Why Citadel’s AI Play Could Shatter the Rules of American Innovation—and Wealth Forever

Ever wondered if the AI revolution is really about wiping out jobs—or is it actually handing America’s entrepreneurs a sharper, mightier toolkit to build something fresh and fierce? Frank Flight of Citadel flips the script on the usual scare stories about AI displacement, arguing the true powerhouse move for the U.S. is creation, not obliteration. You see, America’s secret sauce isn’t just those megacorp giants or massive data centers—it’s the relentless grit of small businesses that make up nearly half of the GDP and keep more than 60 million folks working . These are the real game changers, using AI to bend the rules, lower the bar for what “scale” means, and turning ambitious dreams into thriving realities faster than the world even agrees on the risks.

When a tiny startup can punch way above its weight—automating, analyzing, marketing, and expanding with fewer hands on deck—it’s not just efficiency; it’s a whole new economic playbook. And yeah, while some worry fewer people per company means fewer jobs, Flight points out that if AI sparks a surge in new startups, more boats are setting sail than ever before. Plus, AI’s reach isn’t confined to Silicon Valley cubicles anymore—it’s seeping into every corner of the economy, making high-leverage roles bloom in unexpected places. It’s classic Jevons Paradox at work: make something cheaper and better, and suddenly, demand explodes instead of fading away. So, before you bet against the American builder, remember—they’ve just gotten handed a bigger, better engine, fueling the next wave of innovation and enterprise formation.

AI displacement is the obvious fear, but Frank Flight at Citadel argues the more powerful US story may be formation, not destruction. America’s edge is its ability to turn new tools into new businesses before the rest of the world has finished debating the risks.

The small-business sector is the key transmission channel. If AI lowers the minimum efficient scale, founders can do more with less, pool capabilities across roles, and make expansion decisions that previously did not clear the economic hurdle.

The labour story is less fixed-pie than the bear case suggests. Leaner start-ups may need fewer people per company, but if AI also triggers more business formation, the volume effect can offset lower labour intensity.

The real AI dividend may be diffusion. When AI-exposed roles start showing up outside their traditional home industries and in regions with lower prior exposure, it suggests the technology is spreading scale economics across the economy. Never bet against America when the builders have just been handed a bigger toolbox.

America’s hustle premium

Frank Flight at Citadel makes a useful point that should not get lost in the usual AI debate. American exceptionalism is not just about the Mag 7, hyperscale balance sheets, or the latest bottleneck in compute. It is also rooted in a much older operating system: innovation, adaptability, optimism, and the almost reflexive instinct to build something from scratch.

That entrepreneurial culture is not a soft slogan. America’s small-business sector still accounts for nearly 44% of GDP and employs more than 60 million workers. In other words, a huge part of the US economy is not run from glass towers or server farms, but from storefronts, workshops, garages, home offices, and founders who are usually one payroll cycle away from either expansion or exhaustion.

Flight’s argument is that this may become a unique advantage in the AI era. Until now, the market has mostly framed AI through the lens of frontier labs, hyperscalers, data centers, chips, power, and the enormous capital bill required to build the new digital railway. That framing is not wrong. It is simply incomplete. The more interesting second-order question is what happens when the tools of scale are handed to the smaller operators who never had access to them before.

AI lowers minimum efficient scale. That is the key phrase. It allows a small company to look bigger, move faster, automate more, market better, analyze deeper, and compete in areas that previously required a much larger workforce or a much larger budget. The local business does not suddenly become Amazon. But it may gain enough leverage to survive, expand, and attack niches that once belonged only to firms with deep benches and deeper pockets.

That matters because America has always been unusually good at converting optimism into economic motion. Academic work has long linked optimism with measurable behavior: self-employed workers tend to be more optimistic than wage earners, and more optimistic individuals are more willing to work harder, expect longer careers, and take more idiosyncratic risk. In market language, the US has always run with a higher embedded beta to reinvention.

