Bitcoin’s Surge Threatened: Is Strategy’s Overhang the Silent Killer Despite U.S.-Iran Deal Breakthrough?

Here’s a curveball for you: just when Bitcoin seemed poised to ride the wave of optimism sparked by the recent U.S.-Iran deal, Singapore’s QCP Capital throws cold water on the party — warning that Bitcoin might not cash in on this geopolitical cheer. Why? Well, it turns out Strategy, the big player backing much of Bitcoin’s institutional demand, might have a gaping hole in its dividend coverage. What does that mean in plain English? They could be forced to offload more of their Bitcoin stash to keep paying dividends, throwing a wrench in BTC’s upward momentum. With preferred stocks like Stretch (STRC) tumbling well below their intended value — and critics like Peter Schiff sounding alarms about looming share dilution — the scene’s getting a bit tense. Strategy insists it has decades of dividend coverage, but the market’s not buying the solace just yet. So, could this be Bitcoin’s stumble before it even gets going? Or is it just another bump on the crypto rollercoaster? Buckle up, this story’s unfolding fast. LEARN MORE.

Singapore-based crypto trading desk QCP Capital has warned that Bitcoin may fail to benefit from the U.S-Iran deal. According to QCP’s analysts, Strategy had limited coverage for dividend payouts. As such, it could be forced to sell more of its BTC holdings to meet this obligation.

Strategy has extended its runway to roughly 7.5 months before running out of cash for dividend payments. In the short term, we think this overhang may continue to prevent Bitcoin from fully participating in the broader macro-optimism.

The dividends are tied to its preferred stocks, led by Stretch [STRC], which have been instrumental in raising capital for BTC buys.

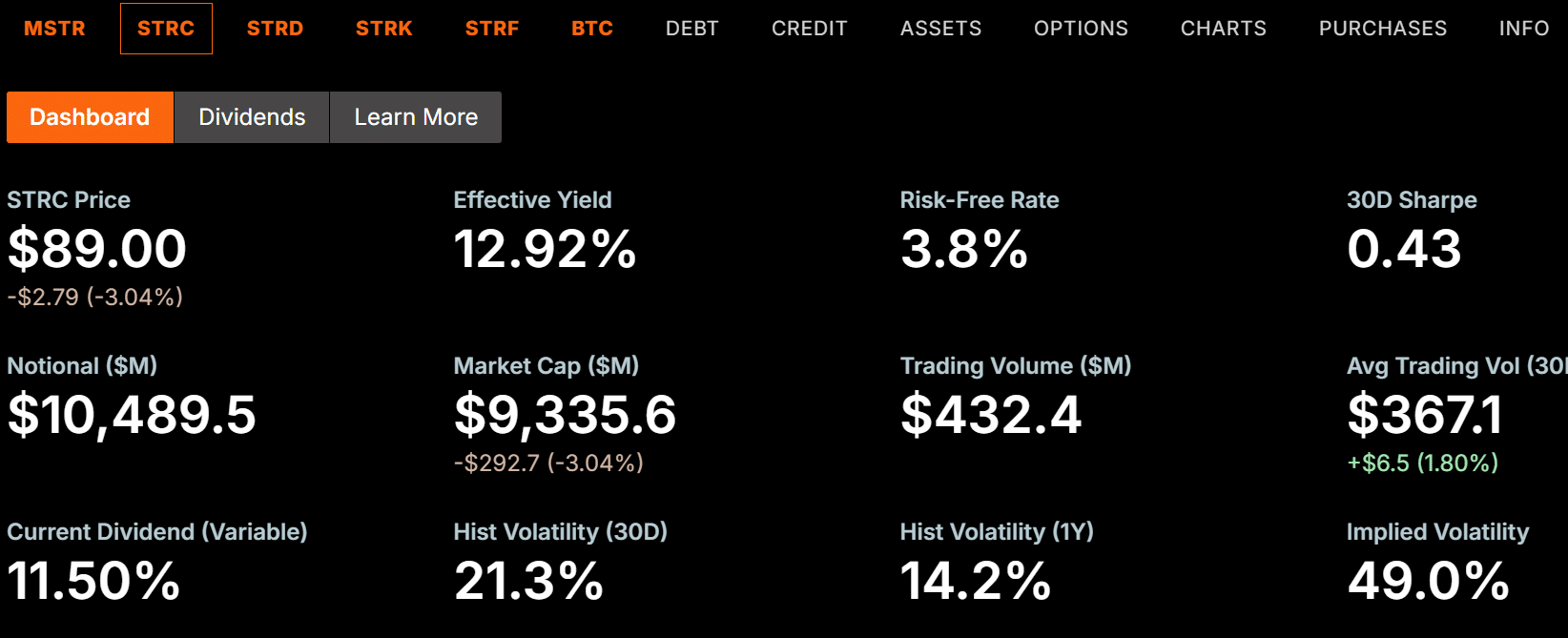

STRC is designed to maintain a price of $100 per share. However, at press time, it was trading at a massive discount of $89. This further underscored STRC distress and muted demand.

