Is FUTU Holdings on the Brink of Collapse, or Is This the Ultimate Investment Opportunity You’ve Been Waiting For?

Ever wondered what happens when a regulatory hammer crashes down on a fintech giant seemingly overnight? Yesterday, FUTU—parent company of the well-known local broker moomoo—suffered a staggering 27% stock plunge, briefly hitting a jaw-dropping 35% drop. Its rival, Tiger Brokers (ticker TIGR), wasn’t spared either, tumbling 25%. This seismic market shake-up didn’t come out of thin air; it followed a stern crackdown from Chinese regulators targeting unauthorized securities and futures activities in Mainland China. But here’s the kicker — 13% of FUTU’s funded accounts hail from Mainland China, a significant piece of the puzzle in this high-stakes drama. Is this the beginning of the end for Chinese retail investors dabbling abroad, or merely a harsh speed bump on FUTU’s journey? Buckle up, because we’re diving deep into the timeline, financial fallout, and what it all means for investors navigating these turbulent waters. Ready to unravel the details? LEARN MORE

img#mv-trellis-img-1::before{padding-top:75%; }img#mv-trellis-img-1{display:block;}img#mv-trellis-img-2::before{padding-top:67.28515625%; }img#mv-trellis-img-2{display:block;}

Yesterday the stocks of FUTU, the parent of local broker moomoo crashed 27%. At one point it was down 35%. It’s competitor Tiger broker (ticker TIGR) crashed 25%.

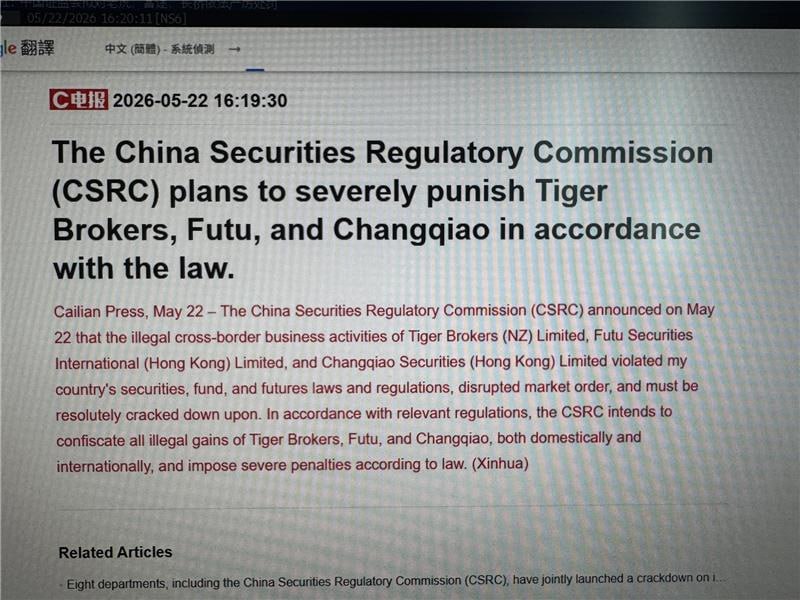

This was due to this announcement:

This feels like the ongoing regulatory concerns that plague Chinese firms since 2021. The brokers that were affected is Tiger Brokers, Futu and also Long Bridge.

The language used i this update was.. very stern. I can understand why people were spooked.

Futu updated investors on what they received:

The CSRC states that certain Futu entities in mainland China and Hong Kong (the “Related Companies”), without obtaining the requisite licenses or approval, conducted securities business, public fund sales business and futures business in mainland China, in violation of the Securities Law, the Securities Investment Fund Law, and the Futures and Derivatives Law of the People’s Republic of China. The CSRC proposes to order the Related Companies to rectify or cease such activities, confiscate illegal gains, and impose fines, with the total proposed penalty amounting to approximately RMB1.85 billion (approximately USD271 million). In addition, the CSRC proposes to impose a personal fine of RMB1.25 million (approximately USD 183,575) on Mr. LI Hua, the founder and CEO of the Company.

The proposed penalty remains subject to further proceedings and the final determination by the CSRC. The Company is entitled to submit statements, present defenses, and request a hearing. The Company will fully cooperate with the CSRC and exercise its lawful rights to safeguard the legitimate interests of the Company and its shareholders.

As of the end of the first quarter of 2026, funded accounts from mainland China accounted for approximately 13% of the Company’s total funded accounts.

So 13% of the company’s total funded accounts are from Mainland China. The Chinese government deem that allowing mainland Chinese to transact in overseas equity to be illegal.