This is where the AI displacement debate may be too narrow. Yes, automation can reduce the labor intensity of certain tasks. Some work will be compressed. Some roles will be hollowed out. But in an economy with high entrepreneurial velocity, the same technology can also broaden the range of viable businesses. It can turn one-person firms into three-person firms, three-person firms into regional challengers, and regional challengers into genuine competitors.

That is the hustle premium. AI does not just replace tasks. It increases founder leverage. It lowers the cost of experimentation. It reduces the friction of starting, scaling, marketing, coding, designing, servicing, and selling. In a country already wired for business formation, that can become a powerful compounding mechanism.

To be clear, none of this resolves the near-term market debate around capex returns, token economics, power constraints, or whether investors are again paying too much today for productivity that only arrives tomorrow. Those questions still matter. The rails have to be funded before the productivity train can run on schedule.

But Flight’s point is that the most durable AI dividend may not only be found inside the largest platforms. It may also come from the long tail of American enterprise. If AI gives the small builder more reach, more leverage, and more room to compete, then the real story is not just machines replacing labour. It is the American instinct to build being handed a bigger engine.

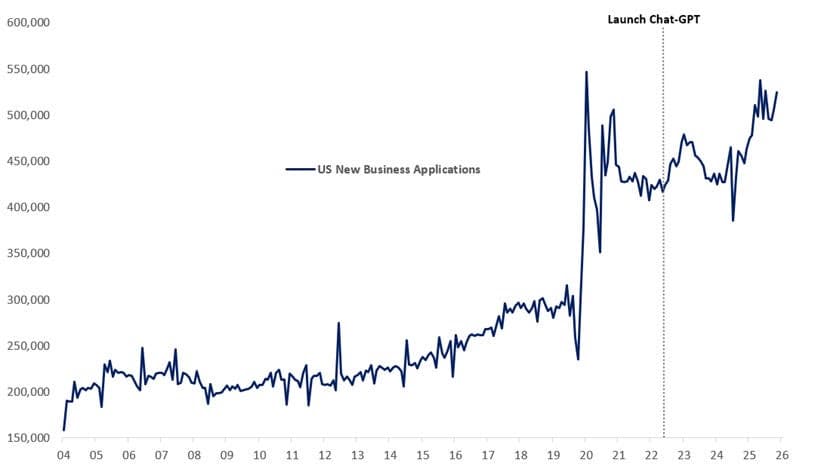

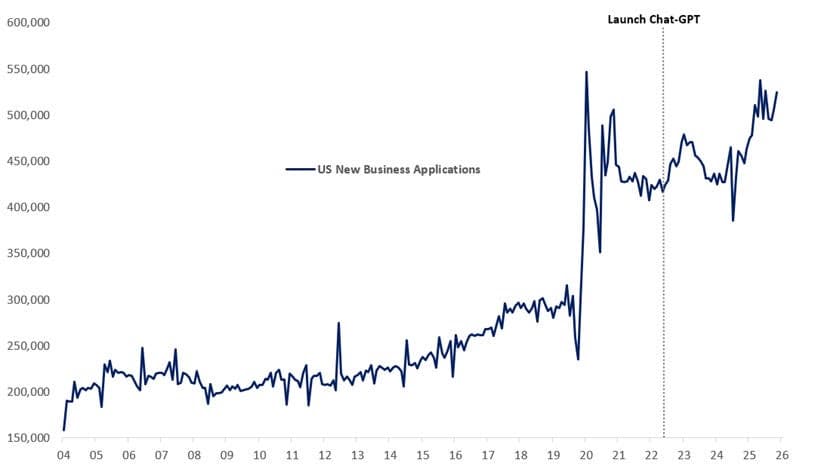

New business applications are surging higher

New Business Applications: Total for All NAICS in the United States

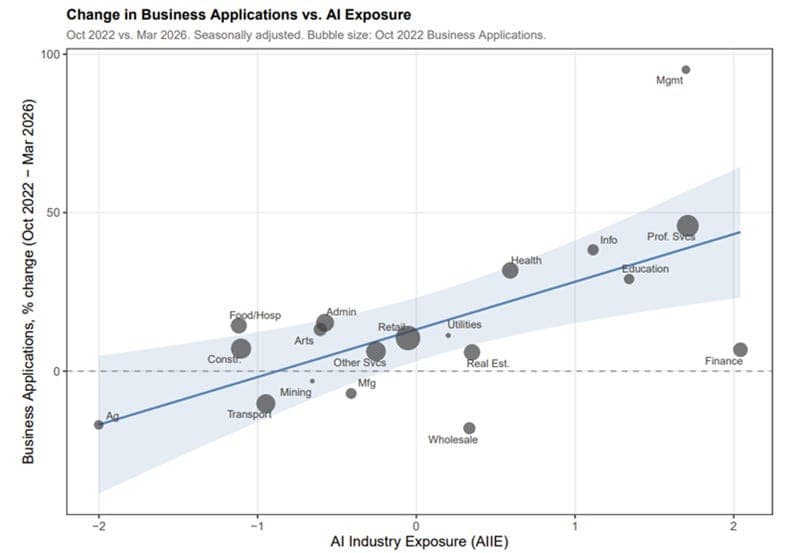

