Why Most Portfolios Fail Miserably (And How My Friend’s Nearly Broke the Mold)

Ever caught yourself frozen over the “factor vs no factor” investing debate, tossing and turning about whether to plunge more cash into factor-based ETFs or just stick to plain ol’ index funds? Yeah, me too. Here’s the kicker—what if all that agonizing ends with you earning less than you hoped, or worse, watching your money chug along at a frustratingly mediocre pace for 20 or 30 years? The reality is, no one can predict those dreaded worst-case decades, not even the best of financial minds. That’s why, instead of sweating the small stuff, we gotta zoom out and focus on the “big rocks” — the solid financial planning and realistic expectations that keep your goals afloat even when returns don’t dazzle. And yes, those factor premiums? They do show up, but it’s crucial to get comfortable and, more importantly, convicted enough to commit significantly—not timidly dabble—in your strategy. Curious how to group your portfolio, tame your fears about REITs, and actually make sense of all these investment pieces? Stick around, because we’re going to unpack the real deal on building a diversified, goal-driven portfolio that stands the test of time (and market mood swings). LEARN MORE

img#mv-trellis-img-1::before{padding-top:66.6015625%; }img#mv-trellis-img-1{display:block;}img#mv-trellis-img-2::before{padding-top:38.671875%; }img#mv-trellis-img-2{display:block;}img#mv-trellis-img-3::before{padding-top:39.2578125%; }img#mv-trellis-img-3{display:block;}img#mv-trellis-img-4::before{padding-top:24.043715846995%; }img#mv-trellis-img-4{display:block;}

This post is financial advise lol. Just putting it out here for his benefit so that its easier.

I have a friend who reads this post and we were discussing shifting away from investing in unit trusts or ETFs that is based on factors.

I explain to him that he can do that. He can always have both Dimensional based unit trust and systematic index tracking funds together. Just look at them as a whole.

I have good confidence that over 20-30 years these factor premiums will show up but even with good confidence can it turn out otherwise? It is possible as well! You can also invest for 15 years and fixed income returns turn out to be better than equities even if I have good confidence in equity returns.

We prioritize the financial or wealth planning part because for the goals that is more important, we want to be more conservative and allocate more capital to them. We just trust our Dimensional or index based implementation. If we happen to be so unlucky that we end up to be the worst or near worst 10% in history, then at least we can reach closer to our goals despite returns not being so good.

Cannot help one right? You ask others they also cannot predict you have the worst fxxking 20-30 years right?

The more important thing is to focus on the big rocks. So what are the big rocks?

I took a look at the returns of the Dimensional Global Core Equity Research Index and the MSCI World Index and this is the median returns for 15 years:

- MSCI World: 9.2% p.a.

- Global Core Equity Research index: 11.0% p.a.

For 20 years:

- MSCI World: 8.9% p.a.

- Global Core Equity Research index: 10.8% p.a.

Now say for example, we are either unlucky or that the factor premiums actually made it worse.

Instead of a +2% its a -1.5% versus the MSCI World.

So my friends actual return for the factor based portfolio is:

- 15 years: 7.7% p.a.

- 20 years: 7.4% p.a.

So you made a choice… and it didn’t work out, and your money grow at this rate (after maybe the expense ratio not factor in).

Are you going to cry father and cry mother?

It will be more shitty that you keep deliberating over factor no factor and then you only put in 20% of your money instead of a more significant portion.

How do you get comfortable and convicted enough to expose a more significant sum of your money to the equity factor is the big rock here.

And don’t tell me factors didn’t show up. It is what factors.

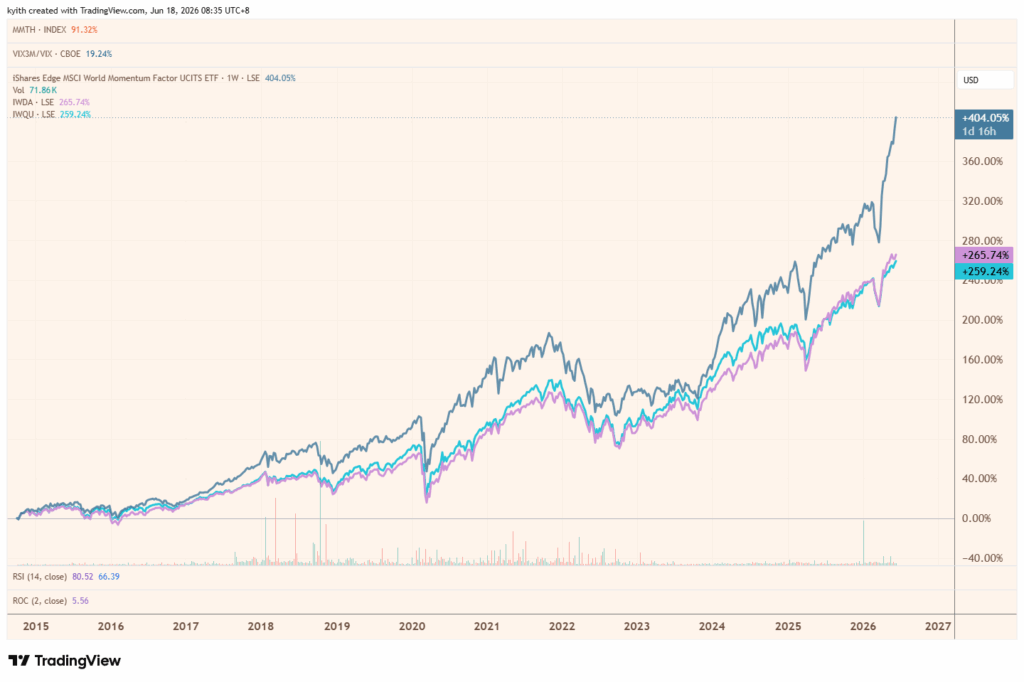

I overlaid the MSCI World ETF (pink) since 2015 with the MSCI Quality (light blue cyan) and the MSCI Momentum (dark blue).

