The Wealth Tax Trap: Why Some Strategies Bleed Your Bottom Line While Others Skyrocket Your Gains

Ever wonder why taxing the ultra-wealthy feels a bit like trying to catch smoke with your bare hands? Nick Maggiulli, COO of Ritholtz Wealth Management, dives deep into this perplexing issue in his eye-opening post, “Why Taxing the Wealthy is Harder than It Looks.” The crux? Wealthy individuals aren’t just sitting ducks; they’re nimble, savvy, and yes, extremely mobile. You slap a tax on their riches, and—poof—they might just shift it elsewhere, slipping through the cracks of legislation. It’s not just about the numbers; it’s a strategic chess game between governments and the rich, complicated further by historical attempts across the globe where wealth taxes either flopped or backfired. This article peels back the layers of wealth taxation—exploring its challenges, the fate of such taxes in various countries, and glimpses of what successful models look like. Ready to unravel why the richest keep dodging the taxman and what that means for your wallet and the future of fiscal policies worldwide? Let’s dig in. LEARN MORE

img#mv-trellis-img-1::before{padding-top:126.52482269504%; }img#mv-trellis-img-1{display:block;}img#mv-trellis-img-2::before{padding-top:24.043715846995%; }img#mv-trellis-img-2{display:block;}

Nick Maggiulli, the COO of Ritholtz Wealth Management and blog Of Dollars and Data has a pretty informative post Why Taxing the Wealthy is Harder than it Looks.

And the reason is because most of the rich is more mobile! If you tax them, then they would evaluate and move the money.

My personal thoughts is that there are more considerations. But anyway.

We are discussing wealth taxes here which means the more wealth you build, the more you get taxed.

Recently California proposed a one-time 5% wealth tax on billionaires, Washington state proposed a 9.9% tax on income above $1 million (taking effect in 2028), and NYC’s proposed surcharge on second homes worth over $5 million. When the US income tax was first introduced in 1913, the top 1% paid an effective rate of under 15%, it took over 30 years to exceed 40%.

There are many countries who tries to implement wealth taxes but eventually not many of them keep it.

As of 1990, 12 countries had net wealth taxes, but by 2017 only four OECD countries still levied them. Most repealed their wealth taxes because they weren’t effective at raising revenue and led to some capital flight.

Some countries that stopped:

- Austria – Repealed in 1994

- Denmark – Repealed in 1997

- Germany – Repealed in 1997

- Netherlands – Repealed in 2001

- Finland – Repealed in 2006

- Iceland – Repealed in 2006. Temporary reinstated the wealth taxes after GFC for emergency fiscal measure.

- Luxembourg – Repealed in 2006

The main reasons:

- Administrative complexity

- Capital flight

- Revenue fell short of expectations

- Difficulty valuing illiquid assets like private businesses and art.

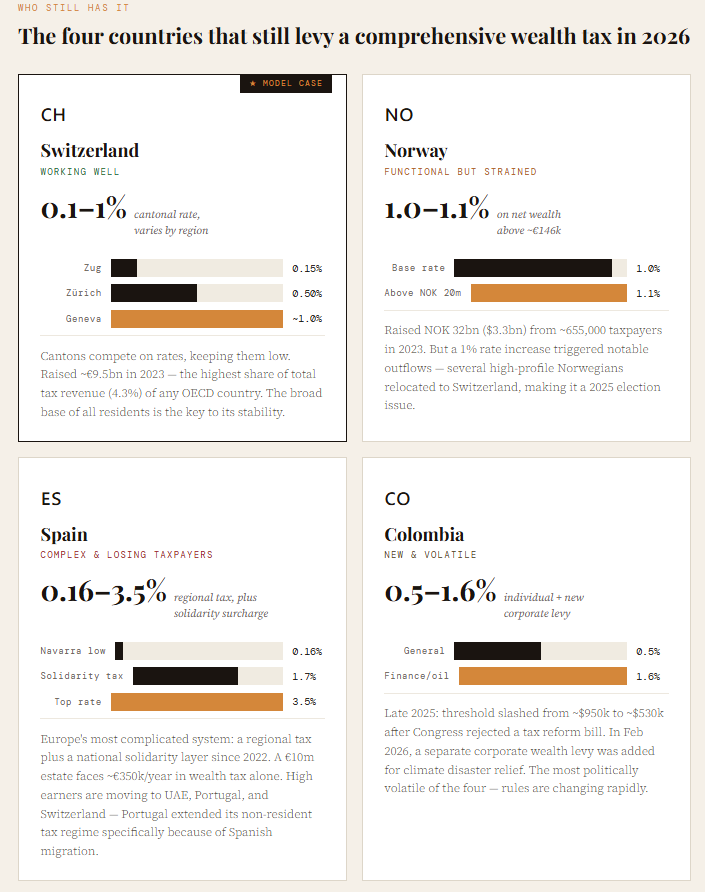

The 4 countries that still have it:

- Norway – Norway levies 1% on net wealth above NOK 1.7 million (roughly €146,000), with 0.7% going to municipalities and 0.3% to the central government. For wealth above NOK 20 million, the rate rises to 1.1%. Norway raised about NOK 32 billion ($3.3 billion) from roughly 655,000 taxpayers in 2023. However it’s not without friction — after a 1% increase in Norway’s wealth tax, many high-net-worth individuals left the country. Several high-profile Norwegians relocated to Switzerland, which attracted domestic media coverage and became a point of contention in the 2025 election cycle.

