The Shocking Truth Behind the Money Our Dad Left Us—And Why It Could Change Everything You Thought About Wealth Forever

When my dad passed away in early 2023, my brother and I found ourselves staring at an inheritance of about $118,000—an amount that felt both like a gift and a weight. You know that strange feeling when money isn’t quite yours, yet you hold the keys to it? That’s what we faced. It’s not part of my usual investment pools like Daedalus or Crystalys, but it comes with its own set of challenges and responsibilities. How do you handle money that your parents painstakingly built, yet now you’re tasked with preserving and growing it — without messing up? This isn’t just about numbers on a screen; it’s an emotional tightrope walk filled with subtle nuances. In this journey, I’m stepping back, reflecting on the strange dance between responsibility and freedom, and mapping out how to steward this legacy wisely. Curious how one can turn inherited wealth from a burden into a resource that honors both past and future? Let’s unpack this together. LEARN MORE

img#mv-trellis-img-1::before{padding-top:47.75390625%; }img#mv-trellis-img-1{display:block;}img#mv-trellis-img-2::before{padding-top:65.13671875%; }img#mv-trellis-img-2{display:block;}img#mv-trellis-img-3::before{padding-top:71.77734375%; }img#mv-trellis-img-3{display:block;}img#mv-trellis-img-4::before{padding-top:73.14453125%; }img#mv-trellis-img-4{display:block;}img#mv-trellis-img-5::before{padding-top:74.21875%; }img#mv-trellis-img-5{display:block;}img#mv-trellis-img-6::before{padding-top:73.046875%; }img#mv-trellis-img-6{display:block;}img#mv-trellis-img-7::before{padding-top:24.043715846995%; }img#mv-trellis-img-7{display:block;}

When my dad passed away in early 2023, my brother and me inherited about $118,000 in various accounts. We can consider this my parent’s money but essentially we still have about $67,000 in iFAST which is what my mom left us.

This money is not in both my more publicly known pool of money Daedalus and Crystalys.

My colleague Yong Cheng, the Deputy head of Advisory at Providend wrote about what does inheritance means to the child who inherit the money.

We all end up with a weird relationship how we look at the money. Brandon felt mixed emotions dealing with money that felt is not his, but is actually his. There is also the weight of responsibility of being more careful with the money, but also a sense of vulnerability not knowing what you don’t know.

In Kyith’s term, Brandon most likely is afraid of fxxking up a meaningful sum of money with a very different status.

We should all be aware inherited money might mean different things to different people (and they might not tell you upfront about what it means, but hide behind some weird conversational points).

I felt that these money was painstakingly build up not by my hands but with their hands. Adding about $100k to $200k can mean telling people my net worth is different but because its given and not built or earn by my bare hands, I am the allocator of the money but its not exactly my money.

I have less insecurities about losing the money through mismanagement because I think I know roughly how to grow or preserve wealth knowledge-wise.

Goal-less Wealth Preservation for Now

Every dollar productively should be allocated to fulfill a certain financial goal. Financial goal can either be to pay for a past spending (i.e. paying off debt), current spending (your expenses today) or future spending (future financial goals such as paying off mortgage, children’s education and retirement income).

I more or less funded a lot my future stuff with my own money so this money is goal-less and usually in goal-less mode, we can also considered the money in wealth preservation mode: Growing to keep up with inflation but managing the money sensibly so that we don’t lose it.

We have a term for this at Providend and its call Asset Enhancement. I really cannot connect with the name asset enhancement because it is such a vague term. And many a times, clients together with their adviser carve out a portion and gave it a name (which is the right thing to do in my opinion). There is a name but it should not be call Asset Enhancement.

Our dad left us with $118,549 and I decided that I want to separate them in an account so that it is easier for accounting.

In a different account, I will just need to keep track

- The inflows into the account (likely the initial contribution)

- Any outflows from the account (like wealth cash flows to pay for donation by selling units or dividends)

This makes calculating the money weighted return or XIRR easier.

