Winklevoss Drops a Bomb on JPMorgan’s Crypto Data Fees—Is This the Quiet War That Could Destroy Your Investments?

Ever wonder what happens when the giant of traditional banking decides to slam the door on fintech and crypto innovation? Well, JPMorgan Chase, the colossal American bank, just threw down a gauntlet that’s shaking the future of financial data access — and, frankly, it’s raising some serious eyebrows. Tyler Winklevoss, co-founder of Gemini, isn’t mincing words; he warns that JPMorgan’s new steep fees could cripple the very firms daring to disrupt finance and, worse, betray consumers’ rights to freely access their own financial data. Is this a protective move to curb data abuse, or is it a full-on siege to squelch emerging fintech and crypto competitors? As regulatory battles heat up and open banking hangs in the balance, the stakes couldn’t be higher — for innovation, competition, and who really gets to control your financial information. Dive in as we unpack this high-stakes tug-of-war where tradition meets the future, and find out why this could be a defining moment for the fintech revolution. LEARN MORE

Key Takeaway

Tyler Winklevoss, co-founder of Gemini, says JPMorgan’s new fees will cripple crypto and other fintech firms and betray consumer rights.

JPMorgan Chase, America’s largest bank, is drawing fresh battle lines in its long-standing feud with fintech firms over access to customer data.

Jamie Dimon vs. open banking

Seizing the opportunity during a potential regulatory rollback, JPMorgan CEO Jamie Dimon proposed charging steep fees to fintech firms for customer data.

This move, critics argue, could harm platforms like Plaid that bridge banks and crypto apps such as Gemini, Coinbase, and Kraken.

Among the most vocal critics is Gemini co-founder Tyler Winklevoss, who sees the move as a direct attack on innovation and a calculated effort to stifle competition.

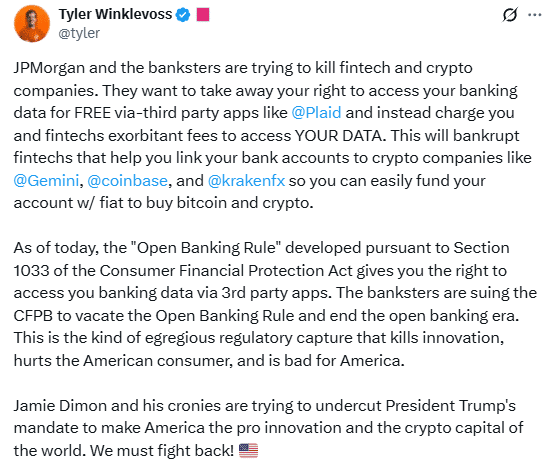

“JPMorgan and the banksters are trying to kill fintech and crypto companies.”

Source: X

The Consumer Financial Protection Bureau’s “Open Banking Rule” currently protects consumers’ rights to access their financial data for free through third-party apps.

But if it gets repealed, it’ll open the door for banks like JPMorgan to put hefty fees on this access, which is essential for consumers and data aggregators (like Plaid) alike.

Naturally, Winklevoss condemned JPMorgan’s move as a clear case of regulatory capture and an attack on consumer rights.

JPMorgan defends itself

JPMorgan, however, defended the move, with spokesperson Pusateri stating that the new fees aim to curb the overwhelming volume of data requests made by fintech firms, most of which, the bank claims, aren’t directly tied to actual consumer activity.

In conversation with Forbes, Pusateri noted,

“We receive nearly two billion monthly requests for customer data from middlemen, and more than 90 percent of those are unrelated to a consumer using fintech services.”

Critics, however, including Winklevoss, called this a textbook case of regulatory capture—where large banks influence rules to limit competition.

Winklevoss slams Dimon’s ‘anti-crypto agenda’

While JPMorgan claims the new fees are necessary to limit excessive data requests, critics see it as part of a broader attempt by traditional finance to tighten its grip on the evolving financial ecosystem.

Remarking on the same, Winklevoss added,

“Jamie Dimon and his cronies are trying to undercut President Trump’s mandate to make America the pro innovation and the crypto capital of the world. We must fight back!”

He also hinted that Gemini’s recent offboarding from the bank may have been retaliation for his outspoken criticism.

Still, he remains firm in his stance, vowing to continue pushing back against what he sees as anti-competitive practices.

He stated,

“Sorry Jamie Dimon, we’re not going to stay silent. We will continue to call out this anti-competitive, rent-seeking behavior and immoral attempt to bankrupt fintech and crypto companies.”

JPMorgan’s pro-crypto move

Interestingly, while battling fintechs on data access, JPMorgan has taken steps toward crypto adoption.

Reports suggest the bank plans to issue loans backed by clients’ crypto holdings, indicating a more complex approach than full-blown opposition.

Apple iPad Air 13-inch (M4): Liquid Retina Display, 256GB, 12MP Front/Back Camera, Wi-Fi 7 with Apple N1, Touch ID, All-Day Battery Life — Space Gray

$839.00 (as of March 27, 2026 02:14 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

UP URARA PUP Autumn Plaid Dog Collar and Bow Tie Set – Orange Yellow Checkered Adjustable Fall Collar with Maple Leaf Charm for Small Medium Large Dogs, Soft Cotton Pet Collars with Buckle and D-Ring

$16.99 (as of March 27, 2026 02:17 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Orange 78 in HILASON 1200D Winter Waterproof Poly Horse Turnout Blanket Belly Wrap

$98.95 (as of March 27, 2026 02:17 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Stainless Steel Cat Litter Box, Extra Large XL Odor Free Metal Litter Box with High Sides Lid, Open Top Litter Pan Include Scoop Easy Cleaning Anti-Scratch Kitty Cat Box Anti-Urine Leakage, Non-Sticky

$39.99 (as of March 27, 2026 02:14 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Post Comment