Why Private Equity and Credit Investors Are About to Face a Shock They Didn’t See Coming — And How to Prepare Now

Ever wonder why so many investors get cold feet about fixed income investments, even when they plan to hold them to maturity? It turns out, not all bonds—or private investments for that matter—are created equal. Without a solid grasp of the risks involved, what looks safe can suddenly feel like walking a tightrope without a net. And let’s be honest, expecting your financial advisor or portfolio manager to foresee market storms is like waiting for a walkie-talkie call from Donald Trump to halt chaos—highly unlikely! The real magic of a good adviser? Helping you sift through the noise, align your expectations with reality, and embrace the uncomfortable truth that investing isn’t always smooth sailing. This article dives deep into why private investments, despite their appeal, often leave investors caught between comfort and chaos, examining recent shocks in the market and what they reveal about risk, reality, and resilience. Ready to face the gritty truths behind the dazzling returns? Let’s get into it. LEARN MORE

img#mv-trellis-img-1::before{padding-top:43.9453125%; }img#mv-trellis-img-1{display:block;}img#mv-trellis-img-2::before{padding-top:87.809523809524%; }img#mv-trellis-img-2{display:block;}img#mv-trellis-img-3::before{padding-top:114.54138702461%; }img#mv-trellis-img-3{display:block;}img#mv-trellis-img-4::before{padding-top:149.92679355783%; }img#mv-trellis-img-4{display:block;}

I wrote about our unwillingness to learn about things, that may eventually be life changing a few days ago and my friend was curious about why the investors in my article would be worry about duration. By right, if have an idea that you want to hold a fixed income to maturity, then why would there be a worry?

I explain to my friend that you are right, but the issue is that if you are ill-equipped with fixed income knowledge, in your eyes fixed income may look the same.

You can’t tell the riskiness of one from the other. Or how to frame riskiness.

My point is without that baseline, you will have “this” expectation of how your investing experience with this fixed income is, but you may get a bloody shock when “the” reality is entirely different.

You can blame the adviser, or the sales rep selling to you but in a way you got to take some responsibility for your lack of sophistication causing that gap in expectation.

The more sophisticated investor would know that there is no free lunch. You are taking on some sort of risk in the hopes that the return is worth it. And you are trying to find people that can manage the risk. You are also trying to find people that are very familiar with the investing experience so that they can explain to you how you should look at what transpired that are related to your investment along the way.

The last point to me is the real value of paying that 1% p.a. advise fee to an adviser.

Not the returns because eventually what you will earn is a range of outcome based on the kind of risk that you take and the bloody adviser, nor the investment manager who decides the portfolio have no control over.

It is as if the investment manager can give a call to Donald Trump and stop all this. You will also know that your investment manager has no power over that but you have this expectation that he would be able to “sense” or “know” these things earlier than you.

If you are with a good adviser, some of the uncertainty about how you invest, what you invest in, what you hear in the media you should concern with, what you hear in the media you should concern with less, these should clear up.

So what is left is higher conviction to funnel money into your investments to build wealth.

And uncomfortableness.

The uncomfortableness doesn’t really go away and the process to build some real wealth will involve some of this.

There are people who didn’t realize that uncomfortableness doesn’t go away but seek out the investments that don’t have this attribute.

And they end up with the same issue, a big gap in investment reality vs expecations.

A favorite in recent times is private investments.

This reader that wrote in to Ben Carlson on A Wealth of Common Sense may emphasize this:

My financial advisor has me in alternative assets (PE, VC, Private real estate, private credit, etc.). About 40% of my total investable assets (more in brokerage than IRA). I understand the assets – many are semiliquid or illiquid. I’m more interested in what is a reasonable proportion to hold. I am in my mid 40s. Looking to retire in a decade-ish.

You will feel comfortable until… it becomes uncomfortable.

The more concentrated you are the more feelings will be amplified.

The bankers really like to sell the idea that now a proportion of your wealth should be in these private investments because:

- Returns are higher than traditional.

- They are not volatile so with them in your portfolio, your portfolio is more stable.

The first one is debatable already. You might want to read what Dimensional’s research on this came up with.

We are not saying that they are not good or good but that what drives returns is the same dynamics. You might be taking on more risks that the level that you wish.

It is also that they can be quite volatile if the private investments end up being traded:

Someone is Preventing You to Be More Comfortable with the Volatility of Investments.

