Could the Fullerton Wise Income Fund Secretly Be Your Ultimate 30-Year Payday?

Ever wonder why a steady 4.5% distribution from an income fund sometimes feels like riding a rollercoaster blindfolded? That’s exactly the conundrum with the Fullerton Wise Income fund’s R class—while it promises a consistent slice of the NAV, the reality is a wild dance of income volatility because, at its heart, it’s tethered to capital fluctuations. Now, sure, you could always just sell units to smooth out those income bumps, but here’s the kicker: selling units means your portfolio’s clock is ticking faster toward empty. Can you really have the best of both worlds? Most investors tiptoe around this truth, clinging to the hope that enough income buffers the shocks—but luck (and capital!) only goes so far. With my trusty Safe Income Spending Simulator—cue the name Gilgamesh—I’m diving deep, running dozens of 30-year retirement scenarios to see just how a Wise Income-like portfolio holds up under fire. Spoiler: It’s a lot more nuanced than a fixed percentage payout. Curious to see the real story behind those numbers and what they mean for your retirement game plan? LEARN MORE

img#mv-trellis-img-1::before{padding-top:60.521415270019%; }img#mv-trellis-img-1{display:block;}img#mv-trellis-img-2::before{padding-top:59.66796875%; }img#mv-trellis-img-2{display:block;}img#mv-trellis-img-3::before{padding-top:86.906019007392%; }img#mv-trellis-img-3{display:block;}img#mv-trellis-img-4::before{padding-top:57.989228007181%; }img#mv-trellis-img-4{display:block;}img#mv-trellis-img-5::before{padding-top:57.91015625%; }img#mv-trellis-img-5{display:block;}img#mv-trellis-img-6::before{padding-top:54.39453125%; }img#mv-trellis-img-6{display:block;}img#mv-trellis-img-7::before{padding-top:88.39190628328%; }img#mv-trellis-img-7{display:block;}img#mv-trellis-img-8::before{padding-top:89.343379978471%; }img#mv-trellis-img-8{display:block;}img#mv-trellis-img-9::before{padding-top:89.633507853403%; }img#mv-trellis-img-9{display:block;}img#mv-trellis-img-10::before{padding-top:52.100840336134%; }img#mv-trellis-img-10{display:block;}img#mv-trellis-img-11::before{padding-top:85.412262156448%; }img#mv-trellis-img-11{display:block;}img#mv-trellis-img-12::before{padding-top:64.406779661017%; }img#mv-trellis-img-12{display:block;}img#mv-trellis-img-13::before{padding-top:36.881720430108%; }img#mv-trellis-img-13{display:block;}img#mv-trellis-img-14::before{padding-top:43.816631130064%; }img#mv-trellis-img-14{display:block;}img#mv-trellis-img-15::before{padding-top:77.258235919235%; }img#mv-trellis-img-15{display:block;}img#mv-trellis-img-16::before{padding-top:44.468313641246%; }img#mv-trellis-img-16{display:block;}img#mv-trellis-img-17::before{padding-top:24.043715846995%; }img#mv-trellis-img-17{display:block;}

There is this Fullerton Wise Income fund that has 2 distribution class. The R class distributes 4.5% of the NAV. This is basically a constant-percentage withdrawal method and such a method technically can just keep giving 4.5%. But because it is based on capital, your income is going to be volatile.

But you could always choose to sell units so that you can have a consistent income.

Well selling units is always touchy for many because if you sell units, your portfolio will run out of money faster?

You cannot have both really. I find that income investors have to acknowledge that if your income is volatile it is also a problem! What makes many of their plan work is that they have so, so, so much more income that the volatility doesn’t affect them. It is good to acknowledge what makes them work isn’t taking only natural fund distribution… but they have more capital.

Anyway, since I have Gilgamesh, my Safe Income Spending Simulator, I thought why not see how a Wise Income like portfolio would do over many, many, many 30-year retirement.

So that is this post is about.

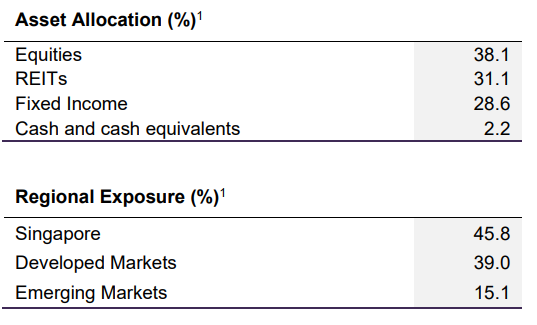

You can find the January 2026 Fullerton Wise Income Factsheet here.

Here is the allocation.

We are going to start somewhere to simulate with Gilgamesh, and then we are going to do a few variations to see how changing some parameters could change how we view a Wise Income-Like portfolio.

What I Put into my Fullerton WiseIncome Simulation

- Inflation Scheme: US CPI [Up to Feb 2026]

- All-in-cost: 0.40% p.a.

- Portfolio Allocation:

- MSCI World: 30%

- S&P Asia Pacific REIT: 30%

- ICE BofA 1 Year US Treasury Note Index: 20%

- 20-Year US Treasury Index: 20%

I think this is not the most ideal. Ideally, we want to use Singapore REITs only, but the first Singapore REITs only started in 2002 (which is either CapitaMall Trust or Ascendas REIT), so you can’t have so many 30 year periods.

S&P Asia Pacific REIT starts in 1989 which will give us a fair amount of 30-year periods.

I would hope to use some Asian bonds, with a shorter duration, but we don’t really have that data. So I used a barbell approach of a 1-year US Treasury and 20-year US Treasury to get to a close enough duration. Without Asian focused bonds, the investor lose out on the credit premium, but gain some lower volatility.

