Why Your Great-Grandkids Will Laugh at How Broke We Were: The Billionaire Boom Coming Sooner Than You Think

So, picture this: Your 100-year-old, famously frugal Great-Aunt Maggie passes away, and you brace yourself for… what? A quaint little bungalow, a stack of dusty papers, maybe some probate drama? Well, buckle up — because it turns out Maggie wasn’t pinching pennies; she was quietly sitting on a $1 billion fortune. How on earth did she pull that off without a single flashy investment move, an advisor’s nudge, or even panicking through the market crashes? The secret? A simple, almost stubborn strategy: do absolutely nothing. No flashy trades, no tax tricks, no timing the market — just letting time and the mighty American stock market work their magic over a century. Intrigued? Let’s dive into how the slow and steady really does win the wealth race, and why your inheritance might not be the jackpot you imagined once taxes and fees come knocking. Ready to unravel Aunt Maggie’s millionaire mystery? LEARN MORE

Your 100-year-old spinster Great-Aunt Maggie dies. The family solicitor calls you in. You are expecting a small bungalow, several boxes of yellowing paperwork, and perhaps a lecture about probate.

Maggie had always seemed almost aggressively frugal. She wore old clothes. She walked to the library. She grew vegetables. She did not own a car. As a child, you vaguely wondered if she might be poor.

Apparently not.

Because Maggie’s estate turns out to be worth about $1bn.

How?

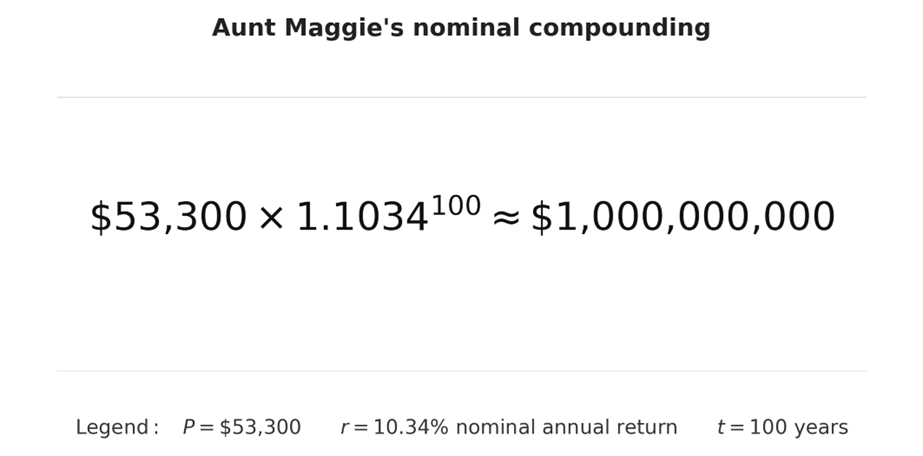

You’d always had a vague idea that Aunt Maggie had once been American. It turns out Maggie’s father was a notable American financier. In 1926, when Maggie was still in her cot, he put $53,300 into the JPMorgan S&P 500 Zero-Fee Magically Accumulating No-Tax Miracle Fund.

Then Maggie did the hard bit.

Nothing.

Maggie did not sell. She did not switch platforms. She did not rotate into Japan in 1989. She did not decide Cisco looked cheap in 2000. She did not panic in 2008. During COVID, she didn’t go on TV and cry. She just went to get her vaccine.

She did not pay an adviser 1% a year to ask her whether she had an attitude to risk.

Maggie just lived to 100 and let America do its thing.

Neat.

Magical thinking

Now to be clear, no such fund existed. Or could have existed.

The S&P 500 did not take its modern 500-stock form until 1957. Retail index funds did not exist. Accumulation share classes did not exist. Zero fees did not exist – and taxes certainly did.

But let’s leave those implementation details aside for a moment.

Maggie has compounded her way to billionaire status.

Unfortunately, you have not.

Heirs and graces

We’ll assume Maggie was UK-domiciled in the end and her estate subject to UK inheritance tax.

Ignore allowances because this is billionaire maths – the estate pays 40% inheritance tax (IHT).

