Crypto Tax Nightmare or Opportunity? Kraken Sounds Alarm as 75% of Forms Fall Under $50—Could a ‘De Minimis’ Rule Change Everything?

Ever wonder if the IRS really needs a microscopic play-by-play of every tiny crypto move you make? Kraken sure does — and they’re not shy about calling out the current crypto tax reporting frenzy as a massive headache. Picture this: out of a staggering 56 million crypto tax forms filed, three-quarters detailed transfers of less than $50 — and half of those were below $10. That’s like sending a detailed tax diary for your morning coffee purchase! While other payment apps like Venmo only report transactions over $600, the IRS expects crypto brokers to spill the beans on every little shift, no matter how insignificant. Kraken’s bold shoutout? It’s time for a “de minimis exemption” — think of it as a much-needed cut-off point that spares users and the IRS alike from drowning in paperwork over nickels and dimes. But here’s the catch: turning this tax dream into reality hits roadblocks tough enough to make even the most seasoned entrepreneur grimace. Why is meaningful crypto tax relief playing hard to get? Let’s dive in and unpack what’s holding back this potentially game-changing reform. LEARN MORE

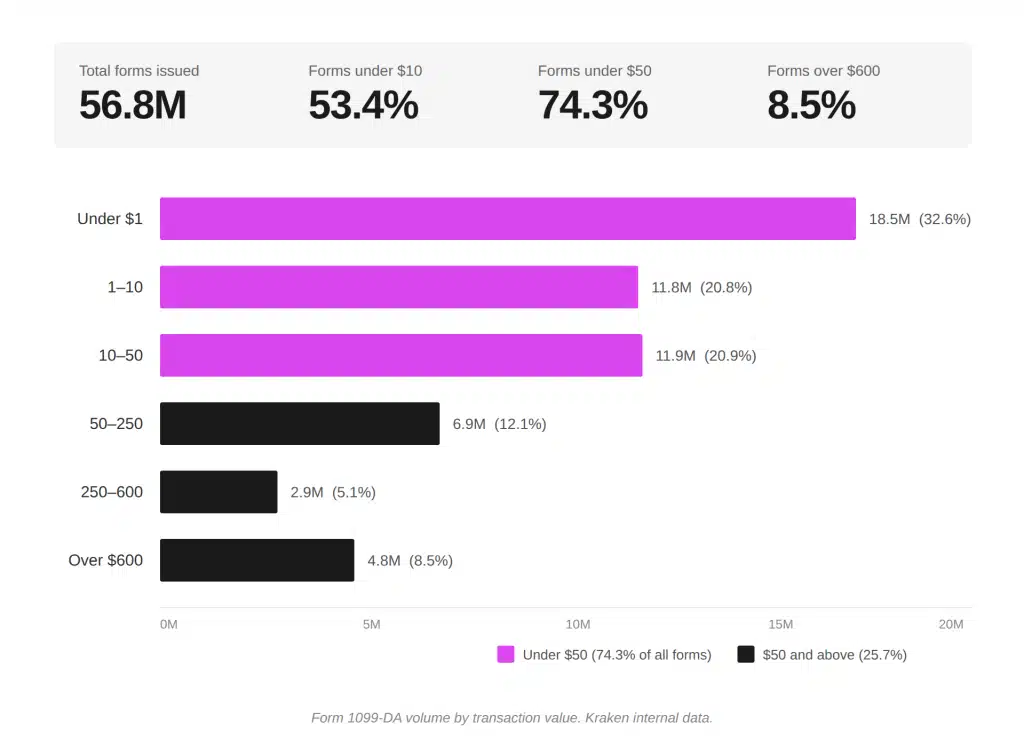

Kraken has decried the current overwhelming crypto tax reporting regime and urged regulators to grant waivers for smaller transfers.

In a report on the 22nd of April, the crypto exchange said 75% of the massive 56 million crypto tax forms submitted to the tax watchdog, IRS, were less than $50. And half (28 million) of the forms were less than $10.

The U.S. Internal Revenue Service (IRS) mandates brokers to submit every single transaction for the entire year as part of the current crypto tax reporting regime. On the contrary, other payment apps like Venmo only trigger reporting if the transfers are above $600, Kraken noted.

The firm decried that the current tax reporting regime is too expensive and complex for crypto users and brokers. At the same time, reporting such small values is not beneficial to the regulator. To fix this, Kraken proposed,

A meaningful de minimis threshold, indexed to inflation and paired with anti-abuse guardrails, would eliminate millions of unnecessary forms while protecting revenue integrity.

‘De minimis exemption’ refers to waivers for small transfers from the typical capital gains tax reporting. Unfortunately, such tax relief seems a little unattainable at the moment.

Why crypto tax relief could remain elusive

For starters, the current tax exemption being pushed only covers payment stablecoins and not other crypto assets such as Bitcoin [BTC]. Whereas, for stablecoins, lawmakers are pushing to have anything below $200 exempted from tax.

However, with a reported behind-the-scenes push to exclude others’ assets, comprehensive tax relief for the sector could remain elusive.

Besides, the said tax proposals need to be tied to the crypto market structure bill, the CLARITY Act. Unfortunately, the bill’s markup has also faced several hurdles to advance. Now the chances of being pushed to 2027 are likely if the May deadline is missed.

If so, the stalled crypto bill will also push the proposed crypto tax waiver for small transfers to 2027. In fact, prediction site Kalshi also reinforced a similar outlook.

As of writing, the chance of U.S. President Donald Trump eliminating capital gains on crypto this year stood at 7%. On the other hand, the chance of CLARITY passage this year was at 46%.

Collectively, these data sets showed the market was pessimistic about such a tax exemption for small crypto transfers this year.

Final Summary

- Kraken calls for a ‘de minimis’ tax exemption, as 75% of its 56 million crypto tax forms overload is below $50 to warrant the reporting burden.

- The crypto tax relief push could be elusive in the near term amid the limited scope of current proposals and slow CLARITY Act progress

Essentia Ionized Alkaline Water, 9.5 Ph Until Opened, 99.9% Pure, Bottled Water, 12Pk

$19.94 (as of August 4, 2026 02:52 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

SUPERDANNY Extension Cord,Flat Plug Surge Protector Power Strip,10Ft | 8 AC & 4 USB Ports (2 USB C),Surge Protector with 1050J,Desk Charging Station for Home Office,College Dorm Room Essentials

$14.99 (as of August 4, 2026 02:58 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Nature's Recipe Wet Dog Food Variety Pack, 2.75 oz Cup, 12 Count (2 Pack)

$28.67 (as of August 4, 2026 02:58 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

UP URARA PUP Spring and Summer Dog Collar with Bow Tie, Cherry Bowtie Collar Adjustable for Girl Boy Dog, Spring Pink Bow Collar for Dogs, S

$15.99 (as of August 4, 2026 02:58 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Post Comment