The tenure of data is from Aug 1989 to Sep 2025. There are 434 months so this gives us 75 historical 30-years period if we iterate month by month.

We try to spend an inflation adjusted $40,000 from a $1 million initial portfolio and see if the portfolio last for all 75 30-year periods.

The result show they do last. 5 out of the 75 did not preserve the value, which is an okay thing. It is more to show that in 70 out of those 30-year periods, you end up having a lot of income AND your $1 million is preserved in inflation adjusted terms.

Here is the metric for such a portfolio. That is the CAGR for this whole period and the Sharpe and Sortino ratio. The standard deviation is pretty low.

In the worst 30-year period, the portfolio is left with $1.8 mil.

And you can go to the “Sequences” tab to see each of those period.

What If I Dramatically Reduce the Duration of the Fixed Income

20-year fixed income gives higher return, but it also caused the portfolio to have greater drawdown if it lives through the 2022 period.

But let me replace the 20-year with just all 1-year Treasury Note and lets see the result.

What we will notice is that instead of the portfolio values preserved in most 30-year sequences, most only end up surviving. You will see the ending values to be still near the starting $1 million, but adjusted for inflation they kind of did not preserve the inflation-adjusted $1 million.

What if We add 5% in US High Yield Bond to the 1-Year Treasury Note Mix?

The wacky thing is I saw that among the top 5 fixed income holdings the WiseIncome fund held a iShares USD Asia High Yield Bond ETF. Some would find that it is a risky move and I have stated my stand on high yield fixed income. It is basically equities masquerading as fixed income.

It goes down when equities go down so it doesn’t cushion the portfolio during more distress times. While we do not have Asia High Yield data, we can replace it with a Bloomberg US high yield bond index to see how the portfolio reacts.

I got to caveat first: Asia High Yield is not exactly US high yield. During the recent China bear, a lot of Asia high yield fixed income really got their value cut and they still don’t look good today. Asia High Yield end up as China High Yield. So I don’t want you to think that these are similar.

The result looked better than just using 1-Year US Treasury.

Why not Use Global Aggregate Bond Instead?

Ok instead of fidgeting with the fixed income so much, lets just use the Bloomberg Global Aggregate Bond Index, which is a 6 year duration, average investment grade fixed income index fund.

I don’t want to use this initially because the data set is smaller. We can only have 70 30-year period.

This ended up pretty good!

More of the portfolio value is preserved after spending the income.

What if We Jack Up the All-in-Cost to 1.4% p.a.?

We take the last portfolio, with the Bloomberg Global Aggregate Bond, and jack-up the cost to include Advisory fees:

With the added fees, this should add stress to the portfolio:

Instead of preserving wealth, most of the 30-year cycles ended up surviving. Still more than $1 million.

What is Really Challenging for Such a Portfolio

I think there are some sequences that takes place in the past 30 years, that have not completed a full 30 years that can be challenging.

If you invest $1 million at the top of before GFC, around Jun 2007, that is something that may be potentially challenging that we wonder if the portfolio can survive.

I reduce the tenure to 17 years (from 30 years) and we are able to see such challenging sequence.

Here is the 17-year period starting in Jun 2007 and ending May 2024:

You can see the 17 year return is like 2.7% p.a. Immediately after invested the portfolio dropped to $600k. It did survive and up to today, it held $473,850 in value.

You drew income of $40k to a final income of $59k in the last year.

The current withdrawal rate shows us if we take the income drawn out at any month, divide by the current portfolio value, what is the withdrawal rate. A low number shows that the portfolio can still deliver income for many more years and if this is too high, the income may not last long.

We can see that in this sequence, the ending current withdrawal rate is 12.7%.

If it is this sequence, most likely the investor cannot draw an inflation adjust income for more than 8 years.

What if We Reduce the Starting Income to $30,000 instead of $40,000 in the Initial Year?

We take the same portfolio, with the same higher fee, but we reduce the income drawn out.

The solution to negative sequence of return risk (which this potentially is) is a lower safe withdrawal rate.

We can take a look at how it looks:

The chart might look the same but its actually higher at $750k instead of $473k.

The most telling is that the current withdrawal rate has now halved at 6% instead of 12%. At 6%, whether your money will last or not depend on market returns and if inflation picks up. In a favorable sequence, your money would last better.

All this goes to show that there are challenging sequence but there is a reason to remain conservative in how much you decide to spend at the start.

Let me know if you have any questions below

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

I break down my resources according to these topics:

- All my personal notes about how my philosophy behind my own money and how I manage it.

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I used to work doing research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

- Havend – Where I currently work. We wish to deliver commission-based insurance advice in a better way.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Fee-only Wealth Advisory Firm Providend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith’s current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

CELSIUS Assorted Flavors Official Variety Pack, Functional Essential Energy Drinks, 12 Fl Oz (Pack of 12)

$21.99 (as of August 5, 2026 02:52 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Lavazza Super Crema Whole Bean Coffee, Medium Espresso Roast, Arabica and Robusta Blend, 2.2 lb Bag, Package May Vary (Pack of 1)

$26.99 (as of August 5, 2026 02:52 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Oura Ring 5 Sizing Kit - Size Before You Buy Oura Ring 5 - Unique Sizing, Not Standard Ring Sizing - Receive Amazon Credit for Oura Ring 5 Purchase

$10.00 (as of August 5, 2026 02:58 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Apple 2026 MacBook Pro Laptop with Apple M5 Pro chip with 15-core CPU and 16-core GPU: Built for AI, 14.2-inch Liquid Retina XDR Display, 24GB Unified Memory, 1TB SSD, Wi-Fi 7; Silver

$2,259.99 (as of August 5, 2026 03:06 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Post Comment