And the person might be yourself because you see volatility as a flaw and you only want to see the reward.

When your banker or financial representative explain the investments to you, you become more interested because the returns look so appealing.

There is a way to sell by emphasizing on the features you are comfortable with, but diluting or playing down the negative aspects of the investment or strategy. Or totally don’t mention the negative features.

You can say the representative has no ethics but I have a nuance view:

If it were to me, I would also not tell you everything upfront but only after you invest for a while. This is because if I unload all the features you need to know about the investments, you won’t be able to decide, you won’t buy in the first place. There are some lessons that are better learn after you invest along the way. It would be better we unfold as you experience it.

An unethical financial representative can say the same thing no doubt.

But it is what makes sales and advice challenging through the eyes of the person needing advice.

It is why many got comfortable with private investments because they think that they have access to world class managers. The more sophisticated ones know that not all private funds make money and the returns are skewed heavily to the funds that are difficult to get into.

But you will eventually feel uncomfortableness somehow because this is a feature regardless is world class or not world class funds.

BlackRock Curb Withdrawals from its Flagship Private Credit Fund.

So a reputable manager BlackRock decide to curb withdrawals from a US$26 billion HPS Corporate Lending Fund (HLEND). This is an unlisted BDC or business development company. The private credit shareholders requested for 9.3% of their shares.

BlackRock said the step is in line with its existing management of liquidity for the fund and a “foundational” feature of the fund.

Shares of BlackRock fell 6.7%

The thing is that HLEND capped redemption at 5% of NAV per quarter. This is not a unique feature only to HLEND but it is pretty prevalent in these private investments.

The question is WHY are people suddenly pulling money out of a very significant reputed private credit fund.

Is it that they know some stuff that you don’t?

Why is this making the news?

This is the real uncomfortableness.

What is Going on at Market Financial Solutions (MFS)

BlackRock HLEND is this few days, but a couple of weeks ago it was MFS in the news but how is it related to private investments?

Market Financial Solutions (MFS for short) lends money to those property investors that need bridging loans. These loans are short-term and high interest (say 0.4%-0.9% per month) so that they can buy buildings at auction quickly.

They announced record turnover and profits not too long ago.

But the people that fund MFS in their business Amber Bridging and Zircon Bridging call for the court to place them into administration based on them double pledging their assets. Take the same property assets as collateral to secure multiple loans from different banks.

This means they have about 930 million pounds of collateral shortfall which is about 80%.

Obviously this means there is a suspicion of fraud.

So if you lend to a business like that, MFS might wind down but how much would you get back?

The lenders that have exposure:

- Barclays PLC: About 600 million pounds.

- Atlas SP Partners under Apollo Global Management: About 400 million pounds. Atlas SP manages $40 billion so this is kind of like 1.3% of the entire book. Because you make a % of AUM fee, a 1.3% wipe out will just kill the profits for the year.

- Castlelake LP by Brookfield: About 400 million pounds. Castlelake has $33 billion so this is about 1.6% of their book.

- Jefferies: They also got caught up in the First Brands trouble. 100 million pounds. Jefferies 2025 net income is $631 million so they might take a hit again.

- Wells Fargo and Banco Santander: Not sure the amount.

FS KKR Capital Corp’s Dividend Cut

I am also seeing more news flow last week about private credit funds cutting their dividend payout:

FS KKR Capital Corp (FSK) declared in its February 2026 earnings call a first-quarter distribution of $0.48 per share, a significant drop from the $0.70 per share distributed just a few months prior. Management cited “specific challenges” with certain investments that impacted their bottom line.

Credit deterioration seem to have accelerated as well with its NAV falling $1.10 to $20.89.

Non-accruals, which are loans that are unlikely to be repaid easily within a 3 month span, expanded to 5.5% at cost.

Look… You are Lending Money or Investing in More Risky, and Smaller Businesses.

I am not sure if you realize this.

Maybe I am not good with words but that is the crude way of putting it.

In the past businesses like MFS and First Brands, Tricolor, those who have fraud or defaulted would be listed on the public markets as micro-cap or small cap companies. But with so much money out there, they end up staying private.

But the reality is that business do go through tough times and some eventually fail.

When recession comes, some businesses just felt it more and some eventually thrive but others fail.

