when demand collapses.

You can see in the chart above that the clamour for copper and cows evaporates during Big League liquidity crises. Witness commodities’ negative returns booked against the Global Financial Crisis, the Japanese asset bubble implosion, and the slump-daddy of them all, the Great Depression.

Thankfully, government bonds usually ride to the rescue during those times of darkness.

But commodities were deemed unnecessary when DIY investing took off because memories of rampant inflation had faded. And Americans hadn’t suffered purchasing power cuts on the scale that scarred previous generations of Brits either.

Totally oresome

The next chart gives you the gory details on how often commodities have stepped up when equities have fallen down:

The red ravines represent the occasions that equities fell from their previous high – including the death plunges we saw in the previous chart.

The icy peaks show the subsequent rolling one-year commodity real returns.

Blue swells that rise above the 0% line show commodities actively counterbalancing equity drops with a positive return over the next 12-months.

But if the blue line tunnels down, then it exacerbates the situation if it bores through the red floor.

Otherwise, negative commodity returns reduce the drag factor so long as the blue losses don’t exceed the red.

The higher and more frequently the blue waves rise above the red depths, the better.

Once again, this is a sterling result, but the chart also warns us that commodities don’t always hedge your losses.

The hard stuff

As grizzled commodities investors know, this is an asset class that can batter you with devastating combos of negative returns.

The next chart retells the commodities growth story, but it highlights the warts ‘n’ all:

Obviously the angry red areas are the down years – or decades.

Not so bad? Not so fast!

The chart is based off softie nominal prices, because that best represents our lived experience as investors.

However, the next chart shows the real deal – because it’s inflation-adjusted returns that put food on the table:

Oh my! This is the ugly I mentioned earlier.

By this light, the history of commodities returns is dominated by nearly four double lost-decades.

In other words, commodities sunk deep underwater for around 80 of the last 126 years. So there’s that.

Shovel it

If the boom and bust nature of commodities puts you off for life, I don’t blame you.

Reader, I invested. Not because I love pain but because commodities can bulk up when equities and bonds wane.

My target asset allocation is 10%. However I only bought 5% initially, my plan being to take advantage of raw materials’ inherent volatility in the future.

That is:

- I’ll buy more when my commodity ETF plummets.

- I’ll sell when the ETF’s price rockets.

Hopefully that rebalancing schedule will enable me to turn a profit on my commodities exposure. Or at least recover more rapidly when the next equities’ bear strikes.

Super psyched

Incidentally, the mighty leg-ups on the commodities’ growth chart led to the development of the commodities ‘super-cycle’ theory.

The theory posits that commodities go on a tear during periodic transformations of the world economy. Whereas the subsequent slumps are the product of over-investment in solving commodity bottlenecks.

If that pattern holds then we’re still on the upswing from the depths of the last commodities’ depression. It began when easy money dried up during the Global Financial Crisis.

It’s a macroeconomic story arc that could help explain the excellent 10-year returns we saw for commodities earlier, and Research Affiliates’ chipper 10-year expected returns forecast too.

But what matters to me is that there’s something in my portfolio that reacts to inflation like Popeye on spinach.

When that happens I’ll sell up and buy breathing space for my equities to recover.

Take it steady,

The Accumulator

P.S. For more on commodities, check out our five-part series:

P.P.S. “What follows is intended as a relatively quick and digestible account…” Yes, I failed. Again.

INABA Churu Cat Treats, Lickable, Squeezable Creamy Purée Cat Treat with Green Tea Extract & Taurine, 0.5 Ounces Each Tube, 50 Tubes, Tuna & Chicken Variety

(as of July 15, 2026 02:41 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Amazon Fire TV Stick 4K Select (newest model), start streaming in 4K, AI-powered search, and free & live TV, find shows faster with Alexa+

(as of July 15, 2026 02:54 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Cat Deterrent Spray 2 Pack, Natural Non-Toxic Plant Based Anti-Scratch & Anti-Marking Spray for Cats & Kittens, Orange Scent Pet Training Aid, Safe for Pets, Indoor Outdoor Furniture, Protector 7.0 Oz

(as of July 15, 2026 02:50 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

TP-Link Tapo 1080P Indoor Security Camera for Baby Monitor, Dog Camera w/Motion Detection, 2-Way Audio Siren, Night Vision, Cloud & SD Card Storage, Works w/Alexa & Google Home (Tapo C100)

(as of July 15, 2026 02:51 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Post Comment