Unlocking America’s Banking Secrets: Why Your Wallet Could Be Losing—or Winning—Big Depending on Where You Live

Ever wonder how seasoned investors sift through the storm of fear swirling around financial markets to spot real opportunities? Well, this morning, as I was whipping up breakfast, I stumbled upon a goldmine – a candid interview with Derek Pilecki of Gator Capital on Value After Hours. Derek, a sharp value investor specializing in banks, insurance, and financials, unpacks some surprisingly optimistic takes amid current market jitters. From the reassuring quality of loan books in regional banks to the intriguing ways private credit buffers risk, his insights reveal a nuanced landscape that defies the usual doom-and-gloom headlines. Plus, the way he connects tangible book value growth and management’s strategic moves might just change how you look at banking stocks altogether. Ready to challenge your assumptions and maybe even spot a mispriced gem? Dive in for a whirlwind tour of financials with a twist. LEARN MORE

img#mv-trellis-img-1::before{padding-top:71.09375%; }img#mv-trellis-img-1{display:block;}img#mv-trellis-img-2::before{padding-top:71.09375%; }img#mv-trellis-img-2{display:block;}img#mv-trellis-img-3::before{padding-top:70.21484375%; }img#mv-trellis-img-3{display:block;}img#mv-trellis-img-4::before{padding-top:24.043715846995%; }img#mv-trellis-img-4{display:block;}

I woke up this morning to prepare breakfast and saw this Derek Pilecki interview about long/short financial investing, regional banks, non-banks and insurance on Value after Hours:

Derek runs Gator Capital and he focus on value investing in banks, insurance and financial related companies so its interesting to hear his comments about different things.

A few short conclusions from the video:

- There is a lot of fear but private credit lending actually segregate and help the mid and small size banks in taking on the more risky loans.

- The lending to private credit is usually done by the larger banks and in a way, they have two levels of vetting. The private credit will vet the borrowers while they vet the private credit firms they lend to.

- Derek met with 10 banks at a conference and nobody is concern about credit quality. It leads Derek to the idea that last time there would be some concern but in the last few years, the credit quality is top notch. He had a conversation with an M&A person and it used to be that 1 out of 3 prospective banks have loan books that are well organized, clear and good quality that makes that an attractive target. But now almost all the banks he come across are good because of the standardization.

- Derek says that quality is good but despite that you would have the usually business cycle challenges with housing markets but it would not be as bad as 2006 due to much better lending standards.

- Follow the growth in tangible book value per share. If that goes up over time, the share price usually follow.

- The large US banks are expensive.

- You can find mid and small banks that trade at 8 times PE when they usually trades at 10-14 times. Derek finds that mid and small banks used to be expensive in the 2017/2018 and he own none. Currently, he finds this space mispriced.

- Not all banks focus on ROE. Banks can do mindless expansion without a care of how well their ROE do.

- The smarter managers will reconfigure the banks by pulling back capital from areas that are not worth it to concentrate on areas that would grow ROE.

- The best combination is when you have something that trades severely below book value and the guidance is for ROE to grow by 1-2%. It will even be better that the company gives an indication that that they are going to buy back shares. The growth in ROE signals that management has a plan, or at least a view that earnings/revenue in a very traditional business can be improved in the near future. If your ROE is 10% and your bank stock is trading below book value, say 0.5 times it means $1 invested in the equity earns 20%. So when the bank takes their resources to buy back their shares, its like each share earns 20%, and set to grow since the management gives guidance. These companies can grow like a SAAS companies when done right.

- Some indications may also be that the management decides to get into asset management business.

- The 2 ends or the line of the yield curve to watch for is the 3-month and the 5-year because the former is what they borrow at and latter is what they lend at. If the plan is for 2 to 4 rate cuts then that would lower the short by 0.5% to 1%.

- Current 3-month US is at 3.68% and 5-year is at 3.52%.

- If the 3-month get lower the steep yield curve helps the net interest margin.

- #12 basically states the tail wind for the short end but since the lending tenure is 5 years, those loans 5 years ago have to be refinance now at a higher loan rate so this helps the NIM as well (but the volume is another matter altogether.

- The 5-year US rate in Mar 2021 is 0.79% so think of it now resetting to something closer to 3.5%.

- In the insurance front, casualty insurance costs have been a headwind and it is proving challenging.

- Derek says financial advisory business at the right price is something that not many people notice. Names in this space to look at are LPL Financial (LPLA), Raymond James (RFJ) and Ameriprise (AMP). AMP looks real cheap.

