SOX Soars to Extreme Overbought Territory — Here’s the Shocking Twist History Warns Could Unfold Next

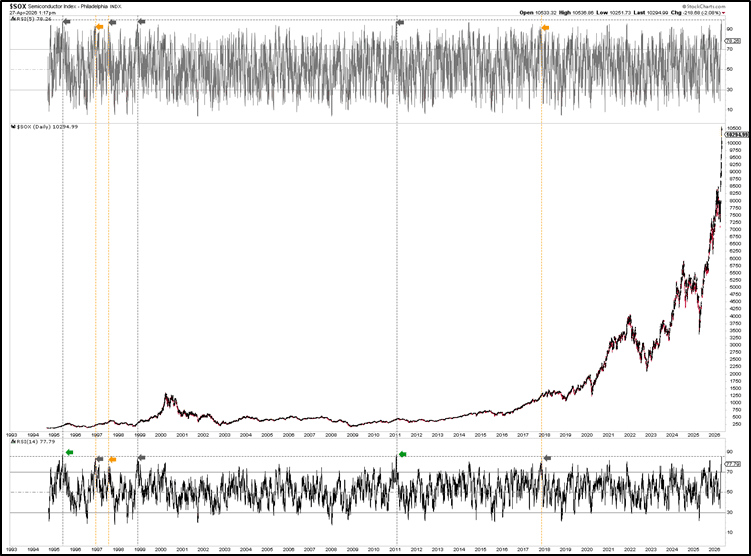

Have you ever witnessed a rally so intense that it practically shouts, “Hold on tight, this is historic!”? Well, the semiconductor index (SOX) just delivered that punch with a staggering 50% surge and an eye-popping 18 consecutive days of gains. Friday, April 24, wasn’t just any day—it marked the moment when the 5-day and 14-day relative strength indicators (RSI5 and RSI14) rocketed to 98.7 and 85.1, pushing the envelope beyond anything we’ve seen before. To put it bluntly, the RSI5 hit a level the SOX has never dared to reach, while the RSI14’s blink-and-you’ll-miss-it appearances in 1995 and 2011 only add fuel to the fire of this extraordinary run. Yet, here’s the kicker—such lofty readings rarely leave much gas in the tank for the near term. It’s as if the market is pulling a double take, asking itself, “How much higher can we really go before the music stops?” This phenomenon isn’t just about numbers—it’s about the story those numbers tell: a powerful rally on its last legs, hinting at a short-term cooldown before any further ascent. Ready to dive deep into what history whispers about these rare overbought moments, and what the future might just hold for the SOX? Let’s unpack the data, the patterns, and the waves that weave this tale. LEARN MORE

The recent 50% rally in the semiconductor index (SOX), with an unprecedented 18 consecutive up days, has been a sight to behold, pushing many forecasts and indicators to their limits. As such, on Friday, April 24, the 5-day and 14-day relative strength indicators (RSI5, RSI14) registered at 98.7 and 85.1, respectively.

The former has never been this high in the index’s history, whereas the latter has been exceeded only twice before: 1995 and 2011. See Figure 1 below. These are signs of a very strong rally, but they also indicate that it is very extended, with little room for further short-term gains. For example, the RSI ranges from 0 to 100.

Figure 1. Daily chart of the SOX with the RSI5 and RSI14

As such, we set out to assess how the index performed in prior instances with similar overbought readings, even though the daily RSI5 was at its highest level on Friday, leaving no precedent but only good analogies. Hence, we focused on the closest readings, with the daily RSI5 above 95.0 and the RSI14 above 83.5. Figure 1 shows that there have been three such instances since 1994. There were also three occasions when either the RSI5 was over 95 or the RSI14 was above 83.5, but not both, as tabulated below.

Table 1: Forward returns when the daily RSI5 and 14 are above 95 and 83.5, respectively

On all six occasions, the immediate downside risk is, on average, -7%, ranging from -5% to -11%. The intermediate-term forward return is, on average, 15%, ranging from 5% to 67%, with only one case (1998) having a negative return. Lastly, the longer-term performance (12 months out) is, on average, 8%, ranging from -40% to +80%, with only 1998 deviating from the rest. Figure 2 below shows the 1996 and 1997 forward returns

Figure 2. Forward returns for the SOX when either the RIS5 is >95 or the RSI14 is >85

Thus, except for 1998, all other instances show a similar pattern: short-term downside risk, intermediate-term upside reward, and longer-term downside risk. If we exclude 1998, the average intermediate- and long-term returns are +25% (5 to 67%) and -26% (-39 to -2%).

This recurring pattern makes sense. The extremely high RSI readings require an immediate reset before the index can move higher again. However, these extreme readings also occur at terminal moves, e.g., 5th waves in the Elliott Wave (EW). Meanwhile, the extreme readings and resets are often (smaller) 3rd– and 4th-wave events. See Figure 3 below.

Figure3. Daily chart of the SOX with Elliott Wave Count

Our EW count shows the index has likely completed a 3rd of a 3rd wave: green W-3 of red W-iii, and is now in green W-4, ideally $9700 +/- 200, before W-5 to $13,000+ can take hold. After that, a final, larger 4th and 5th wave (red W-iii and -iv) should commence before the move from the April 2025 low can be considered complete, allowing the index to enter a new bear market.

These waves align with the forward returns:

· short-term risk = green W-4.

· The more variable intermediate-term upside (weeks to months) = red W-iv and W-v.

· The consistent negative returns one year out = “a new bear market.”

As such, although past performance is no guarantee of future results, we have objective historical data that aligns with our present, albeit more subjective Elliott wave count. This is a powerful combination, giving a high likelihood to the presented outcomes.

Rice Krispies Treats Crispy Marshmallow Squares, Kids Snacks, Cereal Bars, Original, 31.2oz Box (40 Bars)

$11.23 (as of August 3, 2026 03:03 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Purina Fancy Feast Gravy Lovers, Poultry & Beef Wet Cat Food, 3oz, 24-Pack | Variety Pack, grilled gourmet texture made with no artificial colors or preservatives, 100 percent complete and balanced

$22.86 (as of August 3, 2026 02:52 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Happypaw 3.0 2026 Upgrade 18'' Herding Ball for Dogs – Enhanced Chew Resistance & Heavy-Duty Material, Dog Toy Agility Equipment for Australian Shepherds,Collies, Includes 5 Repair Patches

$35.99 (as of August 3, 2026 02:58 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Amazon Basics Leak-Proof Dog and Puppy Potty Training Pee Pads with Quick-Dry 5-Layer Super Absorbent Design, Regular Size 22 x 22 inch, Blue & White, 100 Count

$18.99 (as of August 3, 2026 02:52 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Post Comment