Why Your $1 Million IUL Policy Could Be Costing You More Than You Think—And It’s NOT What You Learned About Index Investing

So, you’ve probably heard the buzz—Indexed Universal Life policies (IUL) are the latest shiny object for affluent Singaporeans aiming to ride the waves of S&P 500 or Nasdaq-like returns, without directly buying ETFs or unit trusts. Sounds like the best of both worlds, right? But here’s the kicker: what if your “indexed” returns aren’t exactly what they seem on paper? Instead of soaking up dividends like a regular index fund, you’re actually playing a sophisticated game of options—where returns hinge heavily on the fixed income portfolio’s income and market volatility. It’s like betting on a roller coaster that nobody fully controls, yet hoping it won’t crash. Curious how your million-dollar premium might be ping-ponging behind the scenes? Stick around — I’m peeling back the layers to expose the real engine powering these IULs, and why your policy’s future value might be more unpredictable than your favorite playlist. Ready to see beyond the brochure’s glossy promises? LEARN MORE

img#mv-trellis-img-1::before{padding-top:76.953125%; }img#mv-trellis-img-1{display:block;}img#mv-trellis-img-2::before{padding-top:36.42578125%; }img#mv-trellis-img-2{display:block;}img#mv-trellis-img-3::before{padding-top:89.35546875%; }img#mv-trellis-img-3{display:block;}img#mv-trellis-img-4::before{padding-top:60.64453125%; }img#mv-trellis-img-4{display:block;}img#mv-trellis-img-5::before{padding-top:30.2734375%; }img#mv-trellis-img-5{display:block;}img#mv-trellis-img-6::before{padding-top:24.043715846995%; }img#mv-trellis-img-6{display:block;}

One of the reasons why more affluent Singaporeans are interested in purchasing Indexed Universal Life policies (IUL) is because they believe that they can finally harness the strong equity returns of popular indexes, just like the index-track ETFs or unit trusts that tracked MSCI World, S&P 500 and Nasdaq.

More and more Singaporean investors realize that actively-managed funds cannot consistently beat their benchmark index. A more fundamentally sound way to invest is to invest in the benchmark index itself. The evidence of history shows that If you hold long enough, you can get great equity returns.

Indexed UL paints to an interested prospect S&P 500, Nasdaq level returns, instead of the traditional crediting rate of a traditional UL that is more fixed income like.

Here’s some local Singapore examples:

- Singlife Legacy Indexed Universal Life has the option of S&P 500 or Nasdaq 100

- HSBC Life Diamond Prestige IUL II has S&P 500, Nasdaq 100, the volatility controlled indexes of S&P Global Diversified 7.5% TCA and S&P US Tactical Multi-Asset 4.5% TCA 0.65% Decrement Index

- China Taiping Infinite Indexed Legacy’s option are more volatility-controlled indexes such as S&P 500 DRC 10% Index ER and UBS-CSOP GAMA Core Index ER. ER stands for Excess Returns.

They have some popular UL with popular indexes that you may recognize and also some indexes with some really cheem names.

Planners, private bankers would also paint a picture of higher return with these IUL, which means that your policy are less likely to lapse (policy value depleted, goes to zero prematurely, no more coverage).

But what if I tell you the reality is that your ‘indexed’ return is not exactly similar to the returns of your indexed funds. One simple difference is that these are price index which means you lose out on the dividends that you would typically earn in a normal physical index fund.

What many may not immediately realize is that the returns of an Indexed UL is very much based on an options budget which is highly dependent on the income from a fixed income heavy portfolio.

If we peel back the layers, you might realize the more you want to steer away from fixed income, the more your returns actually is related to fixed income.

Peeling Back the Layers: How Your Index UL Policy is Structured (from an Investment Person Perspective)

I think this might be the uncommon time you see a universal life policy described this way but any products that involves some sort of investment cannot escape the potential and limitations of the underlying investments.

