The Shocking Truth Behind Why Cautious Retirees Buckle Down on Ultra-Low Withdrawal Rates — And What It Means for Your Financial Freedom

Ever wonder why so many folks swear by “risk tolerance” when planning their investment journeys—only to find themselves paralyzed the moment markets turn south? I stumbled onto a killer tweet by Cullen Roche from Discipline Funds that flipped this whole idea on its head. Turns out, the idea of a “subjective risk tolerance” might just be a myth we’ve all bought into. Everyone freaks out when the bear market bites, whether they admit it or not—and that’s 100% normal. The real game-changer? Understanding your financial risk capacity—a quantifiable, way more practical way to map your portfolio risk based on your actual financial health, not how brave you feel on any given day. Imagine a 65-year-old retiree with $500K versus another with $5 million; their capacity for financial risk couldn’t be more different, and this disparity can literally make or break retirement plans. If you’ve been banking on emotions or age to steer your risk level, it’s time to rethink your playbook. This post dives deep into why those who retire comfortably often stick to super low Safe Withdrawal Rates (SWR), how psych factors turn math into panic, and why billionaires essentially run a different SWR game altogether. Buckle up, because we’re about to decode the real science behind financial peace of mind—and yes, it’s not what you think. LEARN MORE

img#mv-trellis-img-1::before{padding-top:86.03515625%; }img#mv-trellis-img-1{display:block;}img#mv-trellis-img-2::before{padding-top:87.01171875%; }img#mv-trellis-img-2{display:block;}img#mv-trellis-img-3::before{padding-top:77.44140625%; }img#mv-trellis-img-3{display:block;}img#mv-trellis-img-4::before{padding-top:24.043715846995%; }img#mv-trellis-img-4{display:block;}

I saw this Tweet by Cullen Roche, of Discipline Funds about risk tolerance that I resonated with:

let me repost here:

This is something I’ve completely changed my mind about in recent years. I now think the idea of a subjective “risk tolerance” is a terrible concept.

Everyone gets scared during a bear market. And everyone thinks they won’t get scared during a bear market. You will. And it’s normal.

Your portfolio risk should be based on your financial risk capacity and that is absolutely quantifiable if one correctly assesses balance sheet vs income statement health.

A 65 year old retiree with $500K withdrawing $20K per year has a vastly different risk capacity than a 65 year old with $5MM withdrawing $50k per year. The person with the superior financial health can take more risk because they have vastly less sequence risk in their financial plan.

Young people with stable incomes can typically take more risk because their income is equivalent to a very large and safe fixed income allocation. They should take more equity risk because their income statement health allows it.

Age and emotions shouldn’t be the primary driver of risk. Financial health and risk capacity should.

I connected with Cullen’s income planning example more.

Cullen has seen clients since probably 2006. That is 20 years. If you talk to enough people, and also have the unique ability to deconstruct things, you should pay attention to this.

And I also dovetail to the same view as him.

Why Financial Anxious People Usually Retire with a Very Low Safe Withdrawal Rate (SWR)

My friend Kit from Cents of Independence observed that those who successfully retire and stay retired usually ends up with a very low Safe Withdrawal Rate (SWR) number of closer to 2-2.5%.

Those people don’t describe their method as a SWR method. They use other ways to describe it.

But you will realize that when you take their spending or income needs, divide by the amount that drives their income, it comes up to 2-2.5%.

Why is that?

It’s because you end up closer to that person with $5 million spending $50k.

This person’s SWR is 1%.

The person feel safe because in their mind either:

- “My 5 million gives me $300,000. In the worse case even if it gets cut to $100,000, i can live on $100,000 of income”

- “I have this stream of income, that stream of income, another stream of income, and another stream of income, and if markets are not good I will tap this, I will tap that, then tap that”

They all mean the same thing.

Low SWR.

They just don’t call it that way.

They are the Billionaires. Billionaires’ $20 mil a year lifestyle look expensive, but if you have $2 billion that is just a 1% SWR.

