Why I’m Telling My Friend to Reconsider Fundsmith Equity Fund—And What That Means for Your Portfolio Today

Ever had that feeling when you watch a friend’s investment steadily chug along, looking pretty solid, only to suddenly see it stumble and wonder—what just happened? That’s exactly the conundrum my buddy faces with the FundSmith Equity Fund. For years, the returns looked pretty reasonable, like a reliable engine ticking away under the hood. But in the first five months of this year, their USD returns dipped into the negative zone—around -2.5% to -3%. Makes you ask: Is FundSmith’s famed “quality investing” philosophy hitting a rough patch or is the market playing tricks on us?

This isn’t my first rodeo with this fund; I’ve dissected it multiple times already. Yet, there’s something about FundSmith that keeps pulling me back—maybe it’s the sheer volume of questions it stirs up or the mental real estate it occupies for many investors and advisors alike. The question isn’t just about performance though. It’s about understanding the layers beneath the headlines. How should one properly assess FundSmith’s numbers, especially when currency shifts and concentrated stock picks blur the clarity?

Stick around as we peel back those layers—exploring why FundSmith dominates conversations in financial circles, the intricacies of its recent track record compared to peers, and the real story behind those year-to-date figures that’ve left some scratching their heads. Spoiler alert: Investing in just 25 quality stocks means the ride can get wild—with highs and lows more pronounced than the standard market fare.

So, ready to challenge your assumptions about what “quality investing” really means in today’s market? Let’s dive in.

img#mv-trellis-img-1::before{padding-top:65.008291873964%; }img#mv-trellis-img-1{display:block;}img#mv-trellis-img-2::before{padding-top:30.17578125%; }img#mv-trellis-img-2{display:block;}img#mv-trellis-img-3::before{padding-top:64.0625%; }img#mv-trellis-img-3{display:block;}img#mv-trellis-img-4::before{padding-top:109.75348338692%; }img#mv-trellis-img-4{display:block;}img#mv-trellis-img-5::before{padding-top:26.46484375%; }img#mv-trellis-img-5{display:block;}img#mv-trellis-img-6::before{padding-top:49.4140625%; }img#mv-trellis-img-6{display:block;}img#mv-trellis-img-7::before{padding-top:53.515625%; }img#mv-trellis-img-7{display:block;}img#mv-trellis-img-8::before{padding-top:43.84765625%; }img#mv-trellis-img-8{display:block;}img#mv-trellis-img-9::before{padding-top:53.61328125%; }img#mv-trellis-img-9{display:block;}img#mv-trellis-img-10::before{padding-top:24.043715846995%; }img#mv-trellis-img-10{display:block;}

I got a friend who I know invested in FundSmith Equity Fund for a few years. Optically, the returns have been livable for a few years.

And then, the returns becomes… optically not so livable.

This year, the year to date return in USD terms (I did an estimation) is -2.5% to -3.0% over the first 5 months.

I reviewed FundSmith a few times and you can read them here:

This post might also be the fourth post on this so I don’t want to delve into it too much. But I would like to cover a few areas.

Why FundSmith’s Funds Take up Some of My Mental Headspace

In the past, many financial planners like to sell Investment Linked Policies specifically on FundSmith’s funds.

I remember there was a potential prospect that was reviewing coming on with one of my client adviser colleague, but also 2 other financial planners outside.

The main recommendations, aside from the advise/commission structure, is advice in an ILP through FundSmith’s fund.

Deep into a part of the discussion, I remember him saying: “After speaking to a few different people, advisers, many of them bring up FundSmith’s fund. Investing in FundSmith’s fund should be pretty correct.”

Well the argumentative Kyith would tell him a lot of us can be wrong together more often than you think.

And so because we get soooooooooooooo much questions about FundSmith, then of course we have part of our mental space with it.

Be Careful How you Assess FundSmith’s Performance

I think people need to consider carefully how they look at the performance.

If you see a poor number and you compare wrongly, you may have snook yourself into thinking the performance is poor when there is a reason for it.

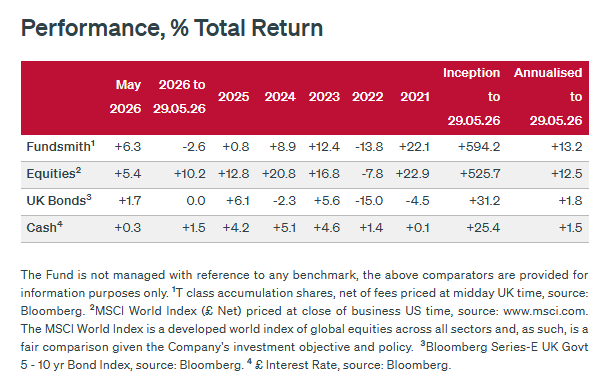

What you see on FundSmith’s website is the return reported for their T class of shares, which is in GBP:

Most index or fund returns are in USD so you would need to make conversions. for example, Equities in that table is the MSCI World. The MSCI World in USD was 21.6% in 2025, 19.2% in 2024, 24.4% in 2023. This should tell you that you kind of need to adjust things a little.