I decided to channel my money into an Endowus account.

I wanted to create that segregation but there is also other reasons:

- I want to reduce the hassle of implementing it under Providend. (Part of my CPF investment and all of my SRS investment {the SRS money is also in Daedalus} is held under Providend)

- Endowus is pretty good in having a variety of unit trust options, not to mention investments for Accredited Investors to implement.

- I known some of the founding members of Endowus since their formative days and are comfortable with how they run it. Being in the industry, I was able to also know the advantages of an MAS regulated entity.

- Their fees are reasonable for the investments that I would most likely implement.

The Current Implementation

You can roughly implement your portfolio:

- Endowus Flagship portfolios. These are curated portfolios based on their investment and wealth management philosophy of what they deem as portfolio can be your core, factor-based, income-based. The portfolios will be rebalanced periodically, and the managers will change the funds when they deep appropriate. They charge from a range of 0.25% – 0.60% p.a. in fee depending on how much money you invest with them.

- Endowus Fund Smart. You can customize your portfolio and select your own funds. Each of the fund would be view as a one-fund portfolio. They charge a lower fee of 0.30% p.a. for this. You can add more funds into that portfolio but the fees will go up accordingly.

I implement my portfolio with Fund Smart.

Currently I have invested about S$93,000 out of the S$118,549.

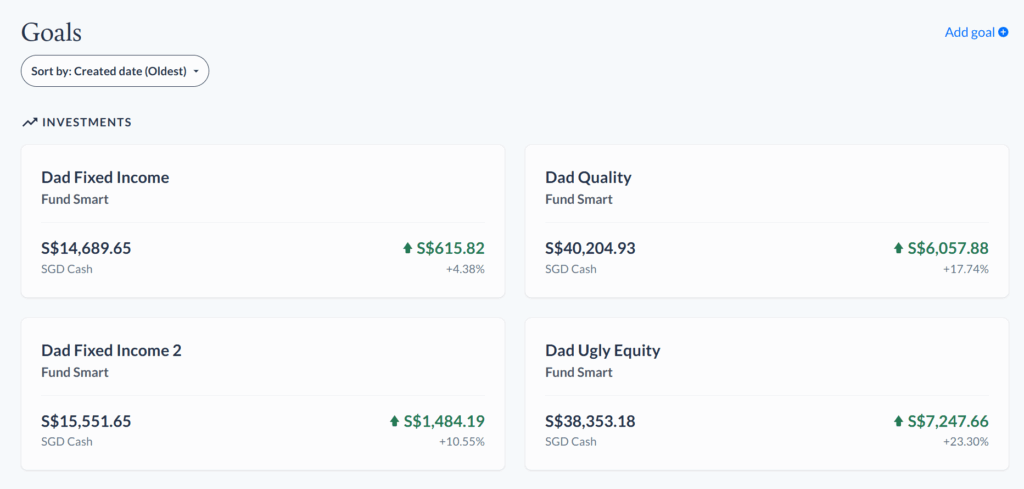

It looks like this currently:

They look like individual portfolios for individual goals and it is. I have to give a name for each Fund Smart portfolios. The Fixed Income names are funds that are fixed income and the other two are equity.

Here is what I invested with:

| Fund Smart Goal Name | Fund | Fund Expense Ratio | Region | Strategy |

| Dad Fixed Income | Amundi Core Global Aggregate Bond SGD-Hedged | 0.10% p.a. | Global | Index Tracking |

| Dad Fixed Income 2 | PIMCO GIS Income Fund SGD-Hedged | 0.55% p.a. | Global | Discretionary Active |

| Dad Quality | GMO Quality Investment Fund | 0.53% p.a. | Global | Quality Factor |

| Dad Ugly Equity | Dimensional Global Targeted Value Fund | 0.44% p.a. | Global | Value with some slight Profitability |

