Why PayPal’s Explosive 13% Buyback Is Lurking in the Shadows—and What It Means for Your Wallet Today

Ever found yourself riding the rollercoaster of a stock you were pretty sure was a solid bet—only to see it nosedive and make you question every move? That’s exactly the story with PayPal lately. Back in September 2025, I penned an article when the stock was cruising at $70. Fast forward, and it’s plunged to $44. Ouch. With my average cost sitting at $82, that’s a brutal 46% hit. So what happened? Well, a change in leadership, cautious guidance, and a market riddled with skepticism about PayPal’s new CEO Enrique Lores—pulled from HP, no less—have investors scratching their heads. Is this the beginning of a payments giant’s downfall, or just a rough patch before the rebound? Let’s dive into how PayPal’s valuation, cash flow yields, and share buyback strategies paint a picture far more nuanced than just ‘dead in the water’. Buckle up—this tale might just surprise you. LEARN MORE

img#mv-trellis-img-1::before{padding-top:48.4375%; }img#mv-trellis-img-1{display:block;}img#mv-trellis-img-2::before{padding-top:13.76953125%; }img#mv-trellis-img-2{display:block;}img#mv-trellis-img-3::before{padding-top:69.296375266525%; }img#mv-trellis-img-3{display:block;}img#mv-trellis-img-4::before{padding-top:65.985576923077%; }img#mv-trellis-img-4{display:block;}img#mv-trellis-img-5::before{padding-top:33.736153071501%; }img#mv-trellis-img-5{display:block;}img#mv-trellis-img-6::before{padding-top:56.432748538012%; }img#mv-trellis-img-6{display:block;}img#mv-trellis-img-7::before{padding-top:52.63671875%; }img#mv-trellis-img-7{display:block;}img#mv-trellis-img-8::before{padding-top:52.63671875%; }img#mv-trellis-img-8{display:block;}img#mv-trellis-img-9::before{padding-top:52.63671875%; }img#mv-trellis-img-9{display:block;}img#mv-trellis-img-10::before{padding-top:53.02734375%; }img#mv-trellis-img-10{display:block;}

My PayPal article was written in 1st Sep 2025 when it was at $70 and today it sits at $44 bucks.

So that has not worked out for me. My average cost is higher at $82 so this has been like a 46% loss to me.

The stock dove after the last quarter’s earnings results because the guidance was cautious. Different stocks react differently to this but the impact is greater when the previous CEO Alex Chriss was always so optimistic and then we have this. I said previous because Alex has departed and replaced with CEO of HP Enrique Lores.

The market is rightly skeptical whether Enrique is the right person for a payments company that have missed opportunities and left us with a lot of “what it could have been”.

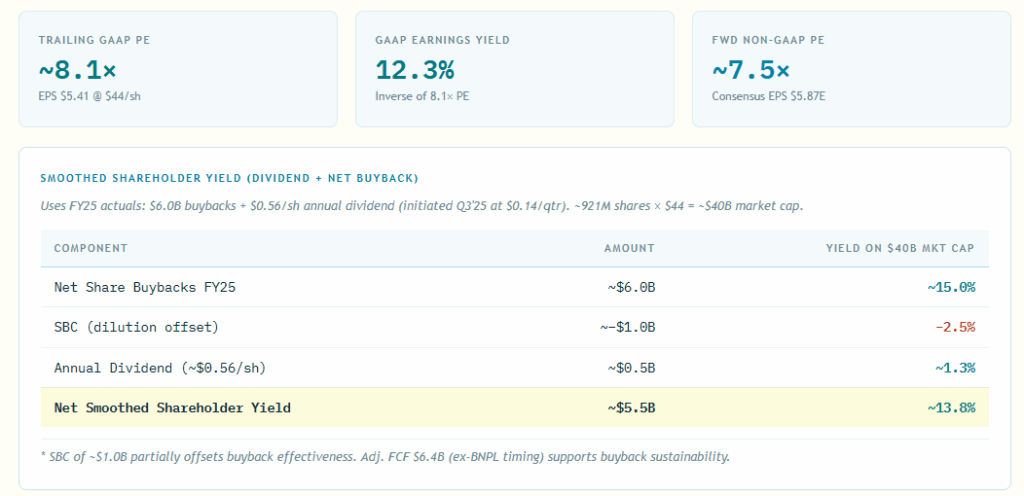

If the Price Is Cheap Previously its Even Cheaper Today

6 months ago, PayPal was trading at 7.2% earnings yield or 13.8 times PE. The free cash flow yield (express via buyback amount) is 8.5% and if less the stock-based compensation is 7.1%.

The EPS numbers is a little off but it won’t be too far from the valuation. In a way, PayPal is currently value like next year this earnings is going to get cut again.

The table below shows the dividends and net share buyback for one year. Usually, companies use their free cash flow to buy back their shares but in some cases, the buyback includes cash so this smoothed shareholder yield is good info but we got to take it with a pinch of salt.

If you look at HP’s share buy back, we can kind of figure out that may not be what new CEO Enrique has in mind. He might really be in to turn it around by rejigging it.

Since PayPal is net cash by a little its yield based on its enterprise value is quite close.