- Spain – Spain’s system is by some distance the most complicated in Europe. It operates on two overlapping levels: a regional net wealth tax and, since 2022, a national solidarity wealth tax. The regional tax is progressive, with rates from 0.16% to 3.5% on net assets exceeding €700,000. The solidarity tax then kicks in on top for those with wealth above €3 million. As an example, someone with €10 million in net wealth faces a solidarity wealth tax bill of €350,000 per year — on top of income and capital gains taxes — which has been a significant driver of emigration to the UAE, Portugal, or Switzerland. After Spain introduced the solidarity wealth tax, Portugal extended its tax regime for non-residents specifically because more Spanish taxpayers were considering changing their tax residence.

- Switzerland – Switzerland’s wealth tax is set at the cantonal level, with rates ranging from 0.1% to 1% depending on which of the 26 cantons you live in. This decentralisation is actually a feature. The cantons compete to attract wealthy residents with lower rates, keeping the tax reasonable. Despite its low headline rates, Switzerland’s broad base generates substantial revenue — roughly €9.5 billion in 2023, representing 4.3% of total tax revenue, the highest share of any OECD country.

- Colombia – Colombia’s wealth tax underwent a dramatic escalation at the end of 2025. After Congress struck down a proposed tax reform bill, President Gustavo Petro’s government declared an economic emergency and issued a decree slashing the wealth tax threshold from the equivalent of roughly $950,000 to about $530,000 — significantly expanding the taxpayer base to an estimated 102,000 individuals. On top of that, in early 2026 Colombia added a temporary corporate wealth tax of 0.5% (1.6% for financial, coal, and oil companies) on corporations with net equity above $2.9 million, to raise funds in response to climate-related events. Colombia is very much a work in progress, and the political instability around it makes it the most unpredictable of the four.

The Elements that Makes Some Taxes More Successful

The key pattern in successful policies is:

- Start with a small tax then grow it over time.

- Apply broadly on your base not just a small group.

Switzerland has a wealth tax ranging from 0.1% to 0.7% across its 26 cantons that has been successful. It works because it has low, predictable rates applied to a broad base of individuals, rather than a higher rate on a narrow group.

Research analyzing over 45 million US tax records from 1999–2011 found that the millionaire migration rate was just 2.4%, lower than the overall population migration rate of 2.9%. When modelling identical tax rates across all states, elite migration fell by only about 2%. This suggests most wealthy people are embedded in their communities and won’t move unless a policy is extreme.

NYC’s pied-à-terre tax is flagged as a likely success.

It’s an annual surcharge on second homes in New York City valued at $5 million or more, where the owner’s primary residence is outside NYC’s five boroughs. It targets non-residents specifically. If you are a full-time NYC resident, you are not affected regardless of how many properties they own in the city. Think of it as a tax on the Boston executive who keeps a Manhattan apartment for work trips, or an overseas investor with a Midtown condo sitting empty most of the year.

One-to-three family homes valued above $5 million face surcharge rates ranging from 0.8% to 1.3% depending on property value. For co-ops and condos with assessed values between $1 million and $3 million, a 4% surcharge would apply. The final rate structure hasn’t been locked in yet but likely based on a similar 2019 proposal, a sliding scale is the most likely structure, with properties between $5–6 million potentially subject to 0.5% annually, scaling up from there.

This tax is modest and applies to over 13,000 units, giving it the broad base and reasonable size that tends to work. Washington’s millionaires tax is seen as having a better chance than California’s precisely because it covers a much wider group of earners.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

If you’re thinking of opening an Interactive Brokers account, my referral link is here.

As the new account holder, you’ll receive USD 1 in IBKR stock for every USD 100 you deposit, up to USD 1,000 in shares — so a USD 10,000 deposit gets you USD 100 in IBKR stock, and the bonus is capped at USD 1,000 for deposits of USD 100,000 or more. A few other things to know: the minimum deposit to qualify is USD 10,000, done within 30 days of opening, and the bonus shares are locked up for one year from the award date. The promotion is currently active, and using the link costs you nothing extra. On a separate note, if you haven’t already, it’s worth taking a look at how IBKR’s share price has performed over the past five years — the stock you receive as a bonus isn’t just a token; it’s a stake in a company that has done quite well for its shareholders.

I break down my resources according to these topics:

- All my personal notes about how my philosophy behind my own money and how I manage it.

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I work and do research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Fee-only Wealth Advisory Firm Providend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith’s current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

Monster Vision 2 | Portable Entertainment System with 15.6" 1080p Display & 60W Speakers | up to 25 Hours of Playtime | Dual HDMI Ports | Includes USB-C to HDMI Cable | ATSC Tuner for Portable TV use

$249.99 (as of July 9, 2026 03:06 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Syruvia Sugar Free Coffee Syrup, Cookie Butter Flavored Syrup for Drinks, Lattes, and Desserts – 25.4 fl oz

(as of July 9, 2026 02:57 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Samsung Galaxy Buds 4 Pro (2026) AI True Wireless Bluetooth Earbuds, Hi-Res Audio, 2-Way Speaker, ANC 2.0, Optimized Comfort, IP57, Live Translation, Black [US Version, 2 Yr Warranty]

(as of July 9, 2026 02:59 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Amazon Kindle Paperwhite 16GB (newest model) – 20% faster, with new 7" glare-free display and weeks of battery life – Black

(as of July 9, 2026 02:53 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Post Comment