So you inherit $600m.

Still an excellent result. But no longer billionaire status.

The first thing that happens after a century of perfect compounding is that HMRC turns up and removes 40% of the mountain.

$1 billion to one in the stock market

Here is the Maggie checklist for getting to one billion:

- Start early

- Start with a large sum

- Own one of the best-performing major stock markets of the next century

- Pay no fees

- Pay no taxes

- Do not spend any of it

- Do not sell, gift, switch, merge, rebalance, or otherwise crystallise a tax event

- Finally: do not die

Simple.

Time

Compound interest is often called the eighth wonder of the world:

Many people understand the compound interest formula. Hardly anyone behaves as if they believe it.

At a 10.34% nominal CAGR for US equities, Maggie needed only $53,300 to get to $1bn over 100 years. But give her 50 years and she needs $7.3m. With 30 years she only needs… $52m.

This is why compounding is exceedingly dull. It takes decades for anything to happen:

The 10.34% column is the Aunt Maggie thought experiment scenario: nominal US equities, no tax, no costs, no product failure, no bad behaviour, and a century of hindsight.

For the grown-up model, I am going to use 5.2% real as a long-run global-equity return assumption. That is the long-term real equity return (in the past!) per Dimson and Marsh.

At 5.2% real, the starting sum needed to reach $1bn in today’s money after 100 years is:

Call it $6.3m.

That is the clean answer. Your ancestor did not merely need to be sensible. They needed to be rich already.

But let’s face it, plenty of Monevator readers are.

Maggie owned the winner

The S&P 500 is pretty much the best-performing stock market over the last century.

If Maggie had been born German, for example, it would have been a different story. But we’ll assume we’re all investing in 100% global equities nowadays, because we don’t believe in picking markets any more than we believe in picking stocks.

The leaks

Let’s take the clean $6.3m starting pile that becomes $1bn after 100 years at 5.2% real.

Then we’ll let the British state, fund managers, and biology have a go at it.

The model I’ll use is deliberately simple:

- 5.2% real gross equity return

- 0.20% annual implementation cost

- 2.0% dividend yield

- 39.35% additional-rate dividend tax

- 0.5% FX spread on foreign-currency distributions, equal to a 1bp annual drag on a 2% yield

- 40% IHT events at years 30, 60, and 90 (assume each generation just leaves assets to the next)

- Allowances, bands, reliefs, and clever planning ignored

Again we’ll assume that not a penny is ever spent from the pot.

A 0.20% annual fee turns the clean $1bn into $827m.

Taxing a 2% dividend yield at 39.35% creates a 0.787% annual drag. With the fee included, the family ends with $390m.

Add a 0.5% FX spread on those same distributions and you shave off another $4m.

The family is now at $386m.

Then three IHT events take the $386m to $83m:

The line chart below is the same argument in picture form.

The top dark blue line is the spreadsheet. The chopped blood-red line is reality.

Yes, Britain has a wealth tax

Whether or not Charlie Munger ever actually said it, the aphorism is correct: the first rule of compounding is never to interrupt it unnecessarily.

Dying is quite the interruption. Especially in the UK, where Maggie’s estate pays 40% IHT.

Of course, you can give your fortune away at least seven years before you die, assuming you know when that will be. But if you gift chargeable assets then the gift is normally a disposal for capital gains tax (CGT).

People occasionally suggest that Britain should have a wealth tax. Is that as well as this one? Or instead of?

Will your fund make it to 2126?

The spreadsheet says: buy global equities and wait.

Fine. Which fund?

We are asking a product to survive for 100 years. It must keep its mandate, stay cheap, avoid forced mergers, avoid weird domicile changes, avoid legislation, and remain available on future platforms.

There are, to my knowledge, no global equity index funds that have done this.

But some investment trusts have! The AIC has a list of investment companies launched before King Charles III was born. Several are more than 100 years old.