Those who lend money to these businesses might not get back their money or get back a fraction. Some would end up with the company itself (since the assets of the company are collateral)

The difference is that you think some manager have a knack for picking and incubating companies better.

The difference is that when you own a fund, you hold a diversified portfolio of them.

The diversification helps to a certain degree to harvest an eventual return (but may not be eventually appealing to you), and it would save you from impairing all your money.

But when peeled back, you are investing in these smaller businesses and that is what it comes down to.

Your Investments Might Eventually End Up Okay…. but

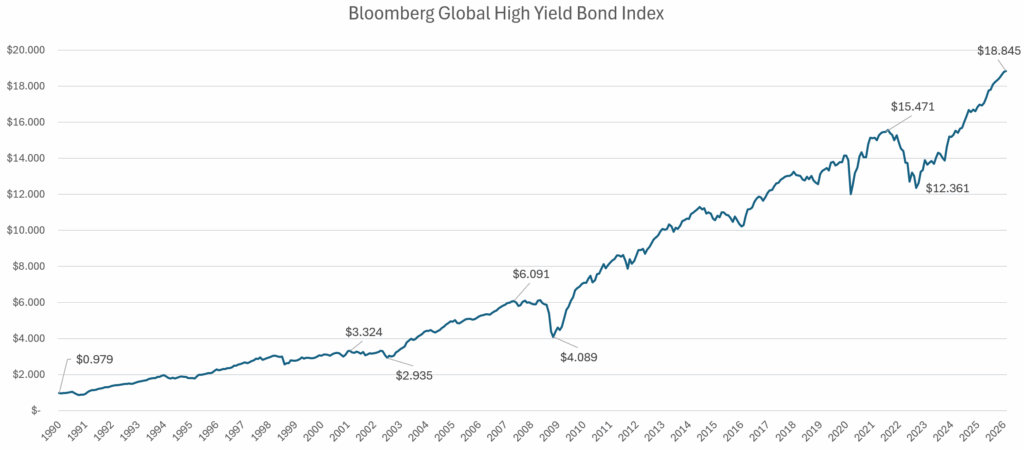

I am going to show you how $1 invested in a Global High Yield Bond Index since 1990 will be:

It looks good. The $1 million becomes $18 million.

High yield bond is also known as junk bonds or the IOUs that are less than investment grade.

The compounded return is 8.46% p.a.

Its not bad and the person would have built wealth.

But the net asset value fluctuates and during the 2000-2003 period, GFC, Covid, there will be defaults.

Companies die.

The high yield bond since it is public will see its value being cut.

But you know the result today. It ends up higher.

But are there defaults then? Yes.

This chart shows the fixed income default rate based on credit rating. You can see during the Great Financial Crisis, the CCC has a 50% default rate. Same as during Covid (40%).

That is very high!

The B is 15% default rate.

You might wonder “Kyith, so how did the high yield bond index survive 40-50% of the fixed income default?”

Here is the allocation of the iShares Global High Yield Bond UCITS ETF based on credit quality:

- BBB: 0.55%

- BB: 63%

- B: 27.8%

- CCC: 7%

In a sense, the index is based on the degree of lending and so most of the lending is not so low quality then we think. Or in a way, perhaps you also don’t realize not all junk looks the same.

Companies like Tricolor, MFS who whether it is due to fraud or mismanagement would die.

There is a reason equity investing or lending is risky!

The Value of Your Investments might be $100,000 Today but Tomorrow it will be $0 if You don’t Mark to Market Frequently.

If the comfort that you are feeling is because the value of your investments doesn’t change much then eventually you will see things like this:

Read here.

Last time my reader told me about an European fund Aberdeen European Residential Opportunities Fund (AEROF) that gradually gets written down to zero.

This is not one thing written to zero this is the whole fund NAV write to zero.

This case is a classic private real-estate fund NAV cliff:

- NAV looked reasonable (around 50%) after write-downs.

- But once the manager assessed final liquidation values, the remaining equity was effectively wiped out.

The private fund was incepted in 2016 with a bunch of residential properties in UK, Sweden, Finland and Denmark.

Here is how the NAV go:

- Sep 2017: 100%

- Sep 2018: near 100%

- Sep 2019: above 100%

- Sep 2020: above 100%

- Sep 2021: near 100%

- Sep 2022: 80%

- Sep 2023: 40%

- Sep 2024: 30%

While it did not immediately go to zero, imagine this is your experience when you only received a fund update every quarterly.