This was not the first time and here are some historical tabulation:

- 11 Nov 2021 — First Warning to these brokers: CSRC verbally warned FUTU about allowing mainland Chinese investors to transact in offshore equities, flagging it as illegal. FUTU stock gapped up 5.5% that day.

- 30 Dec 2022 — Ban on New Account Openings. CSRC ordered FUTU to stop onboarding new mainland China customers and to “rectify illegal operations.” Existing customers were allowed to continue trading and could still deposit fresh funds. This is the action that caused FUTU to begin its international diversification push in earnest. FUTU stock gapped down 28% that day.

- 19 May 2023 — App Store Removal. FUTU voluntarily removed its apps from Chinese app stores as a compliance gesture. No reaction.

I just want to show the price action when they announced that new account openings were banned and since then:

You can also see where were my purchases on Crystalys.

So this is not a new news.

What spooked the markets this time is a few things:

- A one-time penalty.

- 2-year deadline where the China operations have to shutdown fully from this 22nd May announcement.

- confiscation of illegal gains.

- FUTU still has a significant China exposure.

What is now known is the CSRC proposes to order the Related Companies to rectify or cease such activities, confiscate illegal gains, and impose fines, with the total proposed penalty amounting to approximately RMB1.85 billion (approximately USD271 million). In addition, the CSRC proposes to impose a personal fine of RMB1.25 million (approximately USD 183,575) on Mr. LI Hua, the founder and CEO of the Company.

So the penalty is clearer the big overhang is that the market things that FUTU derives a significant amount of future revenue and profits from these Mainland Chinese accounts. FUTU announced that mainland China accounts for 13% of their total funded accounts. We will discuss more on this later.

If there are some takeaways, it is that this is not new, an ongoing thing. Since 2022, FUTU and the other brokers should have stopped adding mainland accounts. The question is more of whether they still made significant revenue and profit contribution. More on that later.

Here is a clearer view of the difference in the announcement this time versus the 2022 one:

| 2022 Action | 2026 Action | |

|---|---|---|

| New account openings | Banned | Still banned |

| Existing clients — trading | Allowed | Banned |

| Existing clients — deposits | Allowed | Banned |

| Existing clients — withdrawals & sells | Allowed | Still allowed (only action permitted) |

| Timeline | Indefinite rectification | 2-year deadline then full shutdown |

Existing mainland Chinese can still use their existing accounts to trade overseas but with this ban, they cannot any more and only allow to withdraw. This means that for the past 4 years, the mainland Chinese account holders are still allow to add money in.

The winding down terms:

- 2-year grace period: existing mainland clients can only sell and withdraw — no buying, no new deposits

- After 2 years: full shutdown of all mainland-facing digital infrastructure (websites, apps, servers inside China)

The Likely Impact Financially to FUTU

Perhaps let me put out some key financial figures here first so that we can consider if the market made a significantly more pessimistic view than this actually is.

What I hate about analyzing an overseas company like FUTU is to consider the American Depository Shares (ADS) is to figure out the market capitalization.

Share Structure — Important: 1 ADS = 8 Class A Ordinary Shares

| Item | Ordinary Shares | ADS Equivalent |

|---|---|---|

| Class A (publicly traded) | 765,788,970 | 95,723,621 |

| Class B (founders, not listed) | 355,552,051 | 44,444,006 |

| Total economic shares | 1,121,341,021 | 140,167,627 |

This was based on the FY 2025 report. FUTU’s actual ordinary shares should be closer to 1,133,282,856. I would think not a lot of difference.

Price Change Before and After the Fall:

| Item | Value |

|---|---|

| Price — pre-drop (May 21 close, est.) | ~$123.87 |

| Price — post-drop (May 22 close) | $89.76 |

| Drop on May 22 | −27.53% |

| 52-week high / low | $202.53 / $100.50 |

| Market cap pre-drop (all shares) | ~$17.36B |

| Market cap post-drop (all shares) | ~$12.58B |

Here are some of FUTU’s most recent financials:

| Item | HKD | USD |

|---|---|---|

| Cash & cash equivalents (company’s own) | HK$10,465,888K | ~$1.35B |

| Cash held on behalf of clients | HK$113,398,356K | ~$14.57B — NOT company cash |

| Total client assets (on-platform) | HK$1,233,000,000K | ~HK$1.23 trillion |

| Margin financing + securities lending balance | HK$67,700,000K | ~HK$67.7B |

| Total assets | HK$228,436,876K | ~$29.35B |

| Total borrowings (financial debt) | HK$12,143,237K | ~$1.56B |

| Total liabilities | HK$188,115,754K | ~$24.17B |

| Total shareholders’ equity (ex-NCI) | HK$40,001,188K | ~$5.14B |

| Non-controlling interests | HK$319,934K | ~$41M |

| Total equity | HK$40,321,122K | ~$5.18B |

| Net debt (borrowings − own cash) | HK$1,677,349K | ~$216M net debt |

FUTU balance sheet is rather healthy but I do think the balance sheet of most listed brokers are pretty healthy. They have US $216 million in debt and with US $1.35 billion in cash it helps put into perspective the impact of US 271 million in penalty.