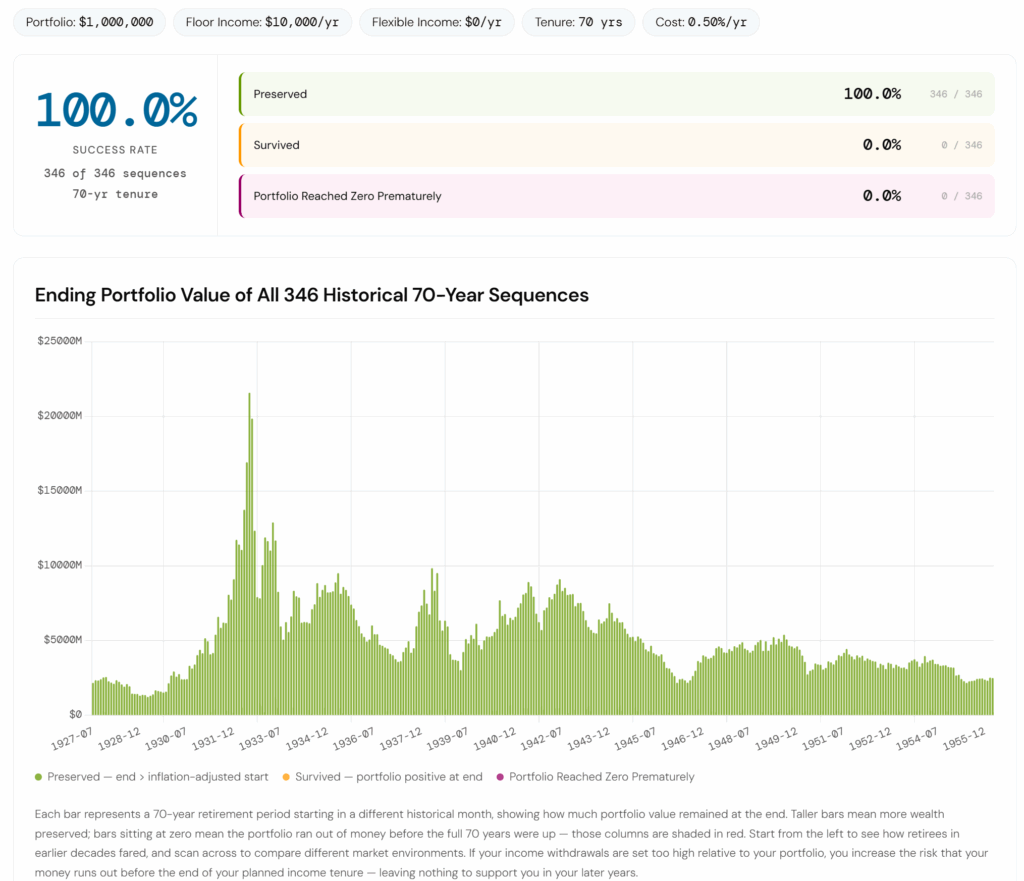

Since I have Gilgamesh, let me show you a 1% SWR on a 100% US Small Cap Value portfolio if you wish to retire for 70 years. Why US Small Cap Value Kyith??

Firstly the data is from 1927 to today so you can actually simulate living through 346 70-year periods of the past. Secondly, in the Great Depression, US Small Cap went down 91%. If you do 100% US Small Cap Value, its like your $1 million left with $90k. It is a very, very, very brutal test.

Here is the result:

All 346 survive this brutal test on a 1% SWR.

Bear in mind, I put in a 0.50% p.a. all in cost. This means that your spending is just double the cost of the investment.

You are spending so low.

I can tell you the worst ending value that started with $1 million end up 70 years later with $1.2 billion.

You end up preserving your capital and the money last intergeneration.

The math of SWR always works out because it puts so little pressure on the portfolio.

Why the 65 year old retiree with $500K withdrawing $20K per year has a vastly different risk capacity

The SWR is 20,000/500,000 = 4%

To you it look safe but… if we subject to the same portfolio test:

Well it is pretty good because… US Small Cap is a little mad (for the large cap bros who didn’t realize the long term data)

You can get a pretty good result under most conditions.

But what Cullen and I would like to point out is… its psychological.

Actual living would look like this:

I picked out a 30-year period where you spend an initial 4% of the portfolio but at the end of 30 years, you end up preserving your capital in inflation adjusted terms (means you can pass on the money to next generation).

You notice a $1 million gets close to $170,000. And you are spending like $30,000 +-.

While the math may check out in the end if your capital gets so close to that, you will freak out one.

You tell me your portfolio drop by 5 times you won’t freak out?

And that is human emotions.

A Very Low SWR Buffers for Not just Market and Inflation Uncertainties but Perhaps Life Uncertainties.

If you retire younger, the income needs spans over a longer period.

The longer the period, the more “threads” or pathways will happen.

And you cannot depend on performance for everything. You will keep thinking “I need more income. I need more income.”

And income means capital lor. It is the same as a low SWR.

But Kyith I am not a Billionaire, I cannot Spend like that! It takes a long time to Save that!

I am trying to explain the math here.

Many who came into that wealth either are very frugal people (like me) or that they made so much more but are frugal, or they came into wealth by selling their business.

I don’t know you can reach it or not I am just explaining the math here.

Hopefully you get it.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

If you’re thinking of opening an Interactive Brokers account, my referral link is here.

As the new account holder, you’ll receive USD 1 in IBKR stock for every USD 100 you deposit, up to USD 1,000 in shares — so a USD 10,000 deposit gets you USD 100 in IBKR stock, and the bonus is capped at USD 1,000 for deposits of USD 100,000 or more. A few other things to know: the minimum deposit to qualify is USD 10,000, done within 30 days of opening, and the bonus shares are locked up for one year from the award date. The promotion is currently active, and using the link costs you nothing extra. On a separate note, if you haven’t already, it’s worth taking a look at how IBKR’s share price has performed over the past five years — the stock you receive as a bonus isn’t just a token; it’s a stake in a company that has done quite well for its shareholders.

I break down my resources according to these topics:

- All my personal notes about how my philosophy behind my own money and how I manage it.

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I work and do research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Fee-only Wealth Advisory Firm Providend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith’s current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

Apple iPad Air 11-inch (M4): Liquid Retina Display, 128GB, 12MP Front/Back Camera, Wi-Fi 7 with Apple N1, Touch ID, All-Day Battery Life — Starlight

$689.00 (as of August 3, 2026 03:06 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Twinings English Breakfast Black Tea Individually Wrapped Bags, 100 Count (Pack of 1), Smooth, Flavourful, and Robust, Caffeinated, Enjoy Hot or Iced, 100 Teabags | Popular Tea Classic, Robust & Smooth, Naturally Caffeinated, 100 Foil Lined Individually Wrapped Bags, Enjoy Hot or Iced

$12.38 (as of August 3, 2026 03:03 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Amazon Fire TV Stick HD, free and live TV, Alexa Voice Remote, smart home controls, HD streaming

$19.99 (as of August 3, 2026 02:58 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

INSIGNIA 50" Class F50 Series LED 4K UHD Smart Fire TV, Voice Remote with Alexa, Stream Live TV Without Cable

$169.99 (as of August 3, 2026 03:14 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Post Comment