The Private Credit Crisis Nobody Saw Coming – Here’s What History Warns About the Next Big Shock

Before software companies became the darlings of private credit in the 2020s, there was another red-hot sector that had everyone swooning: shale oil and gas. Sounds surprising? Well, back in the 2010s, energy companies were the heavy hitters in leveraged finance, borrowing billions to chase the shale boom with fervor that rivaled today’s tech frenzy. But just like the software crowd, their day of reckoning came when oil prices plummeted—turning high hopes into harsh lessons on volatility, risk, and resilience. Intriguingly, one fund that took the hardest hits was Apollo’s business development company, then known as Apollo Investment Corporation (AINV), which later rebranded to MidCap Financial Investment Corporation (MFIC). Its journey through dramatic price swings, payment-in-kind restructurings, and investor emotions offers a vivid blueprint of what might lie ahead for today’s private credit investors. Ready to dive into a rollercoaster of financial thrills and chills that could shed light on the future of high-yield lending? Let’s unravel the saga and discover why discomfort in investing isn’t just inevitable—it’s a lesson waiting to be learned again and again. LEARN MORE

img#mv-trellis-img-1::before{padding-top:83.30078125%; }img#mv-trellis-img-1{display:block;}img#mv-trellis-img-2::before{padding-top:83.30078125%; }img#mv-trellis-img-2{display:block;}img#mv-trellis-img-3::before{padding-top:66.40625%; }img#mv-trellis-img-3{display:block;}img#mv-trellis-img-4::before{padding-top:42.421159715158%; }img#mv-trellis-img-4{display:block;}img#mv-trellis-img-5::before{padding-top:32.424242424242%; }img#mv-trellis-img-5{display:block;}img#mv-trellis-img-6::before{padding-top:27.089627391742%; }img#mv-trellis-img-6{display:block;}

Covenantlite reminds us that before the close link between private credit and software companies, the private credit were infatuated with another thing: Shale oil and gas!

Before Software, Private Credit’s Problem Child was Energy

In 2015, like software companies in the 2020s, energy companies were prolific users of leveraged finance (high yield, leveraged loans, and private credit) in the 2010s.

During the shale boom, U.S. energy companies massively increased their borrowing to fuel their drilling activities. In U.S. high yield, energy issuance totaled about $290 billion from 2008 to 2014, according to J.P. Morgan data, and the sector’s weight in the high-yield index climbed from 10% to nearly 15% by 2014.

The smaller shale producers borrowed more.

Like software today, the energy companies eventually face their day of reckoning.

When oil price collapse from $98 per barrel to $48 per barrel, the margins for the shale producers got hit. There is a grey minimum price of oil that the shale producers need to operate in and $48 was too low. If you lend money to them, you are a suspect to get into trouble, just like today.

It is Apollo Again.

One of the funds that were most exposed during that time was a fund by Apollo. Apollo is one of the larger alternative asset manager so naturally they are in the news today and also then…

They have a BDC (business development company) which is a private credit lending corporation that does private credit lending call Apollo Investment Corporation (AINV). AINV is listed as the ticker AINV.

This means that you can buy and sell the BDC. The value of the BDC is likely to be revalued not that frequently but perhaps like the property of REITs, which was revalued every half a year. The price of AINV will trade at a premium or discount to its NAV though.

