Why Holding on to Your Company Stock Could Be the Biggest Financial Mistake You’re Making Right Now

Ever wonder what it really feels like to leave half a million dollars on the table and still wake up the next day without a speck of regret or that nagging fear of missing out? That’s exactly where I found myself after stepping away from my engineering career — no bitterness, no panic — just a strange kind of peace. But here’s the twist: What if the real challenge isn’t about the money you missed, but about how you interpret your wins and losses? How much do we let our emotions and attachments to company shares blind us from making smart, risk-aware decisions?

For many who have their fortunes tied up in the same employer’s stock, the idea of letting go feels like abandoning ship — yet, history and hard-hitting charts tell stories of loyalty crushed under unpredictable market forces and disruptive innovations. Take Accenture for example: a rockstar in the consulting world until AI came knocking, shaking up even the strongest moats. The emotional tug-of-war between “Hold on tight!” and “Time to diversify!” is real — and it’s messy.

This post dives deep into why our default financial advice leans towards selling those company shares or options, the harsh realities of company lifespans shrinking dramatically, and the tough questions every employee-investor must grapple with. Spoiler alert: Even the best-laid plans and systematic diversification may not protect you from wild ups and brutal downs — but acknowledging that uncertainty might just be the smartest move you make.

Ready to explore this financial tightrope walk and get a fresh, no-nonsense perspective on company shares, personal wealth, and emotional investing? Let’s get into it. LEARN MORE

img#mv-trellis-img-1::before{padding-top:71.09375%; }img#mv-trellis-img-1{display:block;}img#mv-trellis-img-2::before{padding-top:71.09375%; }img#mv-trellis-img-2{display:block;}img#mv-trellis-img-3::before{padding-top:71.09375%; }img#mv-trellis-img-3{display:block;}img#mv-trellis-img-4::before{padding-top:71.09375%; }img#mv-trellis-img-4{display:block;}img#mv-trellis-img-5::before{padding-top:71.09375%; }img#mv-trellis-img-5{display:block;}img#mv-trellis-img-6::before{padding-top:24.043715846995%; }img#mv-trellis-img-6{display:block;}

I got all sorts of comments regarding my last post about leaving $500,000 on the table when I left my last engineering job.

I am not bitter about it. Am also not FOMO.

I attribute being able to stomach these things better to missing out a lot of things (not really a good thing!) but also to realize that I do gain a lot in other areas.

Most importantly life progresses forward and the life today is not all that bad. Whether that is a very “Ah Q” way of thinking depends on whether emotionally I really feel that life is really not bad financially.

The more critical thing is whether each of us is able to not attribute successful or unsuccessful outcomes to good and poor financial decisions.

What is corrosive is that… there are many that equates successful or unsuccessful outcomes to the decision to be good and poor respectively.

A large proportion of the better returns comes since 2024. That is like almost 18 years since I joined the company.

If you look at the time weighted return from 1 Jun 2005 to 1 Jun 2024 that I been with the company and before the big run up, the annualized return over 19.2 years is 6.9% p.a.

But you just add the run up of about 2 years, it becomes 11.7% p.a. In total returns it looks more bombastic. It’s 259% of gain versus 954% gain.

Our Default Orientation is to Ask Our Clients to Sell Their Company Shares or Options.

And I think for good reasons that I can state.

We do have clients that come to us where the majority of their net wealth is in their company shares that have done very well.

So the decision here is “why not continue to hold on to what have built the majority of my wealth up to this point, into something whose returns in the past is not as good to this?”

Well not everyone asks our adviser this way but in a raw manner that must have been what they are thinking.

One of our clients who is in my Telegram group stated his reasoning:

The downside with employee share plans is that you are already depending on that company for your income stream. If a significant part of your assets is also the same company’s stock, your dependency on one company becomes very risky.

Some of us have seen employees of more than 20 years lose their jobs and wealth when their employer got into major trouble. And these were established mighty companies with respected long histories.

I made sure that when I received my next tranche every 6 months, I’d sell the earlier tranche. And diversify my assets to other investments. No regrets even when the final tranche became 4x 15 years after I stopped working for them.

I could not have explain better.

But I think there are a few different stuff that I would like to elaborate further.

