Is the Economy Finally Turning the Corner? Why Stagflation and Recession Fears Might Be Overblown—And What That Means for Your Next Move!

Ever feel like the market’s playing a relentless game of hide-and-seek with us investors — just when you think you’ve got a handle on inflation, recession, or rate hikes, the landscape shifts again? Last Friday, Jeff deGraff from Renaissance Macro stepped onto the OffScript podcast stage to unpack the messy reality behind those moving targets. Before Jerome Powell even opened his mouth, there were debates swirling on whether we’d need to lower rates or brace for runaway inflation. Spoiler alert: Jeff’s take cuts through the noise with some level-headed clarity, reminding us just how fiendishly tricky it is to predict this beast we call the market. From Asia’s surprising strength to the nuanced winners and losers in U.S. sectors, and a data-driven dissection of stagflation odds—this is one conversation that punches above its weight in insight. Could there be a smarter way to read the pulse of global markets without losing your shirt? Let’s dive in. LEARN MORE

Jeff deGraff of Renaissance Macro in this week explains the state of the markets in this OffScript podcast last Friday:

Even before Jerome Powell’s comments on Friday, there is such a diverse view if we need to lower rates or that inflation will be dramatically bad.

My sensing based on those more level headed views is that inflation, compare to recession is a relatively smaller monster at this point.

Jeff’s view is one that I take note of. Almost everyone is pretty data focused so it is not that they are not quantitative. It kind of shows just how hard to foretell these things upfront.

Asia Strength

Jeff explain that whatever that he has to say applies to the frontier markets, which is the segment of the market that is not name emerging markets.

These frontier markets have rallied strong and vigorously.

China, Hong Kong, Korea, Vietnam equity markets have done extraordinary well.

Japan is at a 35-year high. This is critical because this is the first 35-year high that we have seen… in 35 years. This is what they call a fresh high. The Topix have not seen a high since 1989 until this quarter.

These improvements in the markets seem to be telling investors something.

Whatever these tariffs that are enacted seem to be working well for the world collectively.

If Jeff compare Asia and Europe, he favors Asia.

The Mag 7 in the US are relative strength leaders and you are going to have relative strength leaders in any markets. What we are most afraid of is not missing out on the relative strength leaders and lose money because of that. If you are still making money relatively, that is important.

This is not happening in Europe because aside from utilities, financials, aerospace and defense, you are not making money in discretionary, industrials outside aerospace and defense. Asia is more broad based across tech, industrials.

The US

Jeff observe that this is a unique time where within sectors, aside from financials, there are winners and losers. There are clear strong sub-sector groups and weaker ones. For example in semiconductors, Nvidia and Credo looks good but you have ASML, Intel that doesn’t look as good.

This can be daunting but also a great opportunity for portfolio managers to differentiate their performance.

What is the Probability of Stagflation or Recession in the Next 12 Months?

Jeff’s definition of stagflation: Inflation higher than GDP or negative real growth.

The Renaissance Macro Market Cycle Clock, which juxtapose the relationship between inflation and growth, points us to an area that we are almost at stagflation. More of a muddled environment than a clear stagflation.

The good news is that the indicators of stagflation is coming down in terms of the inflation inputs. Big reason is energy prices is a huge component. There is a reason why Scott Bessent is so focused on energy because that passes through so many different things and by focus on one area, you address an issue like inflation broadly.

Tariff creates a lot of noise around inflation, when people try to buy before the tariffs take place. Renaissance Macro have backups in inflation indicators, which are data focused and they have data going back to the late 1940s, which makes it a rather wide dataset.

The dataset shows that we really get into an inflation problem mainly in a supply shock. Think Saddam Hussein invading Kuwait and what that did to energy. Tariff do cause these indicators to tune up.

But the good news is that they are also starting to see the indicators relive itself.

