Are You Brave Enough to Face the Life-Changing Truths That Could Make or Break Your Future?

Ever felt like fixed income is just a boring, slow-moving part of your portfolio—until suddenly it looks as wild as the stock market? You’re not alone. The secret sauce most folks miss is “duration,” a subtle yet powerful concept that can totally flip how you see bonds and fixed income investments. Duration isn’t just geek-speak; it’s the reason why a 20-year US Treasury ETF can feel like riding a rollercoaster while a 1-3 year Treasury barely stirs the waters. What if I told you that misunderstanding this nuance could lead you to think fixed income behaves like equities—wreaking havoc on your financial plan? Stick around, because once you grasp how duration and credit work together, you might find fixed income is less villain, more unsung hero in your wealth-building journey. Ready to dive in? LEARN MORE

img#mv-trellis-img-1::before{padding-top:71.09375%; }img#mv-trellis-img-1{display:block;}img#mv-trellis-img-2::before{padding-top:71.09375%; }img#mv-trellis-img-2{display:block;}img#mv-trellis-img-3::before{padding-top:24.043715846995%; }img#mv-trellis-img-3{display:block;}

There are things in investment that if you understand some of the nuances, it might make you look differently.

One of the nuance is about duration in fixed income.

The challenge with these nuances is that you can write so much, but if a person doesn’t get it, they just gloss over it.

I think its not the first time I written about it but why?

It is because I think people look at fixed income as all the same. It is even worse if you are a layman.

In my mind, they think the worse case for fixed income looks like equities.

Which is not the case if you respect both duration and credit.

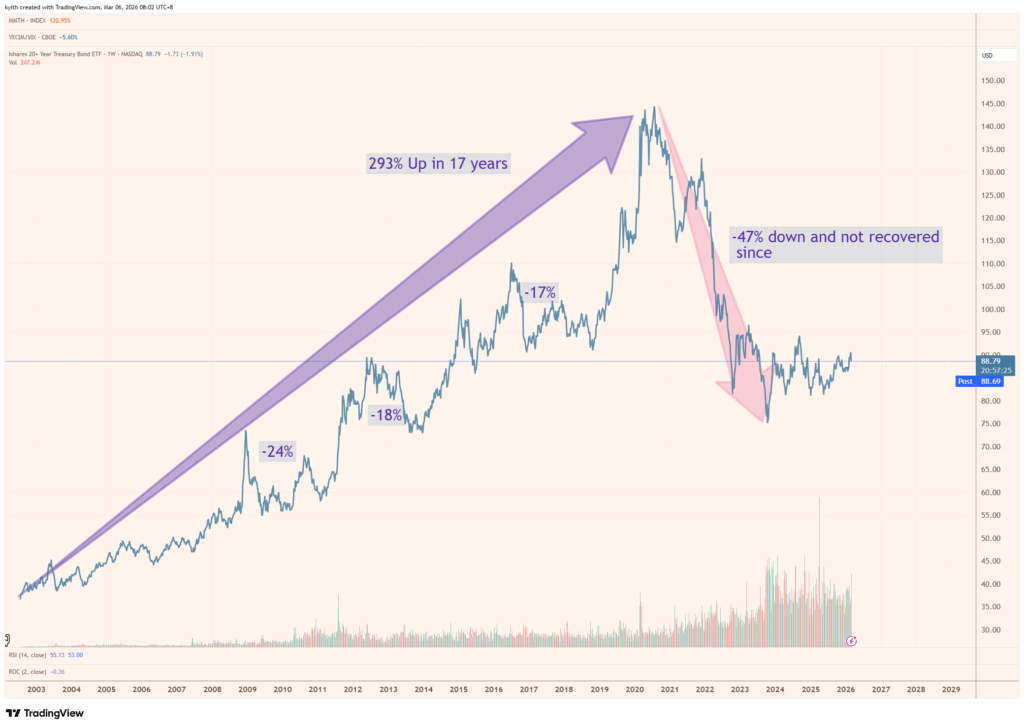

The chart below shows the price and dividend return of the TLT or the 20-year US Treasury ETF:

I think this is what everyone has in mind perhaps because financial bloggers or influencers keep using something with a 20-year maturity.

They may also find the returns more appealing during the 2010 to 2020 low interest rate environment. Indeed, for the first 17 years a TLT would compound wealth at 8.3% p.a.

But there are some pretty big drawdowns of -24%, -18%, -17% as you can see.