Nothing underlines Flight’s point more clearly than the surge in new business formation. Since the launch of ChatGPT, new business creation is up 24%, and the sector split is even more revealing. The areas with the highest AI exposure are also showing some of the strongest formation impulses. That suggests AI is not simply a cost-cutting machine or a labour-substitution story. It is lowering the drawbridge for new entrants. The sectors where AI can do the most are also the sectors where founders are moving fastest, which is exactly the kind of feedback loop that has long made the US economy difficult to bet against. Give American entrepreneurs cheaper tools, more reach, and more operating leverage, and they tend to turn the machine on before the rulebook has even been written.

New business formation appears positively correlated with AI exposure

Change in Business Applications vs AI Exposure, Oct-22 vs Mar-26

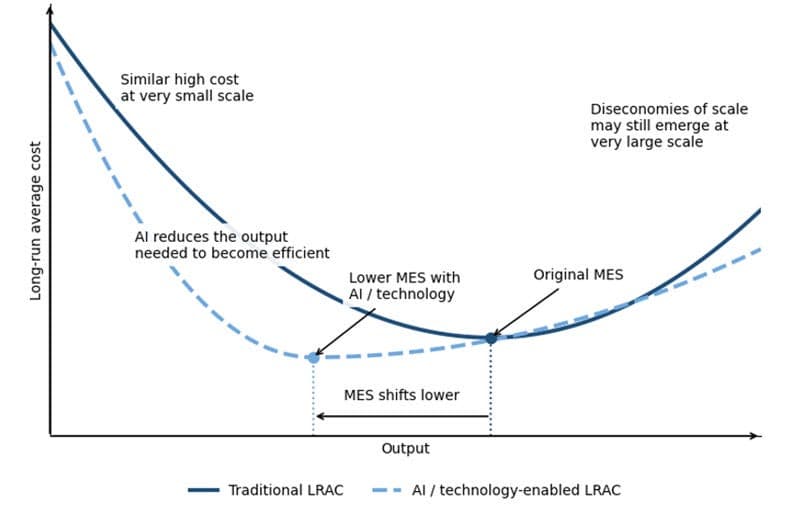

Efficient, cheaper AI changes the expansion math for small businesses. It lowers the minimum efficient scale, which is economist-speak for the smallest size a company needs to reach before it can operate at a sensible average cost. In plain English, AI lets small teams punch above their weight earlier.

That matters because a lot of small-business growth normally dies in the gap between ambition and payroll. The founder may need an accountant, a supply-chain manager, a marketing assistant, a compliance person, and someone to keep the office machinery moving, but the revenue base cannot yet support five separate hires. AI starts to pool those functions. It does not magically replace judgment, but it can stretch the productive range of each worker and make one hire cover more ground.

That is where the derisking comes in. Instead of borrowing aggressively or scaling too fast just to build the operating platform, a small business can grow more organically. Projects that once looked uneconomic start to clear the hurdle. Roles that previously did not justify the cost begin to make sense. AI does not just make companies cheaper to run; it can make the next stage of expansion financially possible..

