Why Feeling "Safe" About Your Income Strategy Could Be the Deadliest Mistake Killing Your Wealth Growth—Here’s the Brutal Truth!

Ever catch yourself wondering if the classic 60/40 portfolio is really “broken,” or just misunderstood? I stumbled upon a chat where someone shared a video claiming it wasn’t working—but honestly, I skipped the drama and dived straight into the data instead. What really grabbed my attention was a savvy participant’s 70/30 mix—but flipped: 70% fixed income, 30% equity—and his candid take on “slow but survivable” returns. This got me thinking: How do you truly measure your portfolio’s resilience when market winds shift unexpectedly? Using a detailed long-term simulation—from Gilgamesh’s robust framework to real-world muscle—I unpacked what it really means to be conservative ‘the right way.’ It’s not about perfect timing or chasing the market’s lowest dips; it’s about understanding the “big rocks” of income safety that keep your plan standing even when the ground shakes. So, are you ready to challenge your assumptions about what makes a portfolio truly safe? Let’s cut through the noise and get real about growing—and protecting—your wealth. LEARN MORE

img#mv-trellis-img-1::before{padding-top:104.70347648262%; }img#mv-trellis-img-1{display:block;}img#mv-trellis-img-2::before{padding-top:65.4296875%; }img#mv-trellis-img-2{display:block;}img#mv-trellis-img-3::before{padding-top:24.043715846995%; }img#mv-trellis-img-3{display:block;}

In one of the chats that I happen to be able to observe, someone shared a video about when a 60/40 portfolio wasn’t working.

I did not go and watch the video because I felt my time was better spent doing something else.

Someone who was pretty active in the chat posted that his portfolio was 70/30 but its 70% fixed income 30% equity. He commented that the returns were slow this year but survivable.