I started with $5000 in lump sum and have periodically added overtime. Readers might have seen me talk about each of the funds on and off and I will link you to them here:

- On GMO Quality Investment Fund: Post

- On Pimco GIS Income Fund: Post 1, 2, 3, 4

- On Global Aggregate Bond: Post 1, 2, 3, 4, 5

All of these funds are Accumulation class

How I Think about the Investment Strategy

If you have seen how I explain Daedalus Income portfolio, this is pretty consistent with that. The returns and risks that your portfolio faced is based on the asset allocation. Traditionally, equities will have the highest probability of giving you the best return and you should view equities as a pseudo fixed income security that has a 20-23-year duration.

If you hold it for that long (if you are an accumulator), you should successfully harvest decent nominal returns. Unfortunately, we are uncertain over the experience in that 20-23 years. It can be pretty volatile, with periods that you feel like selling off your investments or make you question if you make the right investment choices.

Some of us cannot take it and there is fixed income.

The general fundamentals of fixed income means you can get your money back if you respect the duration. For example, both the Pimco and Amundi fixed income funds here have a duration of 6 years which means if I held it for around 6 years, even if the price volatility is crazy, each fixed income securities should go back to the principal value if they don’t default. This is fundamental and unique to fixed income relative to equities. Fixed income is less volatile, and their returns are lower than equities but you got to accept that you cannot tolerate that much craziness in your life.

What will drive the return of this pool of money is how much equities versus fixed income. Currently that is about 75% in equities. The fixed income will give returns just lower.

I am not so concern over the asset allocation since this is to preserve wealth. As long as the equity allocation is above 50% then it is okay.

Now something specific to equities. I chosen two actively managed funds, one with human managers selecting securities (GMO) and the other one with human managers implementing a systematic strategy on developed world small cap (Dimensional).

I understood and would like the opportunity to be exposed to the risks of more quality companies, and small at least profitable companies that is a suspect, in the hopes that eventually they will be able to earn a quality premium and small cap value premium if invest long enough. I expected there to be a premium but not dependent on the premiums because they don’t change lives.

The most important thing for me is to fully invest the money so that i don’t have to think about it. There are more interesting things to consider than to bother about this pool of money that much.

The Side Objectives

I want to have an eye to monitor some of the performances over some of the actively managed funds such as the GMO Quality Investment fund and the PIMCO GIS Income fund over time.

It is different to just, review and track the performance over time versus you have skin in the game. I have written enough about both funds to invest in them. I understand about the research behind how active funds generally struggle to do better than their benchmark indexes and accept the possibility of underperformance (you may not). Underperformance does not mean no performance.

Again, what drives return are more how does equities, in the regions do over the period. The factor premiums in this time and age should be a small component. ‘

How I Implement it Along the Way

The table below is what I tabulated from my Endowus transactions for easy viewing:

| Period | GMO | Dimensional | Amundi | Pimco | Total |

| 6 Dec 23 | $2500 | $2500 | $5000 | ||

| 13-14 Dec 23 | $2500 | $2500 | $5000 | ||

| 24-25 Apr 24 | $2500 | $2500 | $5000 | ||

| 29-31 May 24 | $5000 | $5000 | |||

| 10-13 Jun 24 | $2500 | $2500 | $2500 | $7500 | |

| 15-16 Jul 24 | $2500 | $2500 | $2500 | $7500 | |

| 26 Jul 24 | $1500 | $1000 | $2500 | ||

| 7 Aug 24 | $3000 | $3000 | $6000 | ||

| 11 Sep 24 | $2000 | $2000 | $4000 | ||

| 3 Oct 24 | $2500 | $3000 | $5500 | ||

| 17-18 Dec 24 | $3000 | $3000 | $4000 | $4000 | $14000 |

| 12 Mar 25 | $4000 | $4000 | $8000 | ||

| 9 Apr 25 | $5000 | $5000 | $10,000 | ||

| 6 Nov 25 | $3000 | $5000 | $8000 |

There is not much rocket science to my implementation.