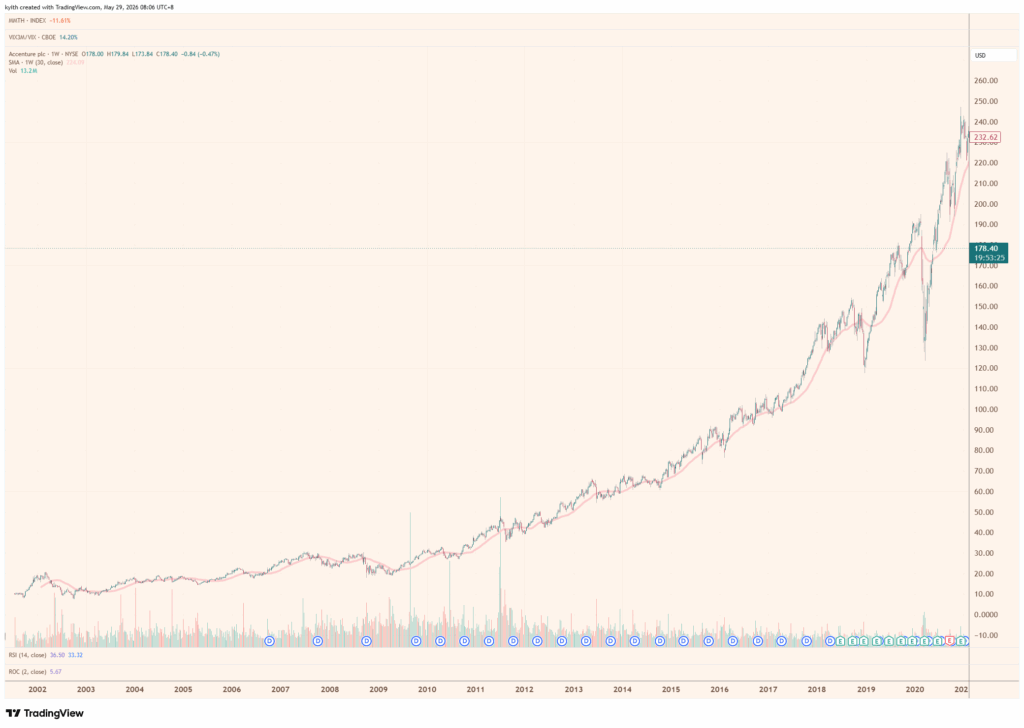

This is a chart of Accenture PLC (Ticker ACN):

If I have a view of someone in mind, it would be someone who work a long career in Accenture. Consulting firm Accenture was one of the firms many graduates aspire to join because they pay better and the projects seems cooler.

We have a pretty good base of people in Singapore working for Accenture.

If you repeat the question that I asked, you can understand why the brains might think it make sense but the heart will feel pain.

And it is not uncommon that although we explain that the most important thing that you should consider is that you are tying the fate of your family’s future in one, single company. If the company does extremely well, your family does extremely well. Hell, the reason why you are in a position to consider this decision is that it has done well to even make this a consideration at all!

The rational part is to consider:

- What is the base rate? Do we think all companies trajectory is like this?

- How many companies actually die or get delisted after a while (often not because of very good outcomes). It used to be 61 years for the stocks in S&P 500 in 1958. Today it is closer to 15 years.

So would you take a chance to bet that the place that you work for is going to be the uncommon companies that does not follow the laws of this base rate?

If I explain so much to the best of my ability and you are still adamant, then okay lor, it is your choice.

What’s hard for all of us is we just cannot recognize… before the tough times that we would only learn the impact of these things when the going gets tough.

So what you see is how ACN’s total returns has been since that run up.

I don’t know how many times I have seen this kind of very nice gradual long term run up, then come crashing down chart in my 20 years investing time.

Objectively ACN is a stock that many see that has a good moat, always going to need consultation, integration and project works.

Until something call AI starts coming up and fxxk them up.

For those who have reviewed ACN as an investment before, you need to touch your heart and ask yourself how was your view about its moat before and after.

It might raised enough insecurities regarding how well you can see things properly, your qualitative forecasting and evaluation abilities.

Different Employees Will have Different Experiences

I guess the newer Accenture employees would think whether to diversify more or rely on Accenture shares differently compare to the long time employees.

We are sooooooooooooo affected by our experiencing self than the remembering self.

This means our emotions at this point affects our financial decision making and it is very challenging to be objective about it.

Good, Sound and Systematic Plans May not Mean You Get the Best Outcomes

Systematic plans that help you diversify out of a significant portion of company holdings should:

- Move you to a fundamentally sound investment strategy that can build wealth.

- Don’t have that significant concentration problem.

- Manage the emotional part of FOMO and Oh Shit better.