AI reduces minimum efficient scale unlocking economies of scale earlier

Long Run Average Cost vs Output, Traditional and AI/Tech Enabled, Theoretical Diagram

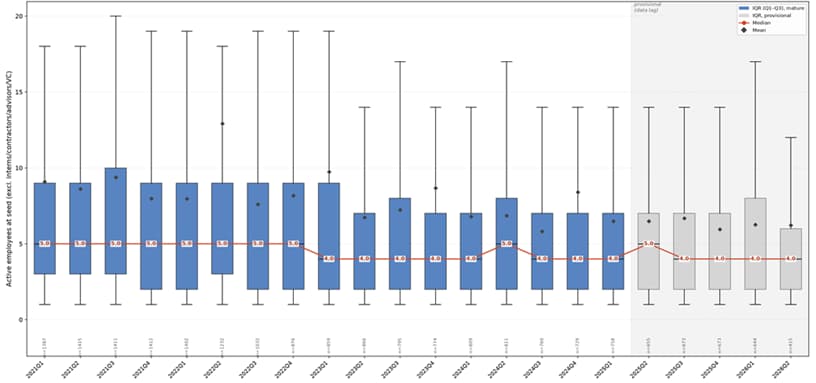

Flight adds another useful breadcrumb from Sequoia, one of Citadel’s largest external shareholders and partners. The Sequoia data show that the median start-up at seed stage moved from five employees to four in the first quarter of 2023, just one quarter after ChatGPT launched.

Now, that signal needs some caution. Rates were rising at the time, capital was getting more expensive, and broader hiring demand was already cooling. Not every leaner start-up is an AI story. Some of it was simply the cycle forcing founders to run with less fat.

But the timing still matters. AI likely gave founders more leverage at exactly the moment the funding environment demanded more discipline. In the old cycle, a seed-stage company often had to hire ahead of revenue just to build the basic operating scaffolding. In this cycle, AI allows the founder to delay some of that hiring, stretch the team further, and still get more done.

That is the real signal. The start-up is not just smaller because money is tighter. It may also be smaller because the tool kit is bigger. And if four people can now do what five people used to do, the economics of formation, experimentation, and survival start to change in ways that do not show up neatly in the first wave of AI market cap charts.

Sequoia data implies a decline in median number of employees at seed raise

Active Employees at Seed Raise, US Companies

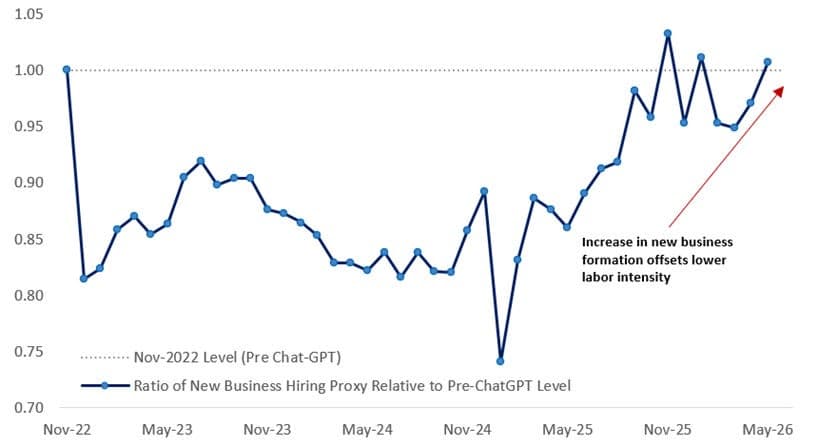

The obvious pushback is labour displacement. If AI lets start-ups do more with fewer people, does that not simply mean fewer jobs?

Flight’s answer is no, or at least not in the simple way the bear case suggests. Using Sequoia’s median employee count as a rough proxy for the labour intensity of new business formation, Citadel runs the basic math: median employees multiplied by new business formation. It is not a perfect measure, and it should not be treated like a payrolls report, but it is a useful back-of-the-envelope way to frame the trade-off between leaner companies and more companies being created.