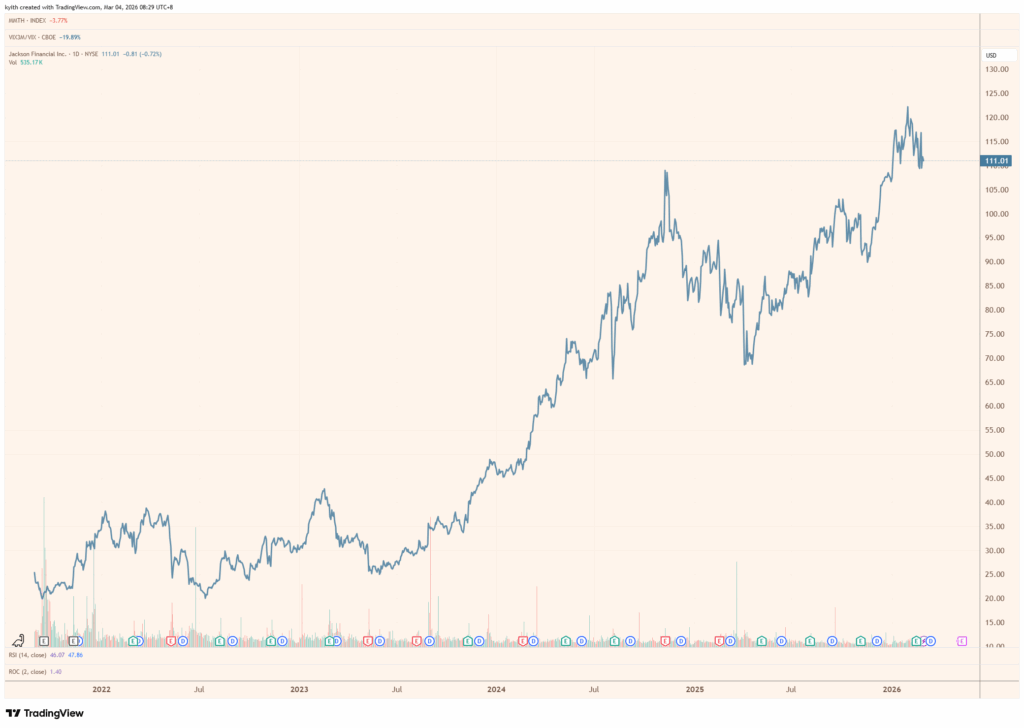

- Another money printing business highlighted is Jackson Financials who was spun out from Prudential and it is a pure play on fixed-indexed annuity which are attractive to retirees. It is a play on the aging part of America.

Hope this is helpful.

Some charts of what is mentioned.

Jackson Financial (JXN)

About $10 billion in Enterprise Value. Debt stayed constant for the past 3 years but in the last 3 years they added $1 billion and $2 billion in cash without much change to the structure.

Ameriprise (AMP)

About $38 billion in Enterprise Value with net cash of $4 billion. 13 times PE leans towards the lower bound of last 10 year’s historical PE.

Yield curve currently compare to 5 years ago:

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

I break down my resources according to these topics:

- All my personal notes about how my philosophy behind my own money and how I manage it.

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I used to work doing research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

- Havend – Where I currently work. We wish to deliver commission-based insurance advice in a better way.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Fee-only Wealth Advisory Firm Providend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith’s current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

ARM & HAMMER Clump & Seal SLIDE Platinum Multi-Cat Clumping Cat Litter, Easy Clean Technology with No Scrubbing, 14-Day Odor Control, 18 lbs

(as of June 24, 2026 02:33 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Roku TV Remote Control (Official Manufacturer Product) - Simple Setup, & Pre-Set App Shortcuts - Replacement Remote Compatible with RokuTV Models ONLY (Not Roku Players)

(as of June 24, 2026 02:48 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Samsung 43-Inch Class Crystal UHD U8000H Series Samsung Vision AI Smart TV (2026 Model, 43U8000H) Crystal Processor 4K, Endless Free Content, Motion Xcelerator, Color Booster, Alexa Built-in

$247.99 (as of June 24, 2026 02:54 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Apple iPad 11-inch: A16 chip, 11-inch Model, Liquid Retina Display, 128GB, Wi-Fi 6, 12MP Front/12MP Back Camera, Touch ID, All-Day Battery Life — Blue

(as of June 24, 2026 02:48 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Post Comment