In general, most would ask them to diversify over time, or in tranches.

But I would tell you… it just makes you feel better but you just got to be ready that your company can:

- Go to shit anytime.

- Go to the moon anytime.

I think some of you would no what examples that I want to bring up:

This is a chart of Seagate (STX).

Singapore used to do a lot of hard disk manufacturing until they get offshore. The offshoring in itself is also a story.

Now you got to ask those Seagate staff. Touch your heart and tell me, at any point in your life, as you held your company shares, you picture there is a possibility Seagate’s shares will go 10x in almost 1 year?

I can ask the same because we also got a good Micron (MU) or ex-Micron population in Singapore.

If you ask them… how they view these stocks is very different from an investor.

They usually don’t invest and they only view one stock. Their company stock!

I can tell you I always have an image of my company shares bouncing between $2 and $4. Always bouncing in this range. I have a fundamental lens that the company may do better than this. Objectively I can see a company executing well out of our main domain and the market repricing our company. But in no fxxking way do I imagine we will hockey stick.

And so this is a good question.

One of my longest time reader (most likely don’t read my blog now since he is now based in China) works for Bank of America (BAC) at the start of his career. He started contacting me in 2010/2011.

You can see this is his experience.

Now you tell me how would he invest? Put in banks like you guys?

Some would rationalize: “Kyith you must pick the right banks!”

To that I say you really have distill ANYTHING from this series of posts.. which is that your stocks no matter how good, or how shit, can take trajectories you can’t mentally imagine.

And the key question is: Do you want the fate of your family and your wealth to be so so so so so so so tied up in one or two things?

To My Colleagues who are the Client Advisers and Associate Advisers Trying to Be Advisers.

I hope the images of these charts gets burned into your minds.

The tone, the degree of time you spend on a subject will be different based on your very own experience. The decision trees are usually the same.

But advise is more than just a “which is better?” decision tree.

Usually some decisions are tough to make because the outcomes are uncertain.

A person could come in and diversifying out over a few years and would either miss out on a really great upside or for it to go to shit. Sometimes it is good to have some of these extreme examples in your “briefcase” as they are more relatable.

Hopefully that adjust the expectations. At the end of the day, we cannot quite control whether the business will turn really good, or really poor.

As an employee, you might see something bad or good, but it is important to note that what you think may not eventually happen.

Or at the pace that you can plan for.

The decisions we make is due more to the uncertain dynamics and therefore those are good financial decsions.

Just the outcome sometimes can be so much better.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

If you’re thinking of opening an Interactive Brokers account, my referral link is here.

As the new account holder, you’ll receive USD 1 in IBKR stock for every USD 100 you deposit, up to USD 1,000 in shares — so a USD 10,000 deposit gets you USD 100 in IBKR stock, and the bonus is capped at USD 1,000 for deposits of USD 100,000 or more. A few other things to know: the minimum deposit to qualify is USD 10,000, done within 30 days of opening, and the bonus shares are locked up for one year from the award date. The promotion is currently active, and using the link costs you nothing extra. On a separate note, if you haven’t already, it’s worth taking a look at how IBKR’s share price has performed over the past five years — the stock you receive as a bonus isn’t just a token; it’s a stake in a company that has done quite well for its shareholders.

I break down my resources according to these topics:

- All my personal notes about how my philosophy behind my own money and how I manage it.

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I work and do research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Fee-only Wealth Advisory Firm Providend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith’s current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

Ring Battery Doorbell (newest model), Speckled Gray with Chime (newest model), White

$104.98 (as of August 3, 2026 03:06 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

ChefBee 4PCS 6.7" Stainless Steel Shallow Cat Bowls, Whisker Friendly | Flat Shallow Wide Design, Food & Water Dishes, Easy to Clean, For Indoor Cats, Kittens & Multicats, Pet Feeding Plates

$7.21 (as of August 3, 2026 02:58 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Best Pet Supplies Interactive Squeaky Dog Toy - Crinkle Duck, Blue | Stuffing Free Body, Soft, Squeaks & Crinkles, No Mess, Perfect for Moderate Chewers, Toss and Fetch Play

$5.99 (as of August 3, 2026 02:52 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

YISHU 6Ft Surge Protector Power Strip with 8 Widely Outlets & 4 USB Ports | 3 Side Outlet Extender with 6 Feet Extension Cord, Flat Plug, for Home, Office, College Dorm Room Essentials, ETL, White

$9.99 (as of August 3, 2026 02:58 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Post Comment