For long-time Bitcoin and Strategy critic Peter Schiff, investors of Strategy’s main stock, MSTR, will be the ones carrying the burden of the share dilution.

STRC closed at $89. Investors who paid $100 last month are down 11%. The current yield for new buyers is 12.92%. If Saylor raises the yield to 13%, he will have to sell even more MSTR at bigger discounts to fund it. If he doesn’t raise the yield, the STRC price will keep falling.

Strategy dismisses dividend coverage concerns

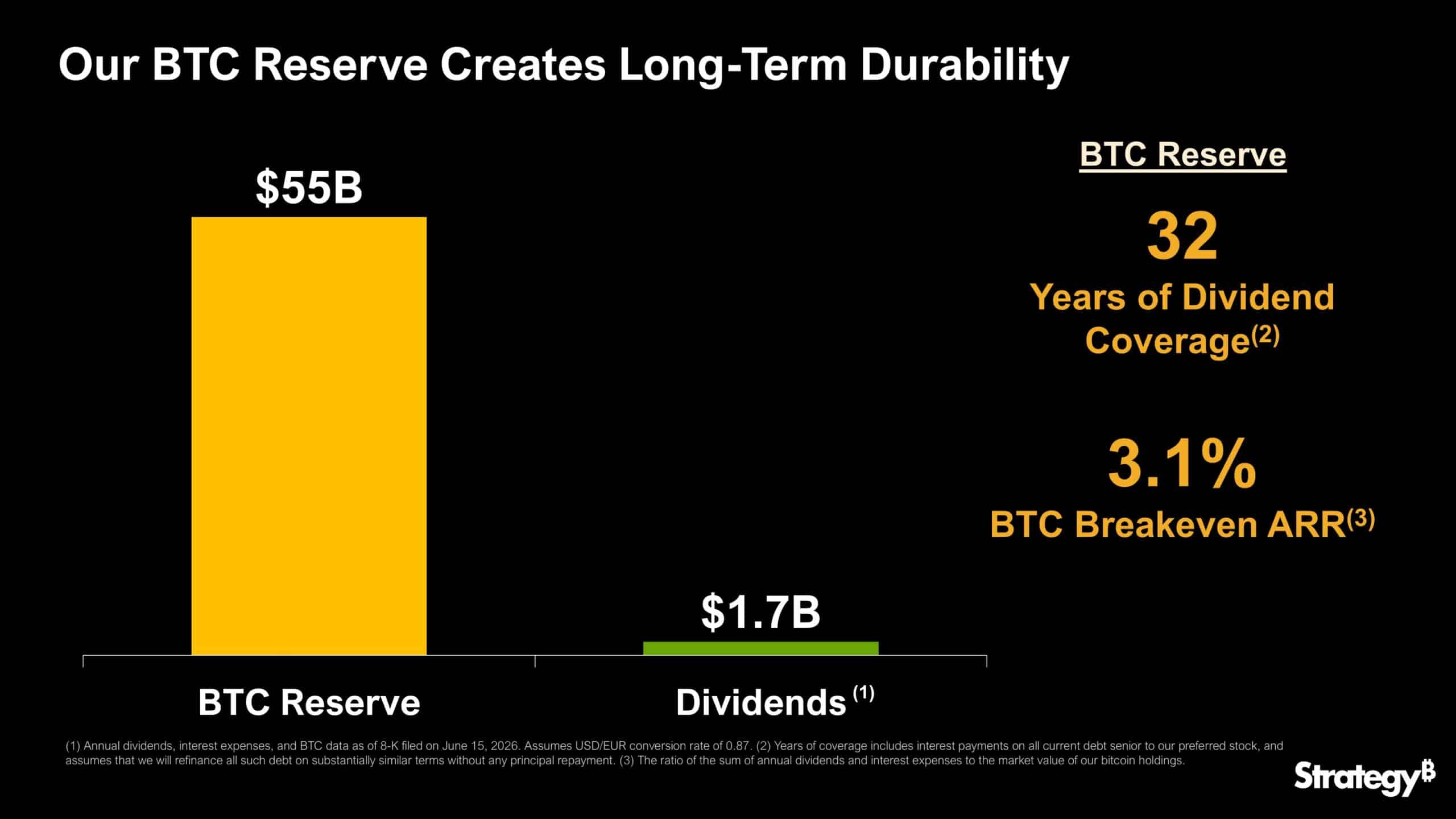

Amid intense FUD, Strategy recently cleared the air, noting that it has 32 years of dividend coverage. In doing so, it cited the current value of its BTC holdings.

