Why Avantis Global Small Cap Value ETF’s Insane 23% Cash Flow Yield Could Be the Hidden Goldmine Investors Are Missing Right Now

Ever had one of those weeks where work just keeps piling on and your thoughts start doing the mental equivalent of a broken record? That was me recently — stuck in a loop of restless thinking until a fascinating insight struck me like a lightning bolt. It revolves around a concept John Huber laid out about “quiet compounders,” companies that don’t boast explosive growth or astronomical returns on capital yet quietly churn out value consistently. Imagine a stock that doesn’t rally with headlines or market hype — it stays under the radar, trading at a dirt-cheap valuation but still returning a staggering 20% annually. Sounds like a dream, right? But here’s the catch: the market won’t always notice, and the stock will just keep compounding quietly in the background, fueled by stable free cash flow and share buybacks.

Now, here’s a kicker — what if your stock never “goes up” in price for the next couple of decades? Would you still hold on? That’s the tough question Charlie Munger’s inversion technique nudges us to ask. Because the truth is, if a business generates enough cash and reinvests it wisely through buybacks, your stake can grow without the need for flashy price appreciation. It’s not just a theoretical puzzle. This skepticism sparked a deeper dive into Avantis Global Small Cap Value ETF’s strategy, which surprisingly mirrors Huber’s idea. This ETF targets thousands of smaller companies that trade at unbelievably low price-to-cash-flow ratios, hinting at an underappreciated goldmine of value.

So, are we looking at a hidden moat where silent value compounding is at play? Or is this just another case of “value traps” dressed up in alluring metrics? Stick with me as we unpack the numbers, the philosophy, and the intriguing possibilities behind investing in these quietly profitable yet overlooked stocks. If you’ve ever wondered whether it’s better to chase growth or bank on steady, under-the-radar cash flow, this exploration might just flip how you think about value investing.

img#mv-trellis-img-1::before{padding-top:43.307086614173%; }img#mv-trellis-img-1{display:block;}img#mv-trellis-img-2::before{padding-top:30.271084337349%; }img#mv-trellis-img-2{display:block;}img#mv-trellis-img-3::before{padding-top:73.540856031128%; }img#mv-trellis-img-3{display:block;}

I did not have a good week at work. Whenever I struggle with work and have no one to confide to, there are usually some random thoughts. Sometimes they just keep repeating and repeating. This is when I realize that I need to sit down and spend some time to process.

It is about how similar John Huber’s illustration is with Avantis Global Small Cap Value UCITS ETF (AVGS).

John Huber’s post on quiet compounders tries to bring to our attention that you don’t always need a company that earns a high ROIC or ROE. The sort of high profitable companies that can compound wealth over the long term. If you find one (and it is a real one), then you can buy and don’t look for a long time. But they don’t trade cheap usually (because market is pretty efficient. If they have durability, you would not be the first or only person to know.)

He shares about the companies… that does not really have growth, but trades at tremendously attractive valuation:

Consider the following:

- A durable, mature company that trades at 5x FCF

- The FCF is stable but will never grow (0% growth forever)

- The P/FCF never moves higher (it will always stay at 5x)

The result of this stock is it will return 20% annually forever.

But, the real beauty of this 20% FCF yield setup that I think is underappreciated by investors and management teams alike is this: you don’t need to care about what the market thinks about your stock. You control your destiny. The multiple doesn’t need to move higher if the stock is that cheap. The share price will rise at 20% per year if the valuation stays at 5x FCF, the FCF is stable, and the FCF is used to buy back shares.

This is very simple math, but I’ve noticed that many management teams focus too much on how to “get the story out”. The cheap stock is not a problem, but in fact is a gift horse.

What if the Stock Does Not Get the Attention from the Markets?

Charlie Munger teaches us to always invert, which means don’t just look at what you want but that you can learn about conviction, or how things played out if you look at the opposite of what you want.