When short term interest rates rose 400%, and in the case of the 20-year market interest, the interest rate rose from 1.8% to 5.2%. If a 1% rise in interest rate cause a 15-20% down move in price of a 20-year fixed income based on duration, what will happen if interest rate went up 3%? you can see correspondingly, the drawdown is about 3 x 15% = 45%.

And then investors had this impression that fixed income is no different from equity.

Let me show you the 1-3 year US Treasury experience:

The annualized return is more muted over the 18 years at 2.2% p.a. but each drawdown is also much more shallow. During the same period when TLT went down 47%, the SHY went down 4.5%. The best part is that it has since recovered.

Now if you are thinking about money that you need in 3 years, you would have fxxk your plan up if you put your money in something long duration.

The most damaging thing is people seeing the 47% drawdown of fixed income and have the impression that fixed income is like equities.

It means you have to get the timing right.

And that it has no place in the portfolio or in your financial plan.

Which you can see it is not always right.

If you are diversified, and control the credit exposure of your fixed income, fixed income can be a sweet spot.

SHY took 2.7 years to fully recover and the SHY has an effective duration of 1.7-1.8 years.

If we use the rule of thumb of (2 x 1.8 – 1) = 2.6 years, that is roughly how long it takes to recover, but perhaps not capturing the returns. Then again the yield to maturity before the drawdown was rather low:

- 20 Sep 2021 2-year Govt Yield: 0.2%

- 24 Oct 2022 2-year Govt Yield (at the deepest part of the drawdown): 4.5%

If you hold 2.6 years you should earn 0.2% p.a.

The conclusion is not too wrong its just the returns are so low to begin with.

Nuances like this shape how we plan.

But admittedly, I don’t always explain well these things and because of that, I failed to value add to someone. But they can be critical.

Because if you perceive fixed income correctly they can be rather useful to you. Not just you because you might be helping your parents plan and you shape your view.

I just happen to share this with a friend and through our conversation, both of us realize he interpret a rolling returns charts wrongly, a chart on deepest fixed income drawdown differently.

If I left it to his own review and he did not clarify, I would never have known some would interpret different materials differently (it kind of show you how hard sometimes these things can be).

But interpretations matter especially if you are trying to build wealth.

If you see it the right way, you may have more peace of mind and conviction to funnel $3 mil of your spare fund into a short term diversified fixed income vehicle instead of vexing over how to get the highest return without so much risk exposure.

That is a more pleasant and feel-good personal experience than another personal experience these past 2 days.

I saw a comment that I put on a YouTube video removed. I think that is okay but it kind of lets me know how a person feels about learning the true essence of something, their degree of vulnerability, versus how others perceive their skill.

At the end of the day, we got to ask ourselves what we want.

- Do you want to rationalize that you are right, even though deep inside you, you already detect that you don’t get the full picture / there is something you felt uncomfortable but cannot explain?

- Are you more concern with presentation, how you look to others and less concern about getting the mental framework right?

There will be tough things for all of us. If we have a struggle with controlling cholesterol, learning to read materials and research on the subject is daunting because every start is daunting. At the end, perhaps the market for personal growth is also efficient between effort and money. If it is very valuable, you either spend effort to make space to comprehend (like duration) or you spend money and eventually you get the same epiphany.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

I break down my resources according to these topics:

- All my personal notes about how my philosophy behind my own money and how I manage it.

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I used to work doing research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

- Havend – Where I currently work. We wish to deliver commission-based insurance advice in a better way.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Fee-only Wealth Advisory Firm Providend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith’s current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

Best Pet Supplies Interactive Squeaky Dog Chew Toy, Ideal Dog Toys for Chewers, Small, Medium & Large Dogs, and Fetch Lovers - Crinkle Duck (Blue), Large

$5.99 (as of March 30, 2026 02:16 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Good ‘n’ Fun Triple Flavor Kabobs Chews for All Dogs, 24 Ounces, Treat Your Dog to Long-Lasting Chews Made from Beef Hide, Real Chicken, Pork Hide, Duck and Chicken Liver

$14.39 (as of March 30, 2026 02:16 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

JBL Go 4 - Ultra-Portable, Waterproof and Dustproof Bluetooth Speaker, Big JBL Pro Sound with Punchy bass, 7-Hour Built-in Battery, Made in Part with Recycled Materials (Black)

$39.95 (as of March 30, 2026 02:20 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Hint Infused Bottled, Best Sellers Variety Pack - Sugar Free Flavored with Zero Calories, Natural Essences, and No Artificial Sweeteners - 16 Fl Oz (Pack of 12)

$13.46 (as of March 30, 2026 02:16 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Post Comment