Why Investor Confidence Is Crashing Right Now—and What It Means for Your Portfolio

When it feels like the tides of the market are turning more gray than gold, what’s a savvy investor to do? As we cruise deeper into Q2 of 2026, retail investors are facing a stark reality check—their sunrise hopes for better market conditions are dimming faster than a candle in a storm. Yet, here’s the kicker: despite wavering optimism, many aren’t packing up just yet. Instead, they’re doubling down on strategy, poised to capitalize on a buyer’s market that’s flexing some serious muscle nationwide. It’s kind of like expecting the roller coaster to slow down… only to realize it’s just gearing up for another wild loop. With geopolitical unrest and AI shaking the labor market, sentiment has taken a hit, but the hunger to grow and optimize portfolios remains fierce. So, is this just another chapter of feeling the squeeze, or the calm before an investor’s renaissance? Dive into the latest insights from BiggerPockets’ Q2 2026 Investor Pulse Survey and see where the smart money’s headed next. LEARN MORE

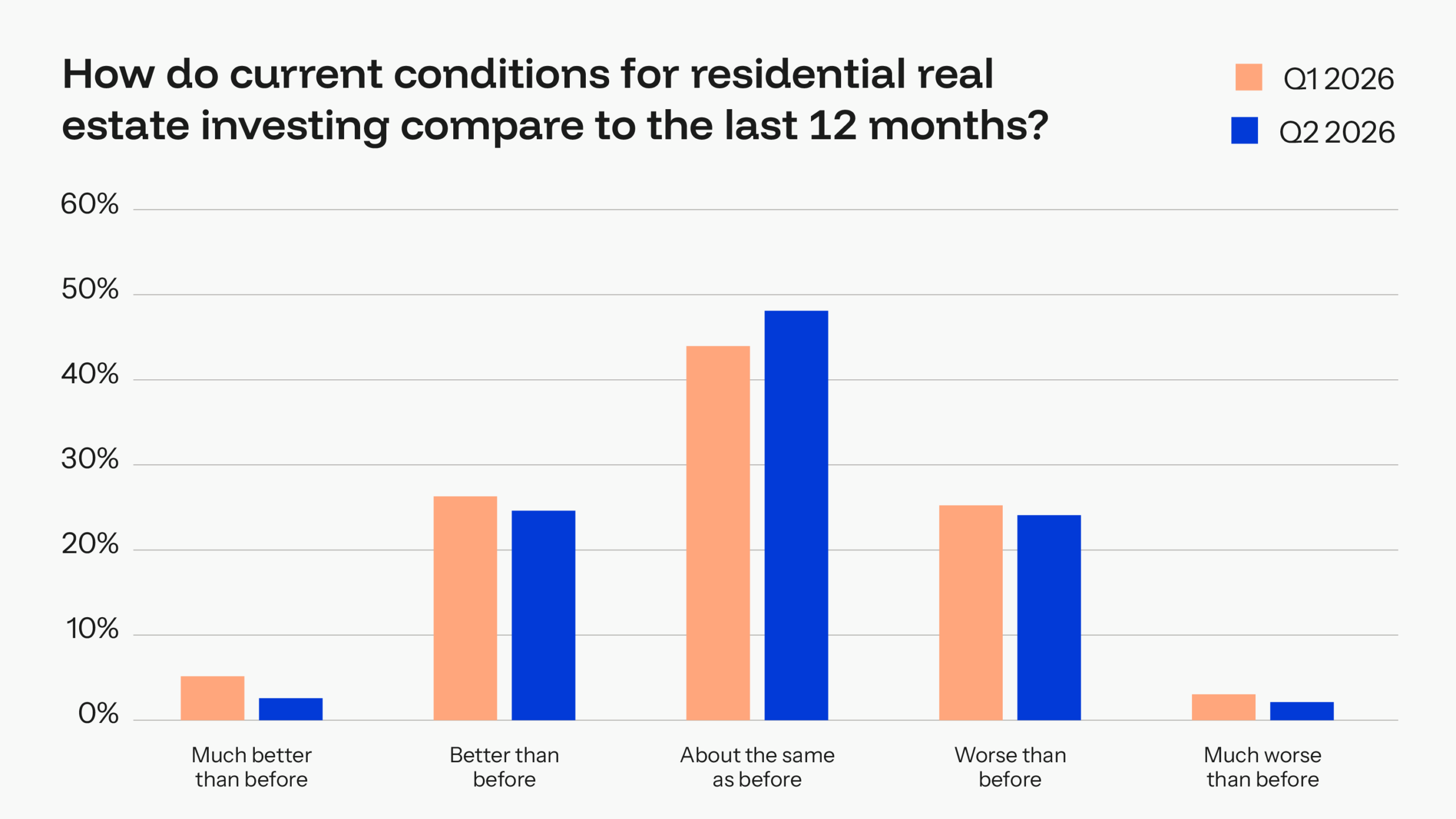

Retail investors’ hopes for improved market conditions are fading in the second quarter of 2026, but many investors still plan to actively grow their portfolios in an increasingly strong buyer’s market, according to BiggerPockets’ Q2 2026 Investor Pulse Survey.