Here’s how the Enterprise Value roughly look like considering these:

| Scenario | Total Market Cap | + Debt | − Corp. Cash | = EV |

|---|---|---|---|---|

| Pre-drop (May 21) | ~$17.36B | $1.56B | $1.35B | ~$17.57B |

| Post-drop (May 22) | ~$12.58B | $1.56B | $1.35B | ~$12.79B |

Here’s FUTU’s full year revenue and bottomline:

| Metric | Value |

|---|---|

| Revenue FY2025 | HK$22,846.9M (US$2,935.4M) |

| Net income FY2025 (GAAP) | HK$11,301.9M (US$1,452.1M) |

| Net income FY2025 (Non-GAAP adj.) | HK$11,644.9M (US$1,496.1M) — adds back HK$343M share-based comp |

| EPS per ADS — Basic (reported) | HK$81.36 = US$10.46 |

| EPS per ADS — Diluted (reported) | HK$80.24 = US$10.31 |

| P/E post-drop — Basic | 8.6x ($89.76 / $10.46) |

| P/E post-drop — Diluted | 8.7x ($89.76 / $10.31) |

| Gross profit margin | 87.1% |

| Operating margin | 61.6% |

| Net profit margin | 49.5% |

| ROE | 33.3% |

| Revenue growth (FY2025 YoY) | +68.1% |

| Net income growth (FY2025 YoY) | +108.0% |

You can kind of see where the PE is after the drop and its a low PE. For reference, IBKR trades at 34 times, UOB Kayhian trades at 15-16 times PE, iFAST trades at 24-26 times PE.

FUTU would have traded like UOB Kayhian before the drop, and now it trades lower than that. And it would be a good future research just how different or which is a better purchase at this point: UOB Kay hian or FUTU.

Aside from this, the main thing to note is that the one-time US$271 million proposed penalty would probably reduce their next year’s earnings one time but also given this kind of growth, would it matter?

I think it depends on how significant does those 13% of total funded accounts out of their accounts contribute to the bottom line.

China Versus Non-China Revenue Impact

The challenge is that FUTU does not split out their revenue by geography. The more they do this, the more it makes you wonder if those Mainland China accounts are the majority of the revenue driver. Remember that even after the 2022 ban, the mainland Chinese accounts can still put in money.

FUTU’s segment reporting uses two buckets:

- “Futu Securities Hong Kong” — includes both HK locals and mainland Chinese clients using HK accounts

- “Moomoo” — overseas brand covering Singapore, US, Australia, Malaysia, Japan, Canada, NZ

Based on the financials we can kind of infer the following shift in mix:

| Period | Mainland China (accounts) | Greater China* (accounts) | Overseas Moomoo (accounts) |

|---|---|---|---|

| Pre-2021 (est.) | ~50%+ | ~80%+ | ~20% |

| Post-2022 ban (est. 2023) | declining, no new adds | ~65%+ | ~35% |

| Q2 2025 | ~13%* | <50% | >50% ← milestone crossed |

| Q3 2025 | ~13%* | 46% | 54% |

| Q4 2025 | ~13%* | ~45% | ~55% |

| Q1 2026 (post-crackdown statement) | 13% (confirmed) | ~45% | ~55% |

*Greater China = Hong Kong + mainland China. Mainland China specifically confirmed at 13% as of Q1 2026.

Another area of clue is the Overseas Moomoo Commission Growth. The 20-F includes a geographic breakdown of commission income by subsidiary. The “Others” entity covers Singapore, US, Australia, Malaysia, Japan, and Canada — zero mainland China exposure. This is the cleanest proxy for non-mainland-China revenue growth.

| FY | HK Entity Commission | Others (Pure Overseas) | Others YoY | Others % of Total |

|---|---|---|---|---|

| 2022 | HK$3,514,765K | HK$492,877K | — (baseline) | 12.3% |

| 2023 | HK$3,197,605K | HK$747,174K | +52% | 18.9% |

| 2024 | HK$4,721,494K | HK$1,323,252K | +77% | 21.9% |

| 2025 | HK$7,825,932K | HK$2,746,812K | +108% | 26.0% |

| FY2022→FY2025 | +458% cumulative | 12% → 26% |

I think this table show the risks. FUTU earns not just commission but interest income revenue but that is almost similar to commissions. But this break down perhaps show that even with the ban in new account opening FUTU still derives a significant chunk of revenue from the HK Entity.