The result is important. The first AI impulse may have lowered labour intensity, with seed-stage teams getting smaller. But as new business formation accelerated, that volume effect appears to have offset the lower headcount per company. On this rough approximation, implied hiring from new business creation now slightly exceeds its fourth-quarter 2022 level after an initial dip.

That is the key distinction. AI may reduce the number of people needed inside the average young firm, but if it also increases the number of firms that can be started, funded, and scaled, the macro employment effect becomes less straightforward. The bear case looks only at the smaller crew on each boat. The bull case asks how many more boats can now leave the harbour.

More new business formation now offsets lower labor intensity

New Business Formation x Median Employees at Seed Round

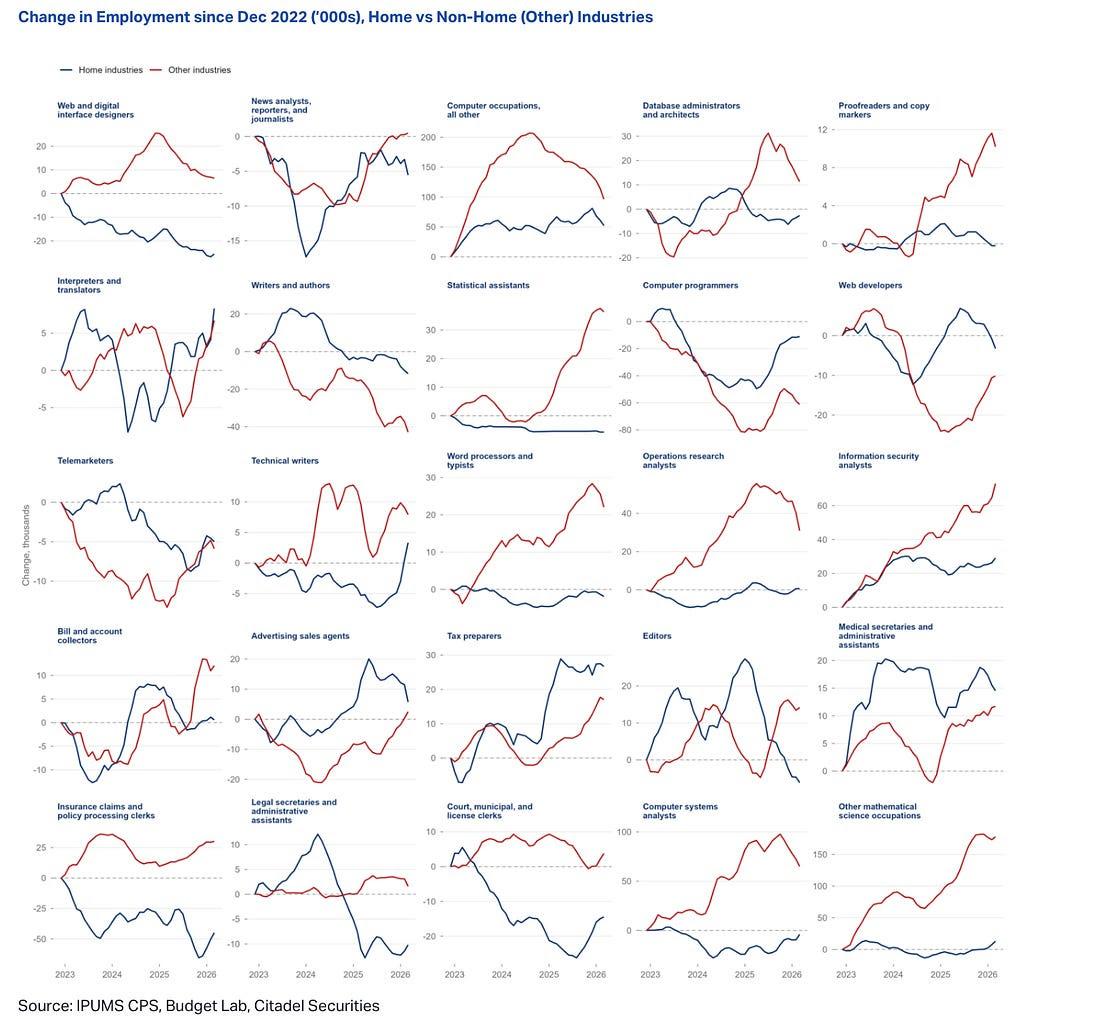

Flight then goes one layer deeper to test whether this “resource pooling” story is actually showing up in the broader labour market. Citadel combines more than 2.3 million individual employment records from the CPS monthly microdata, running from January 2022 through March 2026, with Budget Lab’s AI exposure scores across 541 occupations. The purpose is simple: to see whether AI-exposed jobs are being reallocated across industries and geographies rather than staying in their traditional silos.

The useful framing is “home” versus “non-home” hiring. A software engineer hired by a software company is home hiring. A software engineer hired by a law firm, retailer, logistics company, or media group is non-home hiring. The same logic applies to a cyber-security analyst working outside the classic information-security sector. In other words, AI is not just changing what technology firms do. It may be pushing technology-shaped labour into the wider economy.

That matters because Citadel finds strong home/non-home effects in several of the most AI-exposed industries, although not all of them. The signal is not universal, but it is broad enough to support the cross-hiring thesis. AI appears to be making certain skills useful in places where they previously did not clear the economic hurdle.

This is where Jevons Paradox enters the story. A productivity boost does not always reduce demand. Sometimes it makes the product, service, or capability cheap enough that usage expands. In this case, more efficient AI tools may be increasing the demand for AI-exposed workers by making their output more valuable across more sectors.