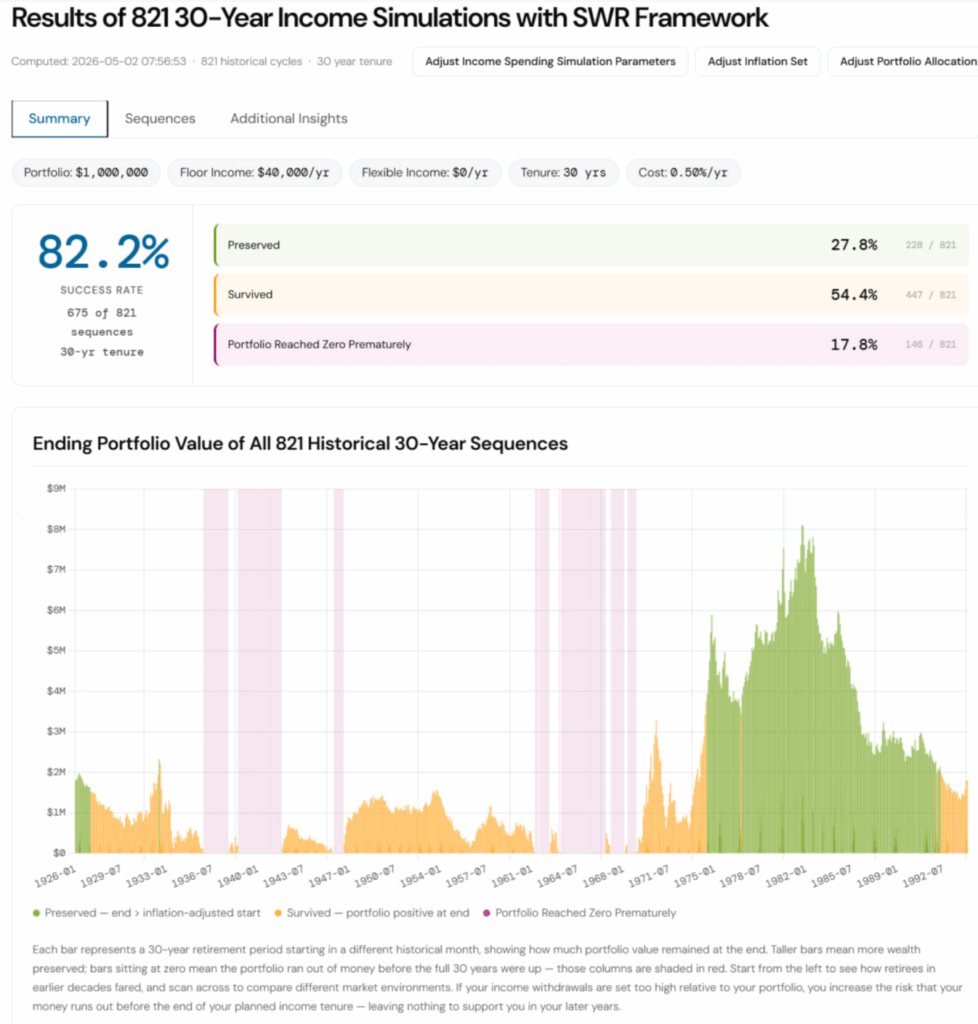

After a long time without any response, I decide to just use Gilgamesh and show over a long period with a 70% US 5-year Treasury and 30% S&P 500, with a 0.50% p.a. all-in cost your chance of success is 82% if you start with a 4% SWR:

It’s not too good but if you happen to start with a 3% SWR the success historically is 100%. But if you push a 3% SWR up to a 50-year income tenure, the success drops back to 82.1%.

The person describes himself as “Kiasu and Kiasee” since whole family depends on him. He describes also that he has a lot of uninvested amount. Eventually he wish for it to be closer to 55-60% equity.

And he says that simulations like this are good for the concept of understanding and planning only if your portfolio of assets in the simulation mirrors that of simulation. He is beyond this level of understanding and planning.

He felt that such simulations are pretty useless to him. Since the data is in USD, and most of his portfolio, if I can detect is SGD based, unless the data is fully hedged back to SGD, it is pretty useless to him.

I detect a few things in past conversations with what I observed is that he may know the Safe Withdrawal Rate framework to a pretty reasonable degree. He probably works in the finance field if my detection is right.

The part that I disagree with is why the results of this SWR framework is less useful for his own personal situation.

I felt that I trust the SWR Framework to give people a glimpse of just how conservative or reckless their income plan is. I would always share because the data may make a person feel more assured than their current state. Or it would raised some red flags that they can still address early in their income spending journey.

Gilgamesh, in its current form is very malleable because there are financial data, with cash, fixed income, and various equity, that allows you to mold the SWR to look at it in different angles. I even show the income results of a 3% SWR 100% Singapore Equity portfolio because we have MSCI Singapore total returns since 1970.

I can accept that the guy has glean correctly the SWR up to now and deem that he is beyond this.

And that like many people he wants to buy the equities at the most opportune time and price.

To which I asked: In the short span of 2 years, we have two pretty major events and there were some drawdowns, was he able to deploy 100% of what he wish to, to bring the allocation to 60/40 or 55/45?

If not, why?

My observation is that not many with a significant sum of cash, who thinks that the current allocation is not their target asset allocation can fully deploy due to psychological and emotional stuff.

What will end up is part of their mental and physical energy is spent focusing on the markets because you have to find the opportune time to fully deploy your money. If you don’t follow the markets, then where to find the opportune time?

They can never fully deploy, either because the prices of what they want never hits that level, or that when it hits, they felt that “it can go lower”.

Only those with severe introspection about their failings for so long, tackled their psychological and emotional flaws, are able to do that.

In a sense, it’s okay if your allocation is not too bad, if you have roughly 40-75% of your allocation in equities. This is based on going through so many SWR cycles (which you can do with Gilgamesh).

What Really Makes You Feel Ultimately Safe?

I just wish to round off the post by focusing on how ultimately what gives the chat group member safety.

What is his mental model of safe.

- Is it all the assets that he has are bought at cheap or reasonable prices? Perhaps he will only feel safe when all the Singapore equities are bought with rock bottom prices.

- Is it because of some weird income buffer framing if he is more of a passive income strategy kind of person?

A person can say one thing, but he or she fails to detect that he doesn’t believe in what he says.

What actually give a person that ultimate safety actually is something that they say it’s not.

So they could say its #2 in the list above but ultimately what makes the person feel safe is #1.

If what gives you ultimate safety is flawed, then you lose your sense of safety when it easily unravel.

Or that you would feel a strange worry and start asking people does your plan make sense still.

Most people are Kiasu and Kiasi but imagine this, most prices today are not Great Depression like. Many Singaporeans, that happen to have market experience after 2008, experiences market drawdowns that did not take 6 years to recover.