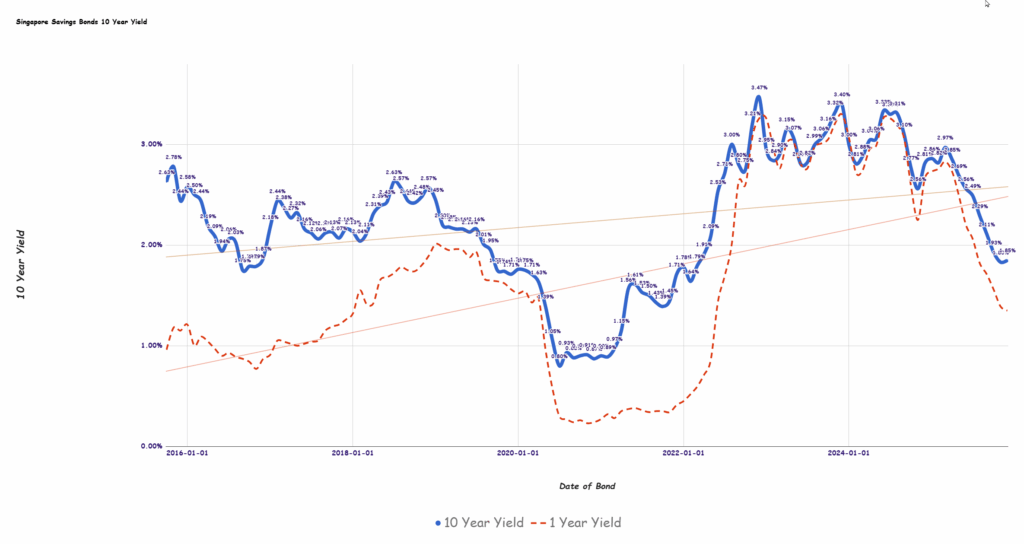

The one area the economist is not strong on in predicting recessions is what has been happening in the credit markets. Renaissance Macro has always been big on using credit market data. For 25 of 35 years of his career, Jeff has been focused on credit because credit is such a good window into the soul of the economy.

There is not a lot of value in corporate credit. Corporate credit spreads are incredibly tight and we will be hard-pressed to have a recession when the corporate credit spreads is this tight.

Credit spreads will reflect the expectations of aggregate demand because if aggregate demand is contracting, a person’s ability to pay your bills or interest payments go down. Your margins get compressed and that will be reflected in the credit markets.

Jeff’s gut feel, taking in all this is stagflation does not manifest itself or follow through. Based on the credit market, the risk of recession is alleviating.

If you want to trade these stocks I mentioned, you can open an account with Interactive Brokers. Interactive Brokers is the leading low-cost and efficient broker I use and trust to invest & trade my holdings in Singapore, the United States, London Stock Exchange and Hong Kong Stock Exchange. They allow you to trade stocks, ETFs, options, futures, forex, bonds and funds worldwide from a single integrated account.

You can read more about my thoughts about Interactive Brokers in this Interactive Brokers Deep Dive Series, starting with how to create & fund your Interactive Brokers account easily.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith’s current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

Purina Fancy Feast Grilled Wet Cat Food Seafood Collection in Wet Cat Food Variety Pack - (Pack of 24) 3 oz. Cans

$20.97 (as of November 3, 2025 03:44 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Pack Approved Beef Shin Bones for Dogs - Liver Coated Long Lasting Dog Chews for Aggressive Chewers - Rawhide-Free Big Bones for Large Dogs - Healthy Large Dog Bone (1 Pack)

$15.99 (as of November 4, 2025 03:40 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Amazon Echo Dot Max (newest model), Alexa speaker with room-filling sound and built-in smart home hub, designed for Alexa+, Graphite

$99.99 (as of November 4, 2025 03:10 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Surge Protector Outlet Extender, Addtam Multi Plug Wall Outlet with 4 USB Ports(1 USB-C), 3-Sided 1800J Power Strip Plug Extension Outlet Splitter, Black

$9.99 (as of November 2, 2025 03:10 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Post Comment