Shield Riders Hit a Crossroads: What’s Next Could Make or Break Everything—Are You Ready to Watch?

Is your hospital plan rider deadline creeping up faster than a late-night infomercial? With April 1st, 2026 just around the corner, many of us are scrambling to figure out if we need to act or if it’s just another passing headline. Here’s the kicker: according to the Ministry of Health’s latest guidelines, you might not have to lift a finger—yet. They’re shaking up the insurance world with new rules aimed at taming soaring healthcare costs, which means more out-of-pocket payments and a steeper co-payment cap doubling from $3,000 to $6,000. Insurers will roll out new riders fitting these fresh standards, leaving us pondering the trade-offs: higher out-of-pocket costs but potentially steadier premiums. So, what does this actually mean for your wallet when those hospital bills arrive? Let’s break down the nitty-gritty before the deadline turns into a done deal. LEARN MORE

img#mv-trellis-img-1::before{padding-top:50.9765625%; }img#mv-trellis-img-1{display:block;}img#mv-trellis-img-2::before{padding-top:49.31640625%; }img#mv-trellis-img-2{display:block;}img#mv-trellis-img-3::before{padding-top:53.90625%; }img#mv-trellis-img-3{display:block;}img#mv-trellis-img-4::before{padding-top:118.65585168019%; }img#mv-trellis-img-4{display:block;}img#mv-trellis-img-5::before{padding-top:111.7903930131%; }img#mv-trellis-img-5{display:block;}img#mv-trellis-img-6::before{padding-top:108.82040382572%; }img#mv-trellis-img-6{display:block;}

Some may be discussing if I need to make a decision on my hospital plan rider given that there is some deadline on 1st Apr 2026, which is about 4 days away.

And you may wonder if it applies to you.

Based on what I read, there should not be any actions that you need to take. MOH give new guidelines to try and improve this escalating insurance cost situation. What they proposed is that:

- Policyholders would have to pay deductibles from now on. Your rider will not cover. More out of pocket money needs to come from cash.

- There will be a higher co-payment cap. The annual co-payment cap will increase from $3,000 to $6,000. Co-payment is the policyholder (you) share of the hospital bill and with the rider, it will cap potential out of pocket to $3000 existing. But that will be $6000.

- With this, the insurers will release new rider plans that align to these new standards.

Eventually Your Out-of-Pocket Cost with New Riders will be Higher but your Premiums may be more in Control.

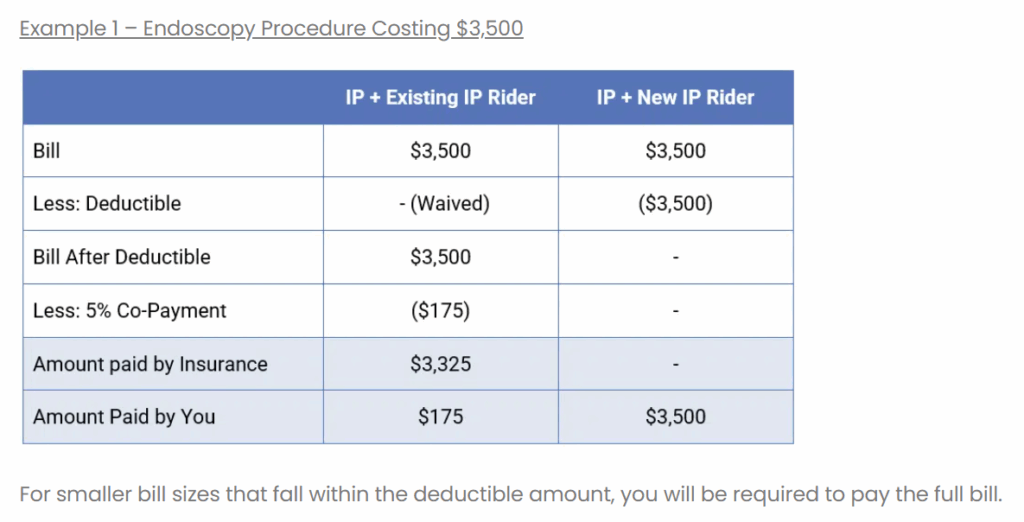

Havend has some good illustration of how your out-of-pocket cost will look like with existing and potential new riders:

5% of the $3500 bill is $175 and the nice thing about a rider is it reduces the out of pocket spending of even a small bill. With the change to a new rider that doesn’t cover the deductible, you will have to pay all of the $3500.

In a way, perhaps there are too many of these small bills of high frequency at private hospitals. Hence by making you feel some of the pain, it might make a policyholder consider the grade of care.

5% of the $10000 bill is $500 and the existing rider will reduce your out of pocket costs dramatically. With the new rider, you will need to pay the deductible of $3500, for that calendar year. If you are admitted more than once during the calendar year, you do not have to pay the $3500 deductible again.

What is left of the bill is $6500 and 5% is $325 and you have to pay this portion with the rest offset by the insurance plan and rider. So your total out of pocket is $3825.

The difference is $3300 which is the same as the previous bill.

This the major bill. The six figure bill.

And in truth this is where we really want the shield plan to do its work.

5% of a $100,000 bill is $5,000. This should be the amount that you have to pay out-of-pocket, but since your private doctor is on a panel, your out-of-pocket is capped at $3,000. So you pay $3,000.

