The Hidden Factor That Can Make or Break Your Financial Security—And It’s Not What You Think

Ever wondered how to spot hidden defects in a second-hand monitor when you can’t even power it on? Sounds like a quirky question, right? Well, it caught me off guard too during a recent meetup with a long-time reader. It’s funny—while some might obsess over every little detail, I’ve been quite lucky (or maybe just careless) buying cheap monitors without a second thought, often skipping any serious inspection. That chat over kopi turned into something much bigger, leading us down the rabbit hole of shield plans, healthcare needs, and the tricky realities of navigating insurance claims and medical care. Because at the end of the day, whether it’s tech gear or healthcare coverage, understanding what truly matters—and having the right perspective—can make all the difference. Curious? Let’s dive in. LEARN MORE

img#mv-trellis-img-1::before{padding-top:41.666666666667%; }img#mv-trellis-img-1{display:block;}img#mv-trellis-img-2::before{padding-top:24.043715846995%; }img#mv-trellis-img-2{display:block;}

I met up with one of my long-time readers yesterday.

He asked me a question that may seem perfectly normal to many of you, but caught me a little off guard. If you buy second-hand monitors, how do you check if the monitor has lines — especially if you cannot power it on?

I never had that problem… because I never checked.

There’s something quietly embarrassing about admitting that. When each monitor costs $20–50, you just live with your luck. By the law of large numbers, most monitors turn out fine. Even among the maybe 60 I’ve bought over the years, the ones that broke down after purchase were a small minority — and almost none of them had line issues. Most sellers would tell you upfront if there were lines.

So I did what felt natural: I just gave him my Dell QHD 2K 27-inch monitor.

I’m not entirely sure why it felt so easy. Maybe it’s because I’ve accumulated enough of these things that one monitor doesn’t feel precious. Or maybe it’s because when someone has been reading what you write for years, quietly following along, something about that feels worth honouring in a small, tangible way.

He had to have lunch with his daughter afterward, so we could only squeeze in a quick kopi near my place.

Sometimes I ask myself — what is a fair exchange in these meetups? I genuinely don’t know. What I do know is that what I walk away with from these sessions is something I couldn’t easily find anywhere else: unfiltered, lived experience. The kind that doesn’t get written up in articles or discussed in forums.

Our conversation eventually pivoted to how to think about shield plans. He had been watching and reading what Havend put out — particularly what Eddy spoke about. Based on all that, he’d formed a pretty thoughtful view of the key considerations. But if I understood him correctly, his frustration was that the really critical points weren’t being surfaced clearly enough. Not just by Havend, but by most people covering the topic.

I told him what I genuinely believe: different people come to a subject with wildly different levels of existing knowledge. Not everyone can easily zoom in on the one or two things that actually matter most. And without that, most people will quietly walk away with the wrong conclusion — not because they weren’t trying, but because no one handed them the right lens.

The main consideration, beyond how wealthy you are, is how deeply you understand your own potential healthcare needs — and what grade of care you can genuinely accept.

The uncomfortable truth is that many people haven’t had enough exposure to the different grades of care to process this well. And your insurance planner — however well-meaning — is often not equipped to advise you on this either. The recent early critical illness claims disputes are a sobering reminder that planners may not always be the right person to tell you what is or isn’t covered.

My reader then spent close to an hour sharing something far more personal: his own private experiences, and the weight of caring for his ageing parents.

(Before I go on — please know that I’m working from memory here, and the 46-year-old brain is not the reliable narrator it once was. Some details may be slightly off, but the spirit of what he shared is intact.)

You Might Need Several Experts in the Room at the Same Time

There are certain complications that don’t belong to just one specialist. You need physicians from different disciplines to come together — to piece things apart, debate the best course of action, and decide collectively. My reader witnessed this firsthand when his mother’s eye pressure situation grew complicated. At a government hospital, they were able to gather a small group of specialists to assess whether to proceed with one therapy or pivot to an alternative. That kind of coordinated, multi-disciplinary response felt almost invisible from the outside — but it was exactly what she needed.

I’ve heard similar accounts from others. When things get genuinely complicated, the government restructured hospitals often have both the depth of expertise and the institutional coordination that private hospitals simply may not replicate as easily.

You May Not Find the Right Equipment at a Private Hospital

For a long time, I naively assumed that private automatically meant more advanced, more sophisticated, more equipped. It took me longer than I’d like to admit to correct that thinking.

My reader shared that one day, his mother suddenly found she could not urinate. I can only imagine how frighteningly helpless that moment must have felt for the whole family — the quiet panic of watching someone you love in distress, not knowing how serious it is or where to go. The urgency, the fear, the scramble.

What eventually helped her was a pessary ring (I hope I got the term right. Physician readers, please don’t kill me). And here’s what startled me: my reader found out that this could only be obtained at KK Women’s and Children’s Hospital. Not at private hospitals. Not at other restructured hospitals. Only at KK.

