Why JPY’s Latest Move Isn’t 2013 Redux—and What It Means for Your Next Big Investment Move

Ever wondered what happens when a fresh political breeze meets an economy hungry for revival? That’s exactly the scene unfolding in Japan with the so-called ‘Takaichi trade’ stirring up quite the financial storm — a steeper yield curve, roaring equity rallies, and a Japanese Yen (JPY) that’s taken a bit of a tumble. It’s like watching the sequel to Shinzo Abe’s bold 2013 playbook, but with a twist—inflation has crashed the party, changing the script entirely. Now, with inflation above 2% and the Bank of Japan’s current governor tightening the reins rather than easing up, USD/JPY isn’t sprinting towards 160 as some might expect. Instead, we’re eyeing 145 as a more probable finishing line for this year. The big question: will the Bank of Japan bend under political pressure or stick to its guns? Hang tight, because this financial drama is far from over — and it might just reshape your investment outlook in ways you hadn’t imagined. LEARN MORE

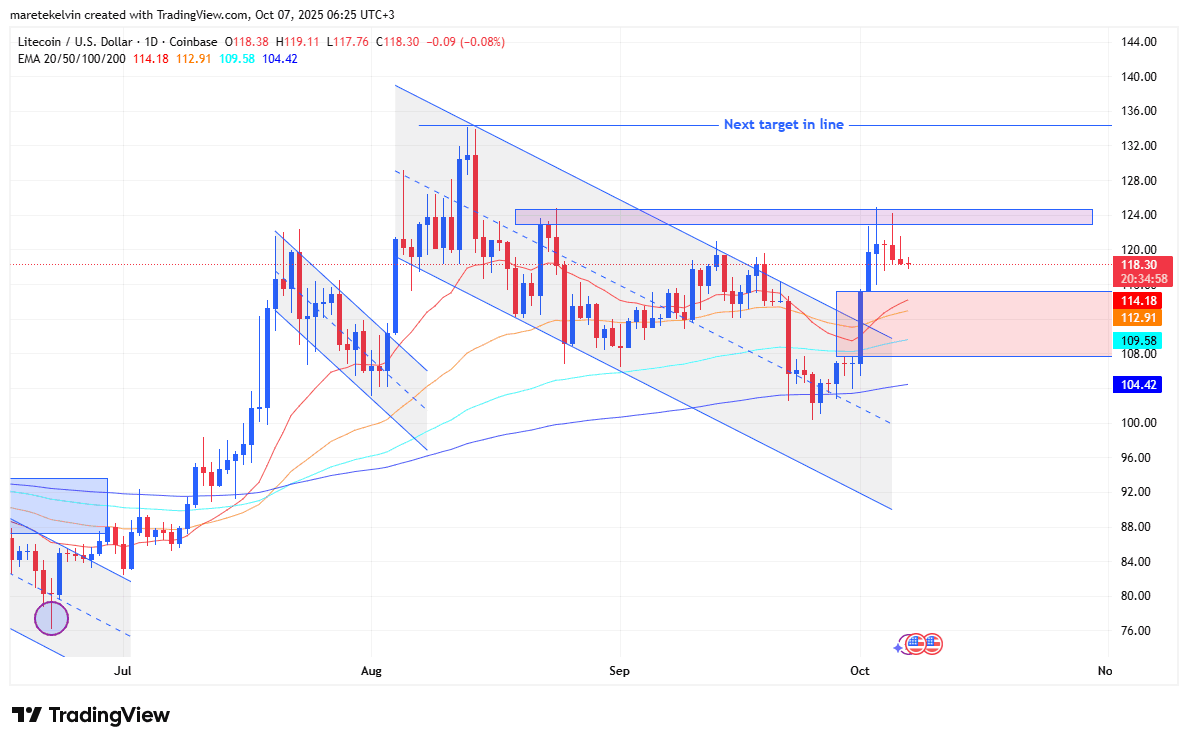

The ‘Takaichi trade’ has indeed delivered a steeper yield curve, an equity rally and a weaker Japanese Yen (JPY), ING’s FX analyst Chris Turner notes.

USD/JPY might be ending the year nearer to 145 than 155

“The presumption here is that the new government under Sanae Takaichi exerts all its influence to deliver a stronger economy. This would include the Bank of Japan presumably ending, if not reversing, its tightening cycle and some heavy fiscal stimulus. Parallels are being drawn to Shinzo Abe’s term of 2013-20, which saw the Bank of Japan grow its balance sheet from 30% to 100% of GDP and the trade-weighted yen initially fall around 25%.”

“The big difference between 2013 and today is inflation. Back in 2013, Japan had been suffering deflation and a new BoJ Governor in March 2013, Haruhiko Kuroda, instituted a new 2% inflation target. Today, Japan’s inflation is above 2%. Inflation is proving to be a top concern for voters, and the current BoJ Governor, Kazuo Ueda, with three years left on his term, is in the process of raising interest rates and shrinking the central bank’s balance sheet. This is the case for USD/JPY not now surging towards 160.”

“For the near term, the focus is going to be on what pressure is brought to bear on the BoJ. Markets now price only a 20% chance of a rate hike at the 30 October meeting. A delay in a hike into next year or even later will further weigh on the yen. But if we’re right with our call for a weaker dollar into November and December, USD/JPY could be ending the year nearer to 145 than 155.”

Apple Watch Series 11 [GPS 42mm] Smartwatch with Rose Gold Aluminum Case with Light Blush Sport Band - S/M. Sleep Score, Fitness Tracker, Health Monitoring, Always-On Display, Water Resistant

$389.99 (as of October 7, 2025 02:45 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

sajawass Wireless Earbuds Bluetooth 5.4 Headphones, Noise Canceling Ear Buds with 75hr Playtime, LED Power Display, IPX7 Waterproof Earphones Over-Ear Earphones for Sports/Workouts - Rose Gold

$22.49 (as of October 7, 2025 02:45 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Milk-Bone Soft & Chewy Dog Treats, Beef & Filet Mignon Recipe, 25 Ounce

$14.48 (as of October 7, 2025 03:04 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Fresh Step Advanced Simply Unscented Clumping Litter, Fresh Step Unscented Cat Litter Fights Odor on Contact, 18.5 lb. Box

$15.99 (as of October 7, 2025 03:10 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Post Comment