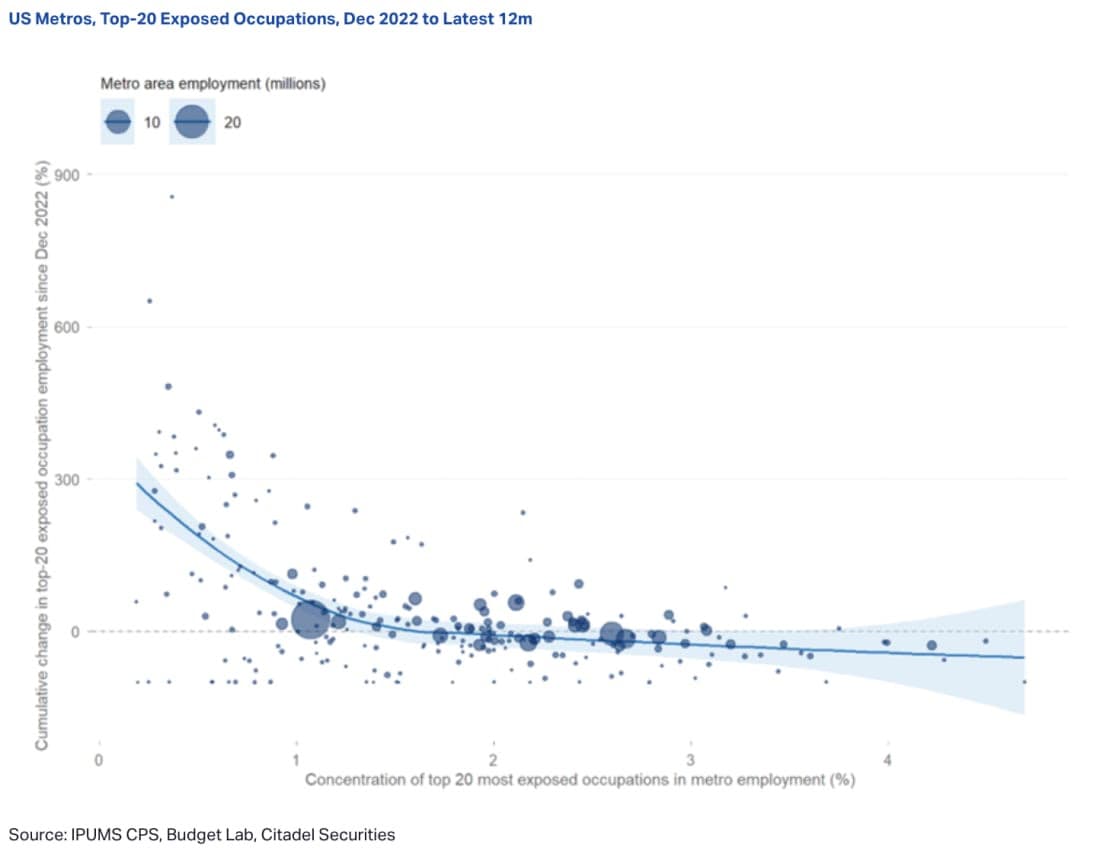

The geographic signal points in the same direction. Using the same microdata, Citadel finds that AI-exposed employment growth is occurring in areas that previously had the lowest concentration of AI-exposed workers. That is important. It suggests AI is not simply making Silicon Valley more Silicon Valley. It may be spreading the economics of high-leverage work into regions and industries where that work used to be too expensive, too scarce, or too difficult to justify.

Evidence of cross-hiring in AI-exposed occupations

Change in Employment since Dec 2022 (’000s), Home vs Non-Home (Other) Industries

Flight’s conclusion is that the AI displacement risk is real, but it is not the whole story. The US economy has always had an unusual ability to absorb shocks, rewire incentives, and turn disruption into new business formation. That is why the AI dividend may not accrue only to the obvious places: the frontier labs, the hyperscalers, the chipmakers, and the power-hungry data-centre buildout. It may accrue just as powerfully to the bedrock of the American economy: small businesses, founders, and entrepreneurs.

The acceleration in new business formation, especially in AI-exposed sectors, is the key counterweight to the lower-labour-intensity argument. If each company needs fewer people, that looks bearish in a fixed-pie model. But America rarely behaves like a fixed-pie economy. If AI allows more companies to be formed, more niches to be attacked, and more previously uneconomic projects to clear the hurdle, then the employment and productivity story becomes far more dynamic.

That is also why the non-home hiring signal matters. AI-exposed roles moving outside their traditional industries are evidence that the technology is diffusing into the broader economy, not just concentrating gains inside Silicon Valley. This is Jevons Paradox in real time: make a capability cheaper and more productive, and demand for it can expand rather than contract.