This wasn’t the first time I’d heard something like this. I’ve encountered similar situations where the only place to get a specific treatment or device is one particular establishment. I’m still genuinely puzzled by why we haven’t decentralised some of these things — though I suspect there are reasons I’m not fully seeing.

What this means practically: even if you go private, you may end up being redirected to a government hospital anyway because the doctors themselves recognize that’s where your problem can actually be solved.

When It’s Urgent, They Move Fast

My reader’s mother’s rising eye pressure was causing her real, significant discomfort. She couldn’t wait weeks for a routine appointment at the Singapore National Eye Centre (SNEC) — this was a family that already had a relationship with SNEC, so they knew the ropes. In such situations, the route is through the Accident & Emergency department, where you will be seen — with some waiting that can test your patience — and if the case warrants it, expedited directly to the right specialist.

It’s not as frictionless as walking into a private clinic. But the cost of care is also a very different conversation.

Epilogue – You Might Want to Join Jiamin’s Webinar

Knowledge that sits close to the actual experience — not theoretical, not secondhand — is what sharpens our lens. My reader’s years of navigating Singapore’s healthcare system with his parents gave him a kind of quiet, hard-won clarity that no amount of reading could fully replicate.

And I think that’s the point.

If you’ve never had reason to interact closely with the government healthcare system, it’s easy to carry an instinctive unease about it. Easy to feel incredulous when costs keep rising and the system doesn’t seem to move fast enough to help. But if you’ve sat in those wards, navigated those referrals, watched those specialists huddle over your parent’s chart, your picture of what “good care” looks like starts to shift.

Downgrading to a shield and rider for government care is not the end of the world. You might not love it. But sitting across from my reader over kopi, listening to everything he and his family had been through, I was quietly reminded of something: no article, no forum thread, no financial planner can substitute for someone who has genuinely lived it.

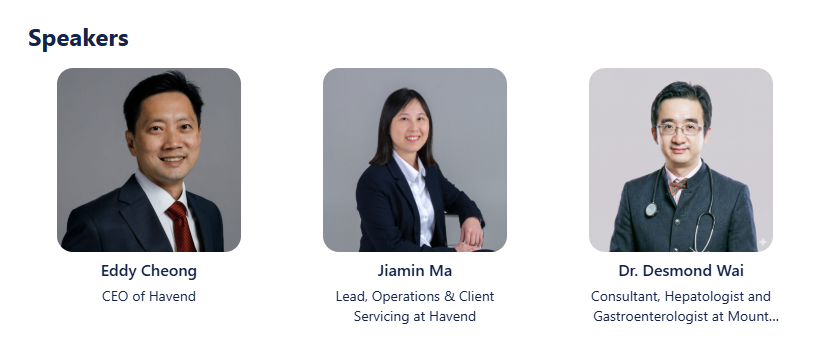

My co-workers Eddy and Jiamin will be hosting a webinar about the claims process on 7 May, Thursday 7:30PM. It is FREE and you can sign up here >>

Why are they doing a webinar on the claims process?

Making claims is not the most glamorous thing and perhaps not what a lot of financial planner think you are interested in. It is when you need to claim that you wondered if you can claim all that you incurred, or only some, and how much would that be. You wonder if the plan will work just like what the person who sold you the plan says.

They will talk about the essentials of integrated shield plans, demystifying the claims language and the end-to-end claims process.

This time we are privilege to be joined by prominent gastroenterologist Dr Desmond Wai at Mount Elizabeth Novena Hospital. Dr Desmond would join our Fireside chat to provide a physician perspective.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

I break down my resources according to these topics:

- All my personal notes about how my philosophy behind my own money and how I manage it.

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I used to work doing research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

- Havend – Where I currently work. We wish to deliver commission-based insurance advice in a better way.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Fee-only Wealth Advisory Firm Providend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith’s current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

Purina Pro Plan Veterinary Supplements FortiFlora Dog Probiotic Supplement, Canine Nutritional Supplement - 30 ct. Boxes

(as of June 25, 2026 02:33 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Wellness Complete Health Pate Variety Pack Kitten Canned Wet Cat Food, Natural, Protein Rich, Grain Free, Whitefish and Chicken Recipes, 3 oz, Pack of 12 Cans

(as of June 25, 2026 02:43 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

UP URARA PUP USA Flag Dog Collar with Flower, 4th of July Comfortable Cotton Dog Collar, American Flag Collar for Puppy Girl Boy Dog or Cat, Patriotic Bowtie Collar with Metal Buckle, S

(as of June 25, 2026 02:43 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Hybrid Active Noise Cancelling Bluetooth 6.0 Headphones 120H Long Playtime, 6 ENC Mic, Over Ear Headphones Wireless, Hi-Res Audio, Memory Foam Earcup, Transparency Mode ANC Headphone for Travel Office

$37.97 (as of June 25, 2026 02:54 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Post Comment