In a way, a high PE price it for its great growth prospect and a lower PE priced it as if it is going to die.

PayPal Hasn’t Actually Died Yet

The thing is it doesn’t look like its died yet just that all the hopes of returning to higher growth has evaporated.

Here is the historical earnings growth rate:

- 20-years: 15.3% p.a.

- 10-years: 18.4% p.a.

- 5-years: 8.9% p.a.

- 3-years: 37% p.a. (this was due to low base and buybacks)

The consensus 3-year forward earnings growth rate: 13.4% p.a.

Well if they actually can grow its very good already!

The consensus future FCF estimate:

- FY2026E: 5 – 6 billion

- FY2027E: 5.5 – 6.5 billion

- FY2028E: 6 – 7 billion

I don’t know man if it is dead why are they still estimating the FCF to be like this. If FCF (maybe less SBC) is 4-5 billion its 10-13% FCF yield.

PayPal’s Share Buy Back History

This chart shows PayPal’s history of share buy backs versus the number of shares outstanding. We observe that the share count remains consistent, most likely because it balances share dilution from compensation. It is only recently that we see the share count dip.

Industry Valuation.

The table below show us how PayPal currently values relative to its other Payments peers:

Market is Pricing PayPal for Stagnation or Decline.

At a current 12-13% free cash flow yield, market is valuing PayPal with the following story:

- If PayPal exits at 10 times FCF with zero growth, the implied free cash flow yield is 10%. PayPal’s 12-13% is not far off but its really valuing at no growth but also a lower price earnings.

- If PayPal is valued at a 5% free cash flow decline till perpetuity with it always valued at 12 times free cash flow, the implied free cash flow yield is 8.3%. If it trades higher than that, it kind of makes you consider that free cash flow decline scenario.

Share Buy Back’s Boost to PayPal’s Share Price Imagination: What if Free Cash Flow (less Stock-based Compensation) decelerates and Market Values PayPal at 10 times PE?

We can put out a table to show how the share price will change from $44 if we take all the free cash flow less share based compensation to buy back its shares, reducing number of shares outstanding.

The less shares outstanding, the more money shared among existing share holders. The Market Cap will stay the same, but the share price will be boosted. Observe the FCF-SBC just keeps going down.

I think its hypothetical which is why the price is shown as $54 instead of $44 because PayPal is currently valued at lower than 10 times.

The last time they were at $100 was in 2022, and if this happens the share price would go back there in 8 years time.

What if Free Cash Flow (less Stock-based Compensation) decelerates even more?

We model the same thing but if the FCF decelerates at 10% instead of 5%.

In a way, the share price still grows, just that it takes longer to go back to $100.

What if Free Cash Flow Decelerates at 5% but Market Rates it at 13 times PE?

I tried to see what if the market actually values a payments company higher at 13 times. If you look at the PE valuation of the other players, 10 times is a really low bar.

It is actually better.

What if Free Cash Flow Decelerates at 5% but Market Rates it at 8 times PE?

And also what if market still only rates PayPal at current 8 times PE?

Well this is the closest scenario currently, and the thing is the price still grows.

Epilogue

I think no one dares to touch PayPal now. It has a really toxic narrative.

What I tried to model is that if what they say is true, then would there be a positive outcome? I think there will. We haven’t even talk about what if they go net debt and buy back.

The company can last less than 15 years but you might get some outcome.

But then again, maybe they won’t even buy back at all. Maybe there is a room to grow. Which is a positive thing because it means its exit valuation may be higher than 13-15 times PE.

The company can self destruct and waste those free cash flow as well.

If you want to trade these stocks I mentioned, you can open an account with Interactive Brokers. Interactive Brokers is the leading low-cost and efficient broker I use and trust to invest & trade my holdings in Singapore, the United States, London Stock Exchange and Hong Kong Stock Exchange. They allow you to trade stocks, ETFs, options, futures, forex, bonds and funds worldwide from a single integrated account.

You can read more about my thoughts about Interactive Brokers in this Interactive Brokers Deep Dive Series, starting with how to create & fund your Interactive Brokers account easily.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Fee-only Wealth Advisory Firm Providend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith’s current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

Apple iPad Air 13-inch (M4): Liquid Retina Display, 256GB, 12MP Front/Back Camera, Wi-Fi 7 with Apple N1, Touch ID, All-Day Battery Life — Space Gray

$839.00 (as of April 12, 2026 02:24 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Bolux Dog Harness, No-Pull Reflective Dog Vest, Breathable Adjustable Pet Harness with Handle for Outdoor Walking - No More Pulling, Tugging or Choking (Blue, S)

$10.07 (as of April 12, 2026 02:31 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Amazon Fire TV Stick 4K Max streaming device, with AI-powered Fire TV Search, supports Wi-Fi 6E, free & live TV without cable or satellite, find shows faster with Alexa+

$39.99 (as of April 12, 2026 02:24 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Fresh Roasted Coffee, The Great Eight, Flavored Coffee Pod Variety Pack, K-Cup Compatible, 96 Count

$34.98 (as of April 12, 2026 02:24 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Post Comment