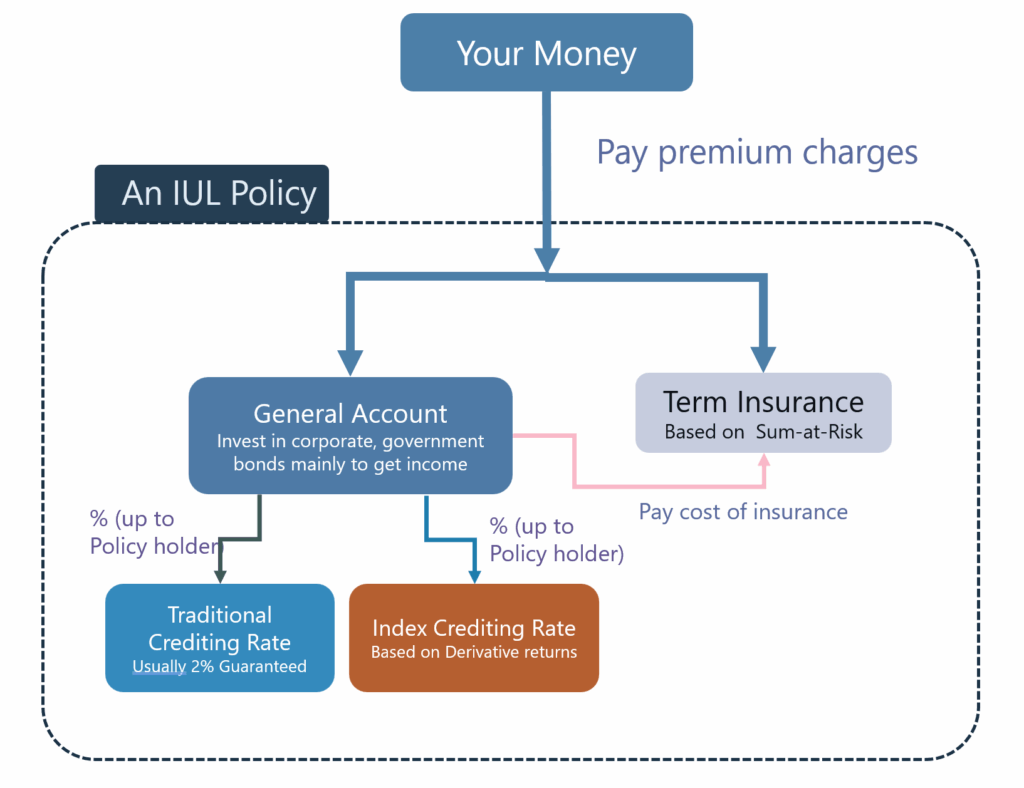

If you are a 50 year old Singaporean male non-smoker that decides to buy a Singlife Legacy Indexed Universal Life by putting in a premium of US$1 million. This will cover you about US$4.4 million.

At the start, probably around 80% of your US$1 million would be invested and your money will look roughly like the following IUL framing:

Your US$800,000 together with other policy money would be in a General Account. This will depend on how your insurer invest.

The investment portfolio is very opaque in my opinion. Not a lot is known about the allocation.

In the US, it tends to be rather fixed income heavy. One of the rare known allocation belongs to Manulife, which is closer to a 20% Equity and 80% Fixed Income allocation.

With such a fixed income heavy portfolio, a significant allocation would be investment grade fixed income which provides a coupon income. The equities are likely to be dividend focused.

This provides a coupon income that is very dependent on recent interest rate but because the portfolio has a pretty intermediate or even long maturity, the coupon income will shift as the interest rate regime changes.

Now this coupon income after deducting the administration cost will be what your policy earn. What kind of return would be the policyholder’s choice.

The policyholder has the choice to allocation a percentage to Index Crediting Rate, whose return will be based on derivative returns and a percentage to Traditional Crediting Rate. You can go 100% to each side, or 50%/50% as an example.

I suspect under certain people’s influence, many would choose 100% based on Index Derivative returns.

Now here is a similar illustration but I focused on the policy holder’s options with the income from the portfolio:

Of course there are admin and cost of insurance that needs to be potentially deducted.

Now if you choose a significant allocation to Index Crediting rate, then the income from the portfolio will be a Budget to Buy Index Options.

Options, which is a derivative contract is how the policy express the Floor and Cap Return of an Indexed Universal Life Policy.

The Options Budget from the Portfolio Income is Used to Purchase a Bullish Call Spread

Suppose the Index of choice is the S&P 500.

The options budget will be use to purchase a bullish call spread which will consistent of:

- Buy a 12-month At-the-money (ATM) call option on S&P 500 Index.

- Sell a 12-month Out-of-the-money (OTM) call option on a S&P 500 Index.

The ATM call option gives you the positive exposure to any upside of the S&P 500 returns past the point that you purchase. When you sell an OTM call option, if the price of the underlying S&P 500 exceeds that price, you will need to deliver the underlying S&P 500 shares. You do not own any S&P 500 shares but since you have a ATM call option, technically, if you exercise it, you will get the S&P 500 shares that you can deliver.

Sounds complicated but essentially this option spread caps your return at the CAP rate and provides a FLOOR at 0.