What most of us want is the value of our shares to appreciate.

But what if the premise is that the business has no growth?

That would be your fear. Why would you want a stock if it does not appreciate for the next 20 years?

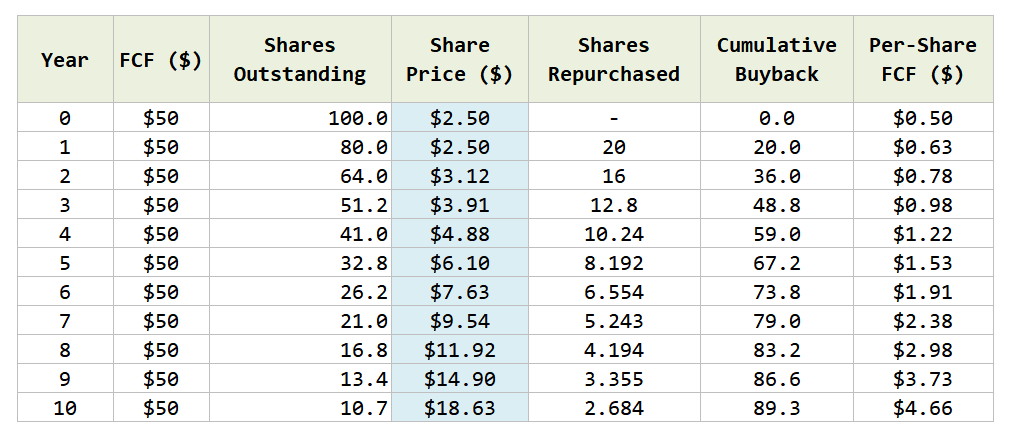

I asked ChatGPT to help me model what Mr Huber presented: If we have a business that trades at 5 times FCF today. Our assessment is that the business is stable to give the FCF yield but it will never grow (0% FCF growth forever). If the Price to FCF remains consistent and the business takes whatever they earn to buyback the shares, what will happen?

Uncertainty will make us wonder if a business can have stable FCF for 10 years but if our assessment gives us quiet confidence that it can, then what happens if the stock yield so much and is so neglected?

If the company consistently takes its 20% FCF yield and buyback its own shares, the Free Cash Flow (FCF) per share grow from $0.50 to $4.66 or 9 times in the 10 years.

Now in what fxxk would would people in the public markets not notice that?

Mr Huber may have a few points:

- The key difference compare to asset-based business is that the value company is profitable.

- Even without growth, value is value.

- But only if the business show some sort of intrinsic value that outweighs the price. The most difficult judge is not the stuff you can value today (e.g. properties relative to the price they traded at), but what people find it hard to judge over time.

- The price can don’t move, but if you keep churning out cash flow after cash flow, and you don’t make stupid decisions over its allocation, sooner or later some fxxker is going to notice.

Why not pay out the 20% yield as dividend?

Ask yourself where would you get a better yield then….. a 20% FCF-yielding business?

That allocation is probably the simplest.

Does Businesses like that Exists?

Mr. Huber’s example looks pretty fairy tale until you realize that is the job of an investor. If it is so easy to know a business has a 20% FCF yield, and can last 10 years, would that trade at that price?

It is usually not so easy to figure out until in hindsight.

It is possible for FCF to remain relatively the same with low growth.

For some reason, Mr. Huber’s post made me think about the Avantis Global Small Cap Value ETF Strategy.

If you recall from my post, Avantis starts their process by asking what would help us find stocks with higher expected returns in the future:

And the research triangulates to smaller companies that ranks higher in operating cash flow (less interest) that don’t trade too expensive.

By that virtue, it eliminates a key downside: Companies that potentially are more value traps with low profitability.

It at least moves us closer to companies with FCF but questionable growth. But is the FCF attractive enough?

Morningstar gives us a snapshot of the aggregate valuation and growth metrics of the 1347 stocks that form the fund:

Category Average is Global Small/Mid Cap Equity and Index is the MSCI World Small Value NR USD.