At the start of 2026, investor optimism for improving investment conditions was high, as moderating mortgage rates, improved affordability, and stronger inventory trends suggested a modest rebound was in order. Now, three months into the year, much of that optimism has faded as the war in Iran has pushed up inflation and bond yields, taking mortgage rates up with them.

Investors, however, remain focused on growth and on taking advantage of the improved deal flow and negotiating leverage that come with the buyer’s market now characterizing the national housing market. Investors don’t see conditions deteriorating; rather, they expect conditions similar to those of the last several years. In essence, they’re expecting more of the same.

Investor Sentiment

Current investor sentiment has declined modestly in recent months, with our Pulse Index for the last 12 months dropping to 102—down from 109 in the previous quarter (100 is neutral, and anything over 100 is positive). The stability of the index over the last three months makes sense, given that the start of the year closely resembled the slow, low-affordability market we’ve been in for the last several years.

Despite the noise, conditions on the ground haven’t changed that much.

However, when asked about the prospects of improving conditions, investors are notably less optimistic than they were just three months ago.

Our forward-looking Pulse Index, which asks investors about their expectations for investing conditions over the next 12 months, dropped considerably from 150 in Q1 to 112 in Q2.

This decline in sentiment is primarily driven by fears about AI’s impact on the labor market and the war in Iran, as investors hold deeply negative views on how the conflict will affect the housing market.

While the war’s impacts on housing are yet to be fully realized, investors appear to have two concerns. First is the direct impact that war and geopolitical uncertainty has on housing demand. Overall, people tend to shy away from large financial decisions during periods of uncertainty). Secondly, and perhaps more acutely, is the impact the war has already had on inflation and the subsequent rise in mortgage rates which have risen about 0.4% since the war started, as of this writing.

From the war’s start and March’s inflation jump (the Consumer Price Index rose from 2.4% in February to 3.3% year over year in March), investor expectations for mortgage rate relief have fallen considerably. Last quarter, the majority of investors believed rates would hover between 5.5% and 5.99%. This quarter, the prevailing prediction is for rates to remain between 6% and 6.49%.

The downgraded expectations for mortgage relief are likely the primary cause of the overall decline in sentiment. Last quarter, investors said the biggest opportunity in 2026 would be a decline in mortgage rates. Now, investors see better negotiating leverage, better deal flow, and falling prices as bigger opportunities.

On top of the uncertainty the war brings, investors are also concerned about how AI could disrupt the labor market and the potential for lower overall housing demand.

As of now, the labor market is actually holding up fairly well. Labor market data is notoriously imperfect, but at a 4.3% unemployment rate, the labor market is showing resilience.

The big picture, however, remains unclear. Hiring rates are in concerning territory, and lower quit rates suggest that employers and employees are feeling nervous about the labor environment—a sentiment reflected by retail investors as well.

Despite the challenges of higher rates and high uncertainty, investor sentiment remains neutral rather than negative.

Portfolio Allocation

Surveyed investors still largely intend to grow their portfolios in the coming year, while many are aiming to focus on optimization.

Almost no investors are planning to reduce their holdings.

Investors identify the best opportunities to grow in regional hot spots in the Midwest and Southeast.

Tried-and-true strategies like long-term rentals and owner-occupied approaches (house hacking or live-in flips) remain areas of optimism.

Investor sentiment aligns quite well with historical evidence of what works during periods of slow home sales and low affordability. Long-term strategies in markets with strong fundamentals can and do provide strong returns, even with higher mortgage rates.

Final Thoughts

Although sentiment for improving market conditions has waned in recent months, investors remain committed to growing and optimizing their portfolios in 2026. Even with increasing geopolitical and labor uncertainty and stubbornly high mortgage rates, conditions haven’t actually changed much in recent months. We still see low affordability and transaction volume.

But there are many positive developments as well. Deal flow is improving, and negotiating leverage is strong in buyers’ favor in most regions of the country. Higher-quality assets are coming to market. While we’re still in a transition phase for the market, the effects of these benefits are likely to hit the market increasingly in the coming months and could turn investor sentiment positive once again.

How does the general sentiment of the BiggerPockets community stack up to your own feelings? Let us know in the comments section.

About the Survey

BiggerPockets is a community of retail real estate investors, with over 3 million members, who in aggregate make up the largest bloc of residential property investors in the United States. The BiggerPockets Pulse is a quarterly survey that measures and shares the sentiment and intended behavior of this important economic force.

This BiggerPockets Pulse Survey collected 234 responses from active real estate investors between April 1st and April 10th, 2026.

Dr. Elsey's Ultra UnScented Clumping Clay Cat Litter 40 lb. Bag

(as of June 24, 2026 02:33 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

DoHonest Baby Car Camera HD 1080P - Rear-Facing Car Baby Monitor with Night Vision, Adjustable View Angle, Easy Setup, Anti-Glare Display, Safety for Kids & Infants

$25.48 (as of June 24, 2026 02:54 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Lance Sandwich Crackers, Variety Pack, 3 Flavors, 20 Individually Wrapped Packs, 6 Sandwiches Each

$7.64 (as of June 24, 2026 02:50 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Smiry Dog Door Mat for Muddy Paws 30x20, Absorbent Dirt Trapper, Non-Slip Washable Chenille Entryway Rug for Inside Floor, Grey, Classic Solid

(as of June 24, 2026 02:43 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Post Comment