It will look like such an options payoff diagram:

The purple line shows your potential payoff depending on the outcome of the underlying S&P 500 index. If the index price is above your ATM strike, you make profits equivalent to the underlying index. But if the price exceeds the strike price where you sell the call, that is the CAP and where your maximum profit.

How is the Floor achieve?

Well if the S&P 500 falls below where you bought it, you lose the total cost you pay for this bullish call spread on the S&P 500.

This cost is the options budget from the coupon income of the portfolio.

Essentially your premiums on your policy is okay! The premiums are invested in that fixed income portfolio and not the actual S&P 500 index itself.

Kyith Why is there a Need to Cap the Returns? Why Can’t We Just Buy an ATM Call?

Because the options are not cheap.

A few things influence the price of the options but the main thing is volatility. An option that is ATM has a much much higher implied volatility than one that is far away from current S&P 500 price, or far out of the money.

So in order to be able to gain exposure, they have to sell an OTM call to earn the premiums (when you sell options you earn the premium, some call this ‘dividends’, but it is essentially call premiums) to finance partly the ATM call purchase.

Kyith, is the Cap on Return Always Fixed at 10% just like in the Product Illustrations?

No.

That is just an illustration on a brochure. This may be the first “be careful of insurance illustration” portion.

Options can be expensive or cheap,

- If options are more expensive -> need more budget -> Cap will move nearer -> limit positive upside.

- If options are cheaper -> need less budget -> Cap can be further -> increase positive upside.

So Why is Interest Rate a Big Deal for Indexed Universal Life Policies?

In order to have greater exposure to the Index, you need… a larger Options Budget;

- Higher interest rate regime -> higher fixed income coupon income -> larger options budget -> greater index exposure

- Lower interest rate regime -> lower fixed income coupon income -> lower options budget -> lower index exposure

The chart below is compiled from the Federal Reserve Economic Data of the 10-year US Treasury yield since the 1960s:

I think just by looking at this you kind of see that the income from a fixed income heavy portfolio is not going to stay static.

And that means the options budget is not going to be static.

Most policyholders thought that only if they leverage on the universal life policy, they should be more concern about interest rate but if your income is so important to give your index exposure, then you kind of need to wonder how interest rate would be.

But i think there is also nothing much you can do.

A lot of us have no control over the interest rate! Much more if we are holding over 20-30 years.

Your Future Index UL Policy Value is Not As Predictable as Policy Illustration You see in the Brochure.

If we recap what we understand, your returns would be highly influenced by:

- Interest rate regime.

- Volatility of the underlying index.

- Index returns.

If you realize that both of these are not stable, and you cannot predict them easily then what does that mean?

- Cap Rate is not firmed as what the brochure illustrated.

- Participation Rate is not firmed as what the brochure illustrated.

- Your exposure to underlying index returns is not firmed as what the brochure illustrated.

- Index returns are uncertain.

You know what is more certain? The policy charges, policy admin costs haha.

Upside is uncertain, costs are certain.

But this is not something that readers of Investment Moats are not unfamiliar with. Traditional fixed income and equity ETF/ unit trusts have this uncertain return characteristics for a long while.

And Indexed UL return is no different.

It doesn’t mean that an Indexed UL is a scam or what.

It’s just that too often someone might guide you or you guided yourself into thinking the dynamics of a universal life is so much more predictable than traditional investments such as property, fixed income and equities.

Kyith, if Returns are Uncertain, Would an Indexed UL Still Stand a Lower Chance of Premature Policy Lapse?

I would just say that how much initial premiums that a policy holder has to put in is based on the credit rate used. The crediting rate used for an indexed UL is much higher than the traditional UL.

Because of the higher crediting rate, the premiums you need to put in today is lower than the traditional UL.

So what happens if… the actual returns is less than the planning crediting rate?

Policy may not have reach its matured value later in life, when the policyholder is older, and when the cost of insurance is more significant. This just puts more stress on the policy and that increases the chance of earlier policy lapse.

But in a way, I kind of think the culprit here may not be that the UL is a scam or the poorer returns.

It is actually the GREED of the policyholder.

They could have setup the policy to be more conservative. But usually what attracted them in the first place is something. And because of this something, they might not want to setup the policy in a conservative manner.

What’s More Important to You

I have this problem with not just an Indexed UL policy but traditional universal life policy in general.

Whenever I ask someone who is interested about a universal life policy, it seems that he/she are more interested in the leverage, or the multiple times of payout if the policyholder passes away relative to the premiums paid.