The portfolio is cheaper by value, lower in price-to-book, price-to-sales, price-to-cash-flow and has higher earnings yield.

Particularly, the price/cash-flow is intriguing low at 4.3 times. This is the operating cash flow estimated of each stock, then aggregated together. This is not free cash flow, which is taking the net cash from operations deducting away the capital expenditure.

But I feel it is good enough.

In their assessment of profitability, Avantis uses operating profit less off the interest expense, divide by book value.

To let you size up this 4.3 times, the IWDA (MSCI World) has a price to cash flow of 13 times.

4.3 times translates to a cash flow yield of 23%. Now i am sure that FCF yield is much lower.

I get the argument that the growth rate of this 1347 stocks is less than the others.

But what if we invert and assume that we buy these 1347 stocks and they don’t go up in price as a collective.

Then what happens to the 23% yielding cash flow?

Okay, even if that is too crazy, remember that the aggregate earnings yield is almost 9.3%.

As an aggregate, these business are not your asset attractively cheap no earnings/cash flow business but with cash flow.

Would the cash flow just disappear? Has to go somewhere right?

If you speak to my friend Ser Jing, he as his eye less on the stock price of this holdings but how much gross profits all the stocks in his Compounder fund generates.

And this is where you ask yourself if you own 10 stocks, and their aggregate earnings yield is 9.3% or aggregated cash flow yield is somewhat close to that, diversified across not just one industry, a few regions, how worried should you be if the prices languish for a couple of years?

What John Huber, Tobias Carlisle would like to tell us is that value can don’t work for the next 10 years, but that is not the only return we get, and the more concrete return is the aggregate cash flow we earn by waiting in the fund.

They should pile up.

If you are a dividend investor who has received 8 years worth of 5% dividends, you should kind of get it. You should also kind of get that markets are fairly efficient that the market will eventually realize it.

The more cash accumulated the bigger the value gap and the more absurd it gets.

i think this is my interpretation of the concept and as a collective, the management of the 1347 stocks are not going to make the better capital allocation decision of one good company management team.

The returns are more blunted for an index.

But you also have to be aware: That one company’s FCF may not be that sturdy for 10 years.

And this is the advantage of the collective cash flow of 1347 companies at 23% (even though that is operating cash flow).

Perhaps tomorrow we will talk about small US banks.

If you want to trade these stocks I mentioned, you can open an account with Interactive Brokers. Interactive Brokers is the leading low-cost and efficient broker I use and trust to invest & trade my holdings in Singapore, the United States, London Stock Exchange and Hong Kong Stock Exchange. They allow you to trade stocks, ETFs, options, futures, forex, bonds and funds worldwide from a single integrated account.

You can read more about my thoughts about Interactive Brokers in this Interactive Brokers Deep Dive Series, starting with how to create & fund your Interactive Brokers account easily.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith’s current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

Sleek Socket Original & Patented Flat Ultra-Thin Outlet Concealer with Extension Cord Kit, Multi Outlets Power Strip, Ideal for Home Improvement, Hide Bulky and Messy Cords, 3ft

$18.66 (as of March 27, 2026 02:19 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Purina Fancy Feast Grilled Wet Cat Food Seafood Collection in Wet Cat Food Variety Pack - (Pack of 24) 3 oz. Cans

$22.86 (as of March 27, 2026 02:14 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

BABORUI 2Pack Blue Interactive Cat Toy Ball - Automatic Interactive Cat Toys for Indoor Cats with 3 Tails, 2 Speeds Rechargeable Enrichment for Small/Medium/Large to Keep Them Busy

$8.48 (as of March 27, 2026 02:14 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Ameritex Waterproof Dog Bed Cover Pet Blanket for Furniture Bed Couch Sofa Reversible

$7.49 (as of March 27, 2026 02:17 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Post Comment