In effect, AI gives businesses access to scale economics before they have fully scaled. It lets smaller firms pool capabilities across functions, stretch scarce talent further, and lower the output threshold where expansion becomes economic. That does not eliminate the risks. It does, however, make the US uniquely positioned to turn AI from a displacement scare into another engine of enterprise formation.

Never bet against America — especially when the country’s builders have just been handed a bigger toolbox.

AI employment growth is happening in areas with lower concentration of AI-exposed workers

Bedsure Orthopedic Dog Beds Large Sized Dog with Removable Washable Cover | 35" Classic Big Dog Couch Sofa Waterproof, Comfy Bolster Sides, Nonslip Bottom, Cozy Pet Bed for Cats, Senior Dogs, Grey

$39.99 (as of July 28, 2026 02:56 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

[Apple MFi Certified] 2 Pack Lightning to 3.5 mm Headphone Jack Adapter, iPhone Aux Adapter Converter Dongle Audio Cable Compatible with iPhone 14 13 12 11 X XS 8 7

$8.99 (as of July 28, 2026 03:04 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

EHEYCIGA Orthopedic Extra Large Dog Bed, Waterproof Washable XL Pet Bed 44" | Non-Slip Bottom and Egg-Crate Polyurethane Foam Big Dog Couch Bed with Washable Removable Cover, Grey

$39.99 (as of July 28, 2026 02:56 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Babole Pet Blue Shark Dog Collar, Cute Boy Dog Collars for Small Dogs - Summer Ocean Pattern Female Male Dogs Collar, Durable Adjustable Pet Cartoon Collars with Quick Release Buckle S

$11.99 (as of July 28, 2026 02:56 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Post Comment