It would be clearer if you view them if I plot the invested on an MSCI All Country World ETF (IMID)

How come there is such a difference between 2024 and 2025?

I guess difference in bandwidth. I don’t usually setup some recurring dollar cost average system into the fund and the down side of that is that when work and life gets busy, you don’t think and nothing gets invested.

It is not like 2024 is less busy than 2025, but I guess that is the nature of life. In 2024, I made a pre-commitment that I have to put more of the money to work so I guess that is why I implemented more.

There were some point in 2025 that I totally forgot that there are still unimplemented money.

Is there a difference between buying the GMO Quality versus the Dimensional Global Targeted Value? Or Pimco GIS versus Amundi Global Core?

Frankly over time not really.

I learn that over time maybe I am fidgeting on things that make little differences.

I do feel comfortable with the Global Targeted Value whenever markets get more expensive because I know its a strategy that would consistently harvest the expensive to buy the cheap. So whenever I put money in it, I get some of the shittiest and iffy companies on the cheap (okay not so shitty since at least they have to be profitable).

But these days if I want to put in fixed income, I will put half in each. If it is equity I will put half in each.

What to do with the rest of the S$25,000?

I suspect another S$15,000 will go into the portfolio next week, which leaves the other $10,000 maybe going in end of the year if I forget again.

Living with their Performance So Far

I pasted the performance reporting from Endowus for all 4 Fund Smart portfolios:

I will touch on a bit about returns measurement. The chart will kind of show the net cash flows and the value of the portfolio. If the blue line dip below the black then that means losing money lah (in simple terms).

Endowus did a pretty good job presenting the performance in 4 different ways. Simple return is the layman return of how much you earn divide by how much you kind of put in. It is the feel good return but the less objective one.

You run into problems with simple return when you consider “I put in money, then I pull out money, so how much is my capital???”

Yup that is the problem but very often client’s can’t understand why it is so difficult for us to just give them a simple return answer.

Because it is not so simple.

Time-weighted return would be an annualized return that is what you can compare against the factsheet of your fund. It does not factor in if you put in a lot of money or very little money at different points.

Modified Dietz and Annualized internal rate of return are two different ways to calculate money-weighted return. This is what I view, and perhaps what I prefer most people to view most of the time.

Money-weighted returns weighs not just based on time (it is usually a compounded return) but also the performance of your decision making. You can invest for 5 years, but if in that 5 years majority of your money is deployed at the absolute bottom of every year, money-weighted returns will look damn good. And it should because it shows that when you see a bottom, you can put in majority of your money. It shows good decision making. But the opposite is also true. Modified Dietz is money weighted but it is not an annualized figure if I am right.

Generally, I don’t look at the $615 return I just look at the Annualized Internal rate of return.

I would discuss both of these fixed income together. I consider that I have kind of the same amount in both. The Pimco fund earns more. If we look at the yield to maturity of the Pimco GIS of around 6% plus to the Amundi 3.5%, over a 2 year time period you can kind of see where the better performance would come from mathematically.

One of my reader did point out about what is the point of the SGD hedged when there is a cost to it. This is something that I did discuss on the background with my colleagues in the Investment Team. There is a cost to hedging and what we understand from Amundi the last time round is that the cost is not that significant. Perhaps the messy part is that with 48% of the Amundi Global Aggregate is in US but the rest is in other currencies. While you benefit from hedging the US portion to SGD, did we lose enough on the rest?

Pimco has about 75% in USD, so if there is a drag on the non-USD allocation, they would have lost out on less.

The GMO fund did its thing but to be fair, a more diversified portfolio of quality did not do as well in the past 2 years compare to a benchmark index that is more heavy with semi-conductors.