What if the ultimate low price is a 60% fall from today, and not a 30% one? If you managed to snag prices that looks reasonably cheap at down 30%, and lets say you manage to get all that you want in. How would you feel if it drops back to the level of purchase 3 years later?

You don’t feel a single thing of worry? You won’t feel confusion?

I would! Even if i have simulated this in my mind to make myself feel better. Here is USSC, which forms 33% of my portfolio then in 2025 when Trump did his thing:

I basically ate a 28% drawdown taking it back to my average price. What if it goes lower?

Most importantly, you can get in at the right price, and your income model is more flawed. You plan with a income yield from your portfolio of 5% and that gives you $50,000 income on a $1 million portfolio. You felt that if you buy all these funds at the “opportune” time, you are set!

But then if the past 20 years, not you but all of us never experience a 400% rise in interest rates, or a COVID that kill office properties, it did not cross your mind that even if you get in the opportune time, the $50,000 income can drop to $30,000, much lower than your planning.

SWR studies with US data is not your kind of portfolio but the reason why I would use that as a vital layer of income risk management is because:

- Its got long enough data of almost 100 years.

- The longer the data, the more weird fixed income and equities behavior are factored in.

- The longer the data, more weird business cycles are factored in.

- You get the good, the decent, the bad and the really bad.

- Most importantly, you get those bad that many of you cannot fathom.

i am not sure if people realize that if you held a 100% S&P 500, the SWR framework will show that if you spend $25,000 on a $1 million portfolio, your $1 million portfolio will drop to $177k (an 82% drawdown) and the portfolio would survived for 30 years.

82% drawdown.

I don’t think that crossed all of your minds.

Even Kyith were to go through that, mentally he would not be able to take it.

But that is the rigors of these tests.

It tests what are the “big rocks” that ultimately make plans safe.

Does any of your mental model of safety actually factors such a challenging situations?

If your model of safety is that you can ultimately go back to work, do you think you can easily find employment in a world where the market dropped 82%?

Yes this is not your Singapore income equity portfolio, but if this were to happen to your Singapore equities, do you think your DBS will keep their dividend payout at 70%?

And so I disagree with the gentlemen that SWR if it is USD based is not so applicable. If it is not like his portfolio it is not applicable.

It is what are the critical lessons, the “big rocks” of income safety that we can glean from it.

Perhaps he understood it enough that he doesn’t have to fully deployed his money. But in a way, if he understood the SWR, he should feel more assured about his current situation. And maybe he is.

I could show readers this SWR again and again, but I get it.

If you are a dividend income person, you would just zoned out on many of these things and if so, you might have not fully comprehend something that can makes you feel more assured about your income strategy.

Ultimately, I acknowledged SWR is not something that many would understand, but in a way, you can’t dismiss its robustness. You can have a plan that is less robust and that may be ok (to a certain degree).

But I hope your sense of income safety is more sound than unsound because if it is unsound and it unravels… that is all on you because you mentally constructed it that way.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

I break down my resources according to these topics:

- All my personal notes about how my philosophy behind my own money and how I manage it.

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I used to work doing research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

- Havend – Where I currently work. We wish to deliver commission-based insurance advice in a better way.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Fee-only Wealth Advisory Firm Providend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith’s current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

Hint Infused Bottled, Best Sellers Variety Pack - Sugar Free Flavored with Zero Calories, Natural Essences, and No Artificial Sweeteners - 16 Fl Oz (Pack of 12)

(as of July 5, 2026 02:41 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Apple AirPods Pro 3 Wireless Earbuds, Active Noise Cancellation, Live Translation, Heart Rate Sensing, Hearing Aid Feature, Bluetooth Headphones, Spatial Audio, High-Fidelity Sound, USB-C Charging

$222.00 (as of July 5, 2026 02:49 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Premier Protein Shake, Chocolate, 30g Protein, No Added Sugar, 24 Vitamins & Minerals to Support Immune Health, Gluten-Free,11.5 fl oz (12 Pack)

(as of July 5, 2026 02:41 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Amazon Echo Dot (newest model) - Vibrant sounding speaker, Designed for Alexa+, Great for bedrooms, dining rooms and offices, Charcoal

$49.99 (as of July 5, 2026 02:49 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Post Comment