FundSmith’s Last 1.5 Years Return Was Objectively Not Good

Terry Smith’s investment strategy is to curate high quality companies and don’t change so much. He is basically investing in the quality factor and if we know that, we can compare against similar indexes and funds that are also quality based.

I have updated FundSmith’s performance, convert them to USD based roughly, and put them side by side against some other quality funds and indexes:

Perhaps some introduction is in order. I can benchmark and compare Fundsmith with a few factor indexes that systematically selects companies that exhibit quality characteristics such as low debt to equity, debt to assets, high return on equity, high return on assets, consistent earnings. There are also systematic indexes that selects companies that have higher profitability such as (operating earnings – interest expense) divide by book value, or 5-years of consistent dividend raises.

There are funds or ETFs that are available to you that you can invest in.

So here is what is presented:

- MSCI USA Sector Neutral Quality Index – IUQA via IBKR

- MSCI World Sector Neutral Quality Index – IWQU via IBKR

- GMO Quality Investment Fund – Fund via Endowus

- DFA US Hi Relative Profitability Index – Mutual Fund not available to Singaporeans

- Dimensional Global Large Cap High Profitability Index – Research Index not available.

- WisdomTree US Quality Dividend Growth UCITS ETF – DGRA via IBKR

- WisdomTree Global Quality Dividend Growth UCITS ETF – GGRA via IBKR

Out of all this, GGRA is in Daedalus Income Fund as a strategic holding. I have GMO Quality Investment Fund in the money my father left my brother and me.

FundSmith after adjusting for currency did 8.7% in 2025. Actually if you see the 2025 performance of the MSCI World quality index, Dimensional US Hi Relative Profitability Index, and WisdomTree US Quality dividend growth, they are not too different. FundSmith is objectively poorer but they are around the same ball park.

The MSCI World did 21% in 2025 and you can see none of the Quality factor related funds or indexes did better than the blended capitalization-weighted index.

But I think it is the year to date performance of 2026 that really fxxk investors up because it’s negative while you can see the rest isn’t the best but they are positive at least 5% for the GMO Quality Investment Fund and GGRA, and FundSmith’s fund is -3%.

Since some of our my colleagues are reading here is the Dimensional Global Core, MSCI World related performance:

What I will Share With My Friend

I think people shrink from personal advice but my friend is in the advice field and he should know what he is doing. If he is coming to me with this, he wishes for a more trusted, independent perspective on this.

Terry Smith has shown consistency in his investment philosophy. But philosophy is one thing and how you implement and execute that philosophy is another.

You have to know that you are investing in a fund with a human manager trying to curate and pick a concentrated portfolio of securities (fund owns only 25 securities). The fund’s performance will be based on the manager’s selection.

But the “big rocks” here is that its only 25 securities and investing in the quality factor.

If the quality factor continue to outperformance or keep up with market cap weighted index, then FundSmith’s fund will do well if Terry’s execution is well.

If Terry’s picks happen to not have home runs in the short or intermediate period, or have more of those that potentially look like they are going to be disrupted then they are going to suck lor.

The table of performance I have shown over this period shows you that:

- Terry’s performance meanders around a known factor.

- That he would perform exceptionally well or poorly.

Concentration will result in wildly good or poor outcome.

And more often those with poor outcome don’t survive to tell the story. So we only hear the good outcomes.

The very fact that my own pick in my strategic systematic portfolio is not doing as well should tell you I expected things like this to happen.

Your returns is based on a basket of securities that you own, driving the returns.

There is going to be a time when some factors show damn shitty returns versus the blended capitalization weighted index like an MSCI World.

The MVOL or Ishares Edge MSCI Australia Minimum Volatility ETF is freaking 0% YTD and 10.5% in 2025.

At the end of the day, my friend has invested for 8 years in the FundSmith fund.

His total return if lump sum is 85% or 8% p.a.

He invested in an active fund. It could be far worse. Take the win. The most important is stay invested.

The fund could underperform for the next 10 years and he would still build decent wealth. It is just that we cannot control these things.

If I were him, I would personally try to take the human element out of the execution decision.

There are limitations what he can switch to in an ILP wrapper. I have not taken a look at the other offerings available to him, but I would rather him be in something that I know better than something that you have no fxxking idea how they drive the returns.

I Give Props to Terry Smith for Trying to do Things the Right Way

I can tell you i said very often one of the value that a Roboadviser bring to their clients is to humanize or improve the communication between the funds and their clients.

There are a lot of funds with good…. and also poor performance that you have no idea WHY their returns good or bad.

Terry Smith not only puts out his philosophy, he recorded two of these Shareholders Meeting to take questions and answer the fund’s investors.