If it Gets Worse, You Will Keep Seeing these in the Headlines as 2026 Progresses.

What I expect if it gets worse is that investors tries to redeem but cannot redeem.

My own brother reminds me of what happen during Brexit:

They key feature of a private fund is that they cant be forced to sell their assets due to redemption.

But we saw what happened during Brexit. They have open ended funds that hold property. Once the vote was known people started throwing redemption orders

Then the fund managers had to throw up gates

When all these settles, your investment might be mediocre but they would be okay. Just like the high yield bonds.

But in the meantime, you would be thinking “Is my private investments okay?”

You be checking with your bankers and your bankers would be assuring you.

You be checking with your friend.

You be checking with influencers.

The more concentrated you are the more you would check.

But All These are Normal

Why do I say that?

Businesses thrive but businesses also will fail.

It happens more in recessions. Recessions is when capital reallocation might occur.

If we have 100 years of investment returns data, do you think within that 100 years, there isn’t business failure and excesses in the market?

Sure have right?

If You Invested In Private Investments, How Would it Likely Turn Out?

What is the conclusion?

- Some funds would navigate these well, and in 20 years time you would wonder why you worried so much. Or that you would be glad the returns was decent but you lived through an unsettling period.

- You lived through an unsettling period and your fund did mediocre returns, not better than general equities.

- You liquidated your investment and lost money, just not all your money. And you lived through what I described in #1 and #2.

If the investments are properly diversified, you end up with 1-3.

And you will be like, “Wouldn’t that be just as uncertain?”

Well yes, it will be just as uncertain in public markets. If they tell you that the historical yield on a BDC is 14%, it doesn’t mean that this is what you will experience.

In a way, you rationalize a lot to yourself that what you see in the past is what you would eventually get.

But despite all this, we will have prospects and clients who come in and ask “What is the average return of your investment?” Like what the past clients enjoy they will also get it in the timeframe they evaluate their investment on.

You give yourself exposure to private investments, promise to lock up and don’t take out, and you hope for the best, hopefully doesn’t lose you money, and hopefully the return is like in the past.

But you will feel discomfort one way or another, especially if the public markets start going crazy.

What bankers would likely dilute the information that they give you is when things around is imploding.

Because you will get uncomfortable when you see more of this fund being market to market suddenly from 100% to 60% and you be wondering if your fund will do the same.

It might and might not and yes the private investment is “not volatile”, but you be playing mind tricks with yourself.

You can’t run away from discomfort.

In a way, you got to start an honest conversation with yourself about discomfort, uncertainty, and then consider if these are always going to be around, how should I plan my investment and my financial plan.

If you want to trade these stocks I mentioned, you can open an account with Interactive Brokers. Interactive Brokers is the leading low-cost and efficient broker I use and trust to invest & trade my holdings in Singapore, the United States, London Stock Exchange and Hong Kong Stock Exchange. They allow you to trade stocks, ETFs, options, futures, forex, bonds and funds worldwide from a single integrated account.

You can read more about my thoughts about Interactive Brokers in this Interactive Brokers Deep Dive Series, starting with how to create & fund your Interactive Brokers account easily.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Fee-only Wealth Advisory Firm Providend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith’s current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

IQBAR Clean Plant Protein Bars - Chocolate Lovers Variety - 12 Count - Keto, Vegan, High Fiber, Gluten and Dairy Free, Low Sugar Snack - Brain and Body Nutrients for Focus, Energy, Meal Replacement

$19.99 (as of March 30, 2026 02:16 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Bedsure Orthopedic Dog Beds Large Sized Dog - Washable Large Dog Cat Bed Waterproof, Comfort Dogs Couch Sofa with Washable Removable Cover, Pet Bed with Nonskid Bottom, Grey, 35"

$39.99 (as of March 30, 2026 02:20 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Bones Coffee Company Highland Grog, Butterscotch Caramel Flavored Coffee, Medium Roast Low Acid Arabica Beans Compatible with Auto drip and French Press Coffee Maker, 12 Oz Ground

$19.99 (as of March 30, 2026 02:16 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Unique Style Paws Dog Collar With Metal Buckle - Red Rose Flower Gift for Small, Medium, Large Boys Girls Dogs - Durable and Cute

$8.49 (as of March 30, 2026 02:20 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Post Comment