So how much is actual Hong Kong people and how much are Mainland Chinese?

If a significant amount is due to Mainland Chinese using this “loop hole” to invest outside and most are due to it, then a lot of the revenue and profits will go away.

The key regulatory issue is that CSRC’s jurisdiction is over mainland residents accessing foreign markets. If the client used a mainland Chinese address and ID when opening the account, FUTU would have classified them as a mainland China client regardless of where they physically opened the account (Hong Kong or China)

Epilogue

I stop short my analysis here because of how challenging it is to separate that HK entity portion. Given this, FUTU should have been down more compared to Tiger Brokers if the main bulk of those HK Accounts are mainland Chinese money.

If this is not the case, then this is a nothing burger.

FUTU after a year or two of pain can climb out.

We will see if FUTU can provide more updates.

I have FUTU in Crystalys, my portfolio for my less important money. You can see from the chart above where I was invested in.

Investing in individual stocks always comes with some risks. Usually, the risks surfaces only when shit hits this way. To be fair, those Chinese money was a strength of FUTU (if it is really significant) relative to other brokers.

I would look into Tiger Brokers Next. I think there are some opportunities.

Here are your other Higher Return, Safe and Short-Term Savings & Investment Options for Singaporeans in 2026

You may be wondering whether other savings & investment options give you higher returns but are still relatively safe and liquid enough.

Here are different other categories of securities to consider:

| Security Type | Range of Returns | Lock-in | Minimum | Remarks |

|---|---|---|---|---|

| Fixed & Time Deposits on Promotional Rates | 4% | 12M -24M | $20,000″ data-order=”> $20,000″>> $20,000 | |

| Singapore Savings Bonds (SSB) | 2.9% – 3.4% | 1M | $1,000″ data-order=”> $1,000″>> $1,000 | |

| SGS 6-month Treasury Bills | 2.5% – 4.19% | 6M | $1,000″ data-order=”> $1,000″>> $1,000 | |

| SGS 1-Year Bond | 3.72% | 12M | $1,000″ data-order=”> $1,000″>> $1,000 | |

| Short-term Insurance Endowment | 1.8-4.3% | 2Y – 3Y | $10,000″ data-order=”> $10,000″>> $10,000 | |

| Money-Market Funds | 4.2% | 1W | $100″ data-order=”> $100″>> $100 | Suitable if you have a lot of money to deploy. A fund that invests in fixed deposits will actively help you capture the highest prevailing interest rates. Do read up the factsheet or prospectus to ensure the fund only invests in fixed deposits & equivalents. |

This table is updated as of 17th November 2022.

There are other securities or products that may fail to meet the criteria to give back your principal, high liquidity and good returns. Structured deposits contain derivatives that increase the degree of risk. Many cash management portfolios of Robo-advisers and banks contain short-duration bond funds. Their values may fluctuate in the short term and may not be ideal if you require a 100% return of your principal amount.

The returns provided are not cast in stone and will fluctuate based on the current short-term interest rates. You should adopt more goal-based planning and use the most suitable instruments/securities to help you accumulate or spend down your wealth instead of having all your money in short-term savings & investment options.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Fee-only Wealth Advisory Firm Providend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith’s current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

Ultimate Assorted Candy Party Mix - 2 LB Bag - Mega Variety Bulk Assortment - Individually Wrapped Candy - Queen Jax - Variety Pack

$18.49 (as of July 30, 2026 03:02 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Blue Buffalo Health Bars Pumpkin & Cinnamon Dog Biscuits, 16 oz | Oven-Baked, Crunchy Texture, No Chicken By-Product, Corn, Wheat, or Soy

$4.98 (as of July 30, 2026 02:50 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Lance Sandwich Crackers, Variety Pack, 3 Flavors, 20 Individually Wrapped Packs, 6 Sandwiches Each

$7.64 (as of July 30, 2026 02:50 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Daily Multivitamin, Dog Allergy Support Chews is Human, 60 Chews | Salmon Oil & Vitamins Itch Relief– Skin & Coat Care, Helps Reduce Itching & Licking, Gut & Immune Supports

$29.99 (as of July 30, 2026 02:55 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Post Comment