FundSmith Annual Shareholders’ Meeting Feb 2026

Don’t you fxxking tell me you don’t have time to watch this if you are interested in the fund or have invested in it. I fxxking watch this not because I am interested but because I want to see so I don’t miss any communication with my friend.

Some tell me it is hard to grow or maintain a fund and that may be true. But just like people you meet, you also don’t want everyone to be your friend or that… only some you end up closer with.

But for those that you want to attract, you also want them to hear from you truly right? So how do we do that? By communicating right?

I think a lot of funds don’t do that because they don’t really care who you are. They just want your money.

Funds or AUM also the same.

It takes time communicating, and it is a cost expense, but its whether you want to build up something more sturdy.

This activity log from Dataroma of the fund kind of shows two things:

- There seems to be some serious buy and sell and does that go against his buy and don’t sell often perspective.

- Or that there are some massive redemptions that requires these selling.

I watched his video and these are some points worth noting.

In his own words, he says the fund’s performance was POOR. Part of the presentation is not to give excuses but to explain from their perspective why the performance has been poor.

Terry explains that the performance of the S&P 500 and MSCI World index is more and more concentrated. This means a few stocks drive a significant portion of the index performance.

If you pick stocks, you can be very lucky (just my post of the value funds just happen to have Micron!) or that you can easily missed out the stocks that eventually drive returns.

Many think that they can fore-pick what will eventually perform well.

Many think that what will eventually perform well are always the bluest chip of companies.

The data does not show that. The better performers eventually are not the bluest chip or it is difficult to predict.

Terry also explain that more and more of the investments are into passive index funds rather than actively managed fund. He argues that this has made the more inelastic.

I have written and commentate on this in the past so this is not so surprising.

One of the by product of this is that the movement in the index price performance might be very very small, but underneath this, the price performance can be crazy.

This chart basically shows some of their holding’s one day movement.

This is what we call Dispersion.

The movement can be wild.

Terry has some interesting metrics presented that many managers will not present but I like it.

If you tell people that you are owning quality business in a concentrated way, and don’t change so much, then you better show me that the portfolio of business is more higher quality.

And these metrics are the traditional metrics to assess if a company is high quality enough. You can see that his stable of company have better quality-related metrics.

High quality companies are… not cheap. At best you hope to buy them at fair value. But high quality companies are able to produce cash flow over longer period and able to grow them. In this slide, Terry shows us the free cash flow profile of their fund versus the S&P 500 over time.

The FCF yield tends to be higher. And their FCF growth is suppose to be higher.

This should also make you ask: Do you agree with this quality investing philosophy? Do you think that there are numbers-evidence of investing in more quality companies overtime?

Because if you don’t, or don’t know, you have a bigger problem because you invested in something that you have very little clue about. So what else have you invest that you have very little clue about.

Colorful Comments on FundSmith on X

It is not me seeking it out, but I get pushed about Terry Smith’s struggle quite a fair bit.

As I end this article, let me just share some of them.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

If you’re thinking of opening an Interactive Brokers account, my referral link is here.

As the new account holder, you’ll receive USD 1 in IBKR stock for every USD 100 you deposit, up to USD 1,000 in shares — so a USD 10,000 deposit gets you USD 100 in IBKR stock, and the bonus is capped at USD 1,000 for deposits of USD 100,000 or more. A few other things to know: the minimum deposit to qualify is USD 10,000, done within 30 days of opening, and the bonus shares are locked up for one year from the award date. The promotion is currently active, and using the link costs you nothing extra. On a separate note, if you haven’t already, it’s worth taking a look at how IBKR’s share price has performed over the past five years — the stock you receive as a bonus isn’t just a token; it’s a stake in a company that has done quite well for its shareholders.

I break down my resources according to these topics:

- All my personal notes about how my philosophy behind my own money and how I manage it.

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I work and do research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Fee-only Wealth Advisory Firm Providend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith’s current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

Apple iPad 11-inch: A16 chip, 11-inch Model, Liquid Retina Display, 128GB, Wi-Fi 6, 12MP Front/12MP Back Camera, Touch ID, All-Day Battery Life — Silver

(as of June 27, 2026 02:48 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Flea and Tick Prevention for Cats & Kittens, Topical Cat Flea and Tick Treatment – Fast-Acting & Long-Lasting 6-Dose Supply

$20.98 (as of June 27, 2026 02:43 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

HAOYUYAN Wireless Earbuds, Sports Bluetooth Headphones, 80Hrs Playtime Ear Buds with LED Power Display, Noise Canceling Headset, IPX7 Waterproof Earphones for Workout/Running (Black)

$23.73 (as of June 27, 2026 02:54 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Beats Studio Pro Premium Wireless Over-Ear Headphones- Up to 40-Hour Battery Life, Active Noise Cancelling, Great for Travel & Commuting, USB-C Lossless Audio, Apple & Android Compatible -Black

(as of June 27, 2026 02:59 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Post Comment