The AIC’s 30-year return table includes:

| Trust | Launch date | £1,000 after 30 years | CAGR |

| F&C Investment Trust | 19/03/1868 | £14,110 | 9.2% |

| City of London Investment Trust | 01/01/1891 | £10,635 | 8.2% |

| Scottish Mortgage | 17/03/1909 | £27,887 | 11.7% |

| Alliance Trust | 21/04/1888 | £12,268 | 8.7% |

I could not find a clean, comparable 100-year total-return table that I would trust enough to print.

That absence is itself the point. But the table does show that collective investment vehicles can live for more than a century.

Are tax wrappers any help here?

If you’ve managed to get $6m – about £4.5m, our required starting capital to get to a billion – into an ISA, then well done.

But I bet you’re over 60.

And there lies the problem: the ISA tax shelter is only effectively inheritable by a spouse, so the wrapper dies with the younger spouse, unless you keep remarrying younger people ad infinitum. [Who knew tax planning could be so rock and roll?! – The Investor]

Still, ISAs can take a lot of the sting out of dividend tax and, of course, you can rebalance without worrying about CGT.

It also emphasises the tax-minimising principle: fill your ISA, your spouse’s ISA, and, if you can afford to, your kids’ and grandkids’ ISAs. Consider going into debt if you have to in order to make sure you use the annual allowance. [Like everything here this is not personal advice! Potentially very risky. Read the linked article, seek advice if needed – The Investor]

Pensions were a potential perpetual tax shelter for a while, enabling you to compound wealth down the generations with no dividend tax, CGT, or IHT. Unfortunately, that wheeze has been rugged by Reeves. (Yes, beneficiaries pay income tax on withdrawals, but the original pension got income tax relief on the way in, so call that a wash.)

Reeves’ actions also exemplify the tax risk. The rules keep changing, rarely to your advantage.

Once you’ve got a few hundred million in your ISA, will they come along with an ISA lifetime allowance?

The one weird trick that completely avoids IHT

Do not die.

The government has not found a way to close this loophole yet: your estate only pays IHT when you die.

So… don’t.

Unfortunately, living a long life is mostly down to luck. But there are a few things that you can do to improve your chances.

Just as we don’t give financial advice here, we don’t give health advice. But here’s a shortlist of things you can do in order to reduce your potential IHT liability:

- Don’t be overweight. This is now much easier to fix with money via drugs.

- Exercise: cardio, strength, balance, and enough mobility to get off the floor.

- Get vaccinated.

- Do not do obviously risky stuff.

- Proactively manage your health. The NHS is not going to do it for you.

So what would actually help?

Maggie already had all the answers:

- Start early

- Start with a lot

- Avoid putting all your eggs in one basket

- Minimise fees

- Mitigate whatever taxes you can

- Don’t spend any of the pot

- Try not to die

This time next century, you’ll be a billionaire. (Maybe.)

What is the point?

There is an obvious objection to all this.

What is the point of becoming a billionaire in 100 years if you don’t get to enjoy spending the money? You don’t want to never treat yourself because coffee will cost $1m in a century.

That pushback is totally fair.

But for some of us, the money itself has long since ceased to matter. It’s for the love of the game!

Be sure to follow Finumus on Bluesky or X and read his other articles for Monevator.

Lance Sandwich Crackers, Variety Pack, 3 Flavors, 20 Individually Wrapped Packs, 6 Sandwiches Each

$7.64 (as of August 7, 2026 02:53 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Pure Life Purified Bottled Water, 12 Pack - Still Drinking Water Enhanced with Minerals for a Crisp Taste - 16.9 Fl Oz - Toy Story 5 Packaging Graphics

$3.96 (as of August 7, 2026 02:53 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Milk-Bone Original Medium Dog Biscuits, 10 lb Box | 280+ treats, classic meaty taste, crunchy dog treats for dogs 20-50lbs, 15% protein, 12 vitamins & minerals, made in the USA

$14.97 (as of August 7, 2026 02:53 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Shark StainForce Cordless Stain, Odor & Urine Remover, 2 Tools, HX102BRN | For Carpets, Area Rugs, Upholstery, Cars & Outdoors, Dual-Activated Formula, Stain Eliminator & Wide Stain Tools, Caddy

$219.99 (as of August 7, 2026 02:59 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Post Comment