With the new rider, you definitely need to pay the $3500 deductible if you have paid for the calendar year. What is left is $96500. If you don’t have the rider you would need to pay a 10% co-insurance or $9650 but since you have the rider its 5% of $96,500 or $4825. The insurance will pay for the rest and you end up paying $8325.

Whether it is $3000, $8325, or $13,150, an effective plan is one that you pay a small amount relative.

The Out-of-Pocket Cost if You have a New Rider Versus No Rider at All, for Different Bill Costs.

I would like to see the difference if the bill is from $10,000 to $200,000 if we have a rider versus no rider. This is not a comparison of existing rider and new rider, but bear with me.

You can see that the new rider is still pretty effective if the bill is significant above $50,000.

I guess many don’t like to have out-of-pocket spending because they don’t have or don’t know how to save up for it.

Without the rider, you would have to pay about 10% of the bill, mostly because the bills are significant enough that the deductible matters less.

Existing Rider Versus New Rider for Different Bill Costs.

We add the existing rider into the mix:

You can see that whether it is capped at $3000 or $6000, the rider still does its job if the bill size is significant. The rider still alleviates large bills.

If You are Attended By a Non-Panel Doctor the Rider Does Not Cap Your Out of Pocket Expenses.

You can visit a private doctor that charges far higher than normal private doctor, so much so that the insurer do not wish to take the risk together.

Your rider then would not cap the bill and it would look this way:

The rider still alleviates 50% more than if there isn’t a rider.

If Most People are Cash Poor, This Latest Move May be More Effective.

The goal of this change is for the policy holders to feel more of the money pain. If you don’t feel pain, you won’t want to seriously consider the trade-offs.

And you will still go to the private doctor.

But if you face the uncertainty of how much cash flow you need to cough out, you start considering if you should go government.

There is Not Much You Can do Today.

- If you have an existing rider plan that covers the deductible and capped at $3,000, and you are happy with it, then you don’t have to do anything. (we will come back to this later).

- If you don’t have a rider now (as of 27 Mar 2026), and would like to get one, you can purchase a rider. But you and those that bought their riders between (27 Nov 25 to 31 Mar 26) will be required to switch to new riders no later than their next renewal after 1 April 2028..

- From 1st April, the insurer will announced new riders that are aligned to the new changes.

Those that are on existing plans will have to see if the insurer will change the existing plans. It is not a given your benefits will not change. In any case, your premiums may go up in such a rapid rate that even though you have better coverage, you may be paying it today in higher premiums.

New Riders 30% Cheaper than Existing Ones? Tamper with your Expectation.

MOH estimates premiums of new IP riders will cost about 30% less than existing riders with maximum coverage — translating to average annual savings of about $600 for private hospital policyholders and $200 for public hospital policyholders.

But I think you kind of need to adjust your expectations.

Singlife is probably one of the insurer that currently have a rider that does not cover the deductible.

And I am currently on such a rider.

If you reader this post, you can kind of figure out they still jack up my premiums massively:

So it is cheaper, but you will also have to adjust your expectation that if you wish to cover hefty private out-of-pocket spending, the premiums on an absolute level is not going to be cheap.

If You Prefer a Government Grade of Care, The Picture Will Look Dramatically Different.

This is because

- The scaling of the range of bills possible is lower. This means the major bill cost much lower than private.

- Costs are more in control, and so the premiums for shield and rider is also more manageable.

- Since the premiums of rider is much more affordable, you can cover and still reduce your out of pocket costs.

The question is whether you can accept that grade of care.

There is a trade-off to think about.

If you want to trade these stocks I mentioned, you can open an account with Interactive Brokers. Interactive Brokers is the leading low-cost and efficient broker I use and trust to invest & trade my holdings in Singapore, the United States, London Stock Exchange and Hong Kong Stock Exchange. They allow you to trade stocks, ETFs, options, futures, forex, bonds and funds worldwide from a single integrated account.

You can read more about my thoughts about Interactive Brokers in this Interactive Brokers Deep Dive Series, starting with how to create & fund your Interactive Brokers account easily.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Fee-only Wealth Advisory Firm Providend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith’s current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

Amazon Fire TV Stick 4K Plus (newest model) with AI-powered Fire TV Search, Wi-Fi 6, stream over 1.8 million movies and shows, free & live TV, find shows faster with Alexa+

$24.99 (as of March 28, 2026 02:15 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

UP URARA PUP Halloween Dog Collar with Flower, Pink Halloween Puppy Flower Collar with Adjustable Metal Buckle,Fancy Halloween Dog Collar Bowtie Gift for Girl Boy Dog,M

$16.99 (as of March 28, 2026 02:18 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Idymere Stainless Steel Litter Box with High Sided, Metal Cat Litter Box, Odor-Free, Non-Stick Litterbox Pan, Easy to Clean Pet Supplies Toilet Tray for Indoor Cats, Kittens or Multicat Homes

$17.99 (as of March 28, 2026 02:15 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

IAMS Proactive Health Adult Wet Dog Food Variety Pack, 3.5 oz. Pouch, (18 Count)

$23.98 (as of March 28, 2026 02:15 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Post Comment