You can see the momentum is clearly higher. But you can see that for the longest time, quality have been doing better than MSCI World.

11 years is a short time but you can’t say the factors are not showing.

On Real Estate Investment Trust

My friend has also been trying to focus on building a passive income portfolio which has banks and also REITs.

Of course REITs has not been doing well recently. But you got to think about it: There will be periods where things aren’t doing well. The industrial companies that is currently boom town Charlie building out data centers weren’t doing well as well right? Same for the Seagate and Western Digital. Would you have bought them when they are languishing?

The challenge is always when you try to recognize how they can get better when they are so shit.

But not many people show long term data on REITs. Since we have REIT data from 1989 till today, I can make use of Gilgamesh to show some.

S&P Global REIT USD from 1989 to 2025 Rolling Annualized Return:

S&P Asia Pacific REIT USD from 1989 to 2025 Rolling Annualized Return:

I think you can see that if you invest 10-years, you can get a “Xia Xia Cian” or be unlucky and earn 2% p.a. or 1.2% p.a. And that might be what some experience.

But you can see the 20-year return in the worst is pretty alright.

How Should You Group Your Portfolio Together?

My friend shared that when he asked Chat GPT if his passive income portfolio is good or how can it be better, the LLM tells him that it is heavy on REITs and he needs to diversify.

And can consider the stocks like SGX and ST Engineering.

Then I am like….

I think he should review how does he group all these bunch of shit. He has a factor based portfolio, now an index portfolio, then got these individual stocks.

What is each for? Or should he look at them together? or Separate? and How Separate?

If you put all of them together it is pretty diversified. An MSCI World alone is like 1600 stocks across a few geographical region. The Dimensional is like KNN more than 10,000 securities.

You tell me you add them its not diversification? Probably isn’t if the REITs will still make up more than 50% if we view them as a whole.

He is going to have income from work and the dividends coming in, and he would have to consider how to deploy it.

But more importantly, I think we should all consider: What is it that we wish to achieve?

Is it a portfolio for financial security/financial independence? To provide passive income when you need to turn on the tap? If so how much do you wish for this pool?

How much is more meant for children’s needs next time?

I think looking at portfolios based on goals is cleaner but that’s me.

I kind of think that folks who are into passive income cannot relate how these index funds, factor funds give passive income. So they look at them separately.

That’s usually a mental barrier.

And they have to overcome that.

Perhaps my friend can visualize it this way: Imagine his REIT and banks stuff he runs it as a fund. And at this moment, the fund choose to reinvest the dividends paid out.

Is he going to tell me this fund cannot provide income? He is managing it and there are dividends received internally. So what’s so different if it is an ETF managed by others?

I think if he has accumulated to $150,000, using rule of thumb rates based on the Safe Withdrawal Rate of 3% or 4% can help him visualize how much conservative annual income he can get on a recurring basis if he chooses to turn on the tap. That would be $4,500 and $6,000 respectively.

It might also open his mind to be more focus. And focus is always a good thing because it may build conviction.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

If you’re thinking of opening an Interactive Brokers account, my referral link is here.

As the new account holder, you’ll receive USD 1 in IBKR stock for every USD 100 you deposit, up to USD 1,000 in shares — so a USD 10,000 deposit gets you USD 100 in IBKR stock, and the bonus is capped at USD 1,000 for deposits of USD 100,000 or more. A few other things to know: the minimum deposit to qualify is USD 10,000, done within 30 days of opening, and the bonus shares are locked up for one year from the award date. The promotion is currently active, and using the link costs you nothing extra. On a separate note, if you haven’t already, it’s worth taking a look at how IBKR’s share price has performed over the past five years — the stock you receive as a bonus isn’t just a token; it’s a stake in a company that has done quite well for its shareholders.

I break down my resources according to these topics:

- All my personal notes about how my philosophy behind my own money and how I manage it.

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I work and do research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Fee-only Wealth Advisory Firm Providend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith’s current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

WOOF Pupsicle Peanut Butter & Beef Refill Pops Dog Treats, Large, 7 Count | For large Pupsicles, peanut butter & beef flavor, long-lasting treats, pre-made Pops, wholesome ingredients, shelf stable

$14.99 (as of August 5, 2026 02:52 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Pringles Potato Crisps Chips, Lunch Snacks, Snack Cups, Variety Pack, 19.5oz Box (27 Cups)

$13.98 (as of August 5, 2026 03:03 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Acer OHW328 Kids Headphones Wired for School - Over Ear Design | 85/94dB Safe Volume, 3.5mm Jack Foldable Headphones for Kids Boys Girls Classroom Yoto Player Chromebook Travel Black Red

$13.99 (as of August 5, 2026 03:06 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Delectables Squeeze Up Variety Pack, Creamy Squeezable Puree, Lickable Wet Cat Treats, Grain Free, No Added Fillers, No By-Products, No Added Preservatives, 0.5 Ounces Tube, 24 Tubes Total

$14.26 (as of August 5, 2026 02:52 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Post Comment