In most situations, I wonder if the person has even taken care of planning for their goals that they are likely more concern with such as retirement income or other more immediate things that needs to save up for.

Do people really think about leaving a legacy when other more important thing is unclear?

The less firm answer I hear, the more I felt that it is greed motivating people more than an actual need. But what they could not see unfolding are a few years later they end up with multiple universal life policies that are bought on leverage, not really sure what they are suppose to do if it is their retirement plan or suppose to leave for legacy.

I think many get themselves into trouble not always because its always the planner, agent, private banker’s fault.

Its you making yourself fall in love with insurance policy brochure illustrations. Taking sales pitch as the eventual realistic results.

Again and again.

Universal life policies are not really evil but they are suitable if you have a specific need. They might not be the only solution to achieve that.

Hell, I will just leave money that is enough for my next generation just by keeping them in plain old cash, fixed income and equities.

Kyith, How Sure Are You that Beneath all this, these IUL Work this Way?

I think this might be the more uncommon times you see IUL talked in this manner but we are in a time and age that if I said something outlandish you can easily verify.

You can ask a few different questions to your favorite AI LLM and it can answer you:

- Are indexed universal life return really based on options budget?

- What does the general account of an IUL policy typically invest in?

- Aren’t IUL exactly invest in traditional diversified equities?

- What influences the returns of an IUL besides the structure cost?

- Do you mean to tell me the cap rate, participation rate that I see in insurance brochure of an iul is not confirm one?

- How different from the illustrated return in a indexed universal life brochure in reality if fixed income income budget is driven by interest rate regime?

AI’s limitation may be what the user of AI do not know. You will only know some questions to ask if you are such a strong critical thinker. Not everyone is.

Again, I am not saying something ground breaking: Your outcome is not certain relative to product illustrations. This is the same for many traditional products and investments.

If after all my mumbo jumbo explanation, you felt that you have more questions, are still interested in universal life and would like to speak to a more trusted, human adviser of universal life, you might want to touch base with my friends at Havend.com.

Fill out a contact form. My friends Mei Zeng and Jayla will put you through to an insurance specialist. You can then explain why you are interested in purchasing a universal life policy, for this reason, that reason, do they really work this way or that way to the insurance specialist that you speak to.

They would also carry the Singlife Legacy Indexed Universal Life, China Taiping Infinite Indexed Legacy, HSBC Life Diamond Prestige that you might be pitched before or interested in.

Whether it is Providend or Havend, we are more goal-focused and if there is less of a reason to use a universal life to implement what you need, you are better implementing in more sensible ways. Havend probably know the guardrails to make your universal life policies safe.

Which is probably a pretty important thing?

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

If you’re thinking of opening an Interactive Brokers account, my referral link is here.

As the new account holder, you’ll receive USD 1 in IBKR stock for every USD 100 you deposit, up to USD 1,000 in shares — so a USD 10,000 deposit gets you USD 100 in IBKR stock, and the bonus is capped at USD 1,000 for deposits of USD 100,000 or more. A few other things to know: the minimum deposit to qualify is USD 10,000, done within 30 days of opening, and the bonus shares are locked up for one year from the award date. The promotion is currently active, and using the link costs you nothing extra. On a separate note, if you haven’t already, it’s worth taking a look at how IBKR’s share price has performed over the past five years — the stock you receive as a bonus isn’t just a token; it’s a stake in a company that has done quite well for its shareholders.

I break down my resources according to these topics:

- All my personal notes about how my philosophy behind my own money and how I manage it.

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I work and do research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Fee-only Wealth Advisory Firm Providend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith’s current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

Welch's Fruit Snacks - Mixed Fruit, Summer Fruits - 0.8 Oz - 60 Pack

$15.99 (as of July 26, 2026 03:00 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Ameritex Waterproof Dog Bed Cover Pet Blanket for Furniture Bed Couch Sofa Reversible

$7.99 (as of July 26, 2026 02:55 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Bedsure Orthopedic Dog Beds Large Sized Dog - Washable Large Dog Cat Bed Waterproof, Comfort Dogs Couch Sofa with Washable Removable Cover, Pet Bed with Nonskid Bottom, Grey, 35"

$39.99 (as of July 26, 2026 02:55 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

SUPERDANNY Extension Cord,Flat Plug Surge Protector Power Strip,10Ft | 8 AC & 4 USB Ports (2 USB C),Surge Protector with 1050J,Desk Charging Station for Home Office,College Dorm Room Essentials

$12.98 (as of July 26, 2026 02:56 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Post Comment