However, critics were quick to point out that the asset would fall harder if Strategy begins liquidating its BTC holdings. In short, the coverage will shrink even further, similar to how its recent 32 BTC sell-off sharply dragged BTC’s price to $60K.

In fact, Strategy’s response raised more questions than the market assurance it was seeking. For instance – One market watcher said that the statement confirms the firm is a ‘permanent seller.’

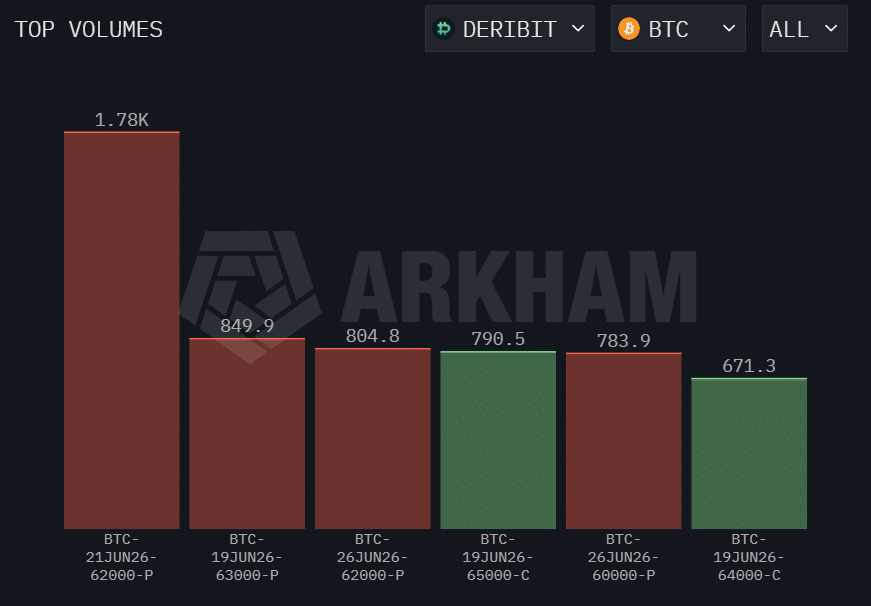

Worth pointing out, however, that BTC’s recent correction was accelerated by the Fed’s hawkish interest rate pause. In fact, sophisticated players, as tracked by Options data, have been actively hedging against a potential dip to $62K and $60K.

This was underscored by the high top Options volumes, especially puts (bearish bets) at these strike prices, as Q2 comes to an end.

Overall, despite Strategy’s overhang, the market didn’t expect a sharp BTC drawdown below $60K. However, the market’s positioning could change if Strategy confirms another BTC sell-off.

Final Summary

- QCP believes that Strategy could be forced to offload more BTC to fund dividend obligations.

- Strategy’s attempted market assurance with “32 years of coverage” sparked more fears and backlash.

Twinings English Breakfast Black Tea Individually Wrapped Bags, 100 Count (Pack of 1), Smooth, Flavourful, and Robust, Caffeinated, Enjoy Hot or Iced, 100 Teabags | Popular Tea Classic, Robust & Smooth, Naturally Caffeinated, 100 Foil Lined Individually Wrapped Bags, Enjoy Hot or Iced

$12.38 (as of August 3, 2026 03:03 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Purina Friskies Gravy Swirlers With Flavors of Chicken, Salmon and Gravy Dry Cat Food - 3.15 lb. Bag

$4.72 (as of August 3, 2026 02:52 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Cable Zip Ties,400 Pack Black Assorted Sizes 12+8+6+4 Inch,Multi-Purpose Self-Locking Nylon Cable Cord Management,Plastic Wire Ties for Home,Office,Garden,Workshop. By HAVE ME TD

$6.99 (as of August 3, 2026 02:58 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Veken Innovation Award Winner Stainless Steel Cat Water Fountain, 108oz | Automatic Pet Fountain Dog Water Dispenser with 3 Replacement Filters & Silicone Mat, Gifts for Cats, Dogs (Silver)

$26.99 (as of August 3, 2026 02:58 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Post Comment