I extracted the 1-year and 3-year performance (these are annualized returns) and put them against some quality based funds:

| Fund | 1 Year | 3 Year |

| GMO Quality investment | 14.8% | 20.2% |

| iShares Edge MSCI World Quality Factor UCITS ETF (IWQA) | 15.8% | 18.2% |

| Dimensional US High Profitability ETF (DUHP) | 12.2% | 16.8% |

| WisdomTree Global Quality Dividend Growth UCITS ETF (GGRA) | 12.3% | 13.3% |

| iShares Core MSCI World UCITS ETF (SWDA) | 19.7% | 19.4% |

Sob turns out GGRA (which is in Daedalus) is the poorest performer here. Given this actually the GMO Quality investment fund did pretty well.

I started with the GMO Quality Investment fund and it went through a good period of harvesting some good returns.

For the longest time Dad Ugly portfolio looked real ugly always but I kind of know we are judging them over a period… that we should not be even judging. Just add them equally.

The managers at GMO has a value lens (they are that original value shop) so I need not worry that they own something that philosophically feels expensive. And for the Dimensional one, I am buying the relatively cheap ugly stuff.

And so here we are, the ugly things in this short span turn up looking better than the good looking things.

It is so hard to describe the feeling of living through one of your children doing better than the other and then the other one doing better at something one day, and then another doing better than the other on another thing in another day.

These experience is harder to describe but can really build you if you glean enough from it.

Epilogue – Untangling the Emotional Baggage of this Bag of Money.

Well that is that.

I am not sure what you can glean from this (I honestly think people can’t learn much).

Perhaps the main lesson is that if you have a pool of money that you separate out in the head, it can be pretty distracting. We can benefit a lot by just considering the money as one pool. Then again, that is not always a good idea. Arghhh what the fxxk are you talking about Kyith!!!

Splitting your money into different pools allows you to visualize what they are for better. But recognize that its also a job if you have not fully invest in them. You can easily screw up by totally forgot to deploy them.

This is not a problem for everyone.

There may be a lot of people with a lot of money, and their job takes up not a lot of time, so they can have the mindshare to consider this.

If you don’t have that kind of luxury, but still have a lot of money then you may feel this more.

Perhaps the more important point that I have not mentioned is… Sometimes you got to learn to see that the money is meant more to give your family a good life.

And this means that its not their money, but it is your money.

It might mean untangling some of the baggage that you are undeserving of this money because you have not been that good of a son or daughter.

It might mean thinking about what they would want you to do with that money. Would they want the best for their grandson and grand-daugther?

It might sometimes mean putting pressure on yourself to give yourself a new challenge because you have not done anything that you feel they would be proud of. And so now is the time to show them that you can integrate these money well and thrive in life.

What I do personally is not a blueprint but to look at whether this is what you want it to end up.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

I break down my resources according to these topics:

- All my personal notes about how my philosophy behind my own money and how I manage it.

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I used to work doing research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

- Havend – Where I currently work. We wish to deliver commission-based insurance advice in a better way.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Fee-only Wealth Advisory Firm Providend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith’s current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

Hint Infused Bottled, Best Sellers Variety Pack - Sugar Free Flavored with Zero Calories, Natural Essences, and No Artificial Sweeteners - 16 Fl Oz (Pack of 12)

$13.46 (as of March 30, 2026 02:16 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

The Only Bean Crunchy Dry Roasted Edamame Snacks (Sea Salt), Healthy High Protein(11g) Keto Food, Low Carb Gluten Free Office Vegan Food 100 Calorie Snack Pack, 0.9oz 10 Pack

$12.72 (as of March 30, 2026 02:16 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

50 Bags Hyssop Dried Herb Hyssop Tea Herbal (Hyssópus Officinális) - 50 Count 1.5 g Tea Bag Herb Hyssops Hissop Hysopp Hisopo

$16.99 (as of March 30, 2026 02:16 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Green Onions (Scallions), One Bunch

(as of March 30, 2026 02:16 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Post Comment