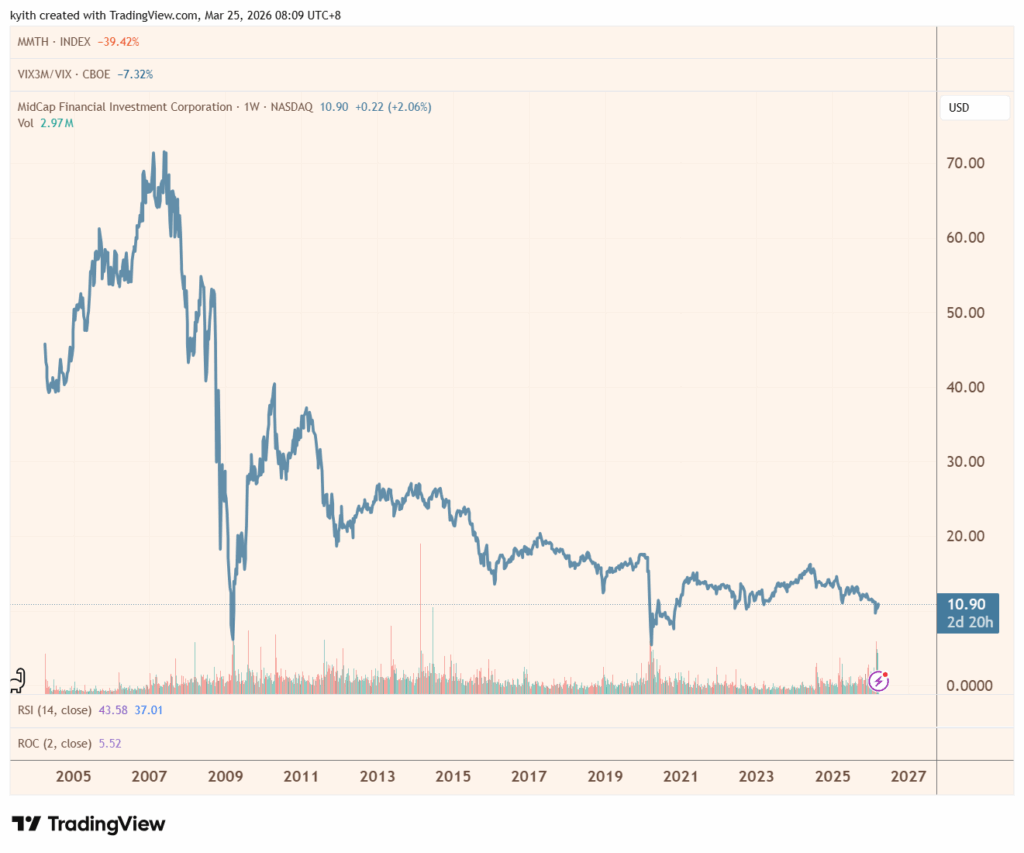

You can’t find AINV today not because it died during that energy price trauma but it is actually renamed to… MFIC or MidCap Financial Investment Corporation in 2022. The ticker is MFIC.

Here is how the price did all this time:

Looks bad huh.

The price decline from 2014 to 2016 is 48%.

Again volatility is not surprising for people who expect but I wonder if the investors was expecting this.

Here is the chart if we include the distribution:

It looks better at 200% return since Apr 2004. That is 5% p.a.

Looks like Global Aggregate Bond Returns.

What You Will Experience Again and Again.

MFIC has 17% of their portfolio lending exposed to oil and gas sector during the peak.

That experience allow us to have a glimpse of what may happen this time because situations doesn’t change.

This chart shows the three tracks:

- What actually happen in the oil and gas industry, to what happen to the BDC

- What the management say during the period.

- The fundamentals of the BDC.

The fundamental progression is that when interest cannot be paid, the ‘interest payment’ takes the form of PIK (payment in kind) or the lender will get more units when the loans get capitalized. This takes place in 2015.

Then the borrowers cannot pay back interest after more than 90 days it becomes non-accruals.

Eventually losses are realized.

You can see what the management say during the period.

- This is an opportunity to deploy more.

- Then it is attractive monetization even after the PIKs show up.

- Only in 2016 did they fire the CIO and conceded & realize the losses.

But it is Difficult to Help Clients, Prospects and Readers Understand.

Covenantlite helped us see that the discomfort that private credit investors faced today is not new.

And as we reviewed, their money was intact. Performances that maybe did not meet the expectations but still they would emerge with capital than a significant amount of their capital impaired.

But when faced with 13-16% distribution yield, what is difficult is to explain to them yearly how discomforting that can be. There will always be some sort of discomfort in investment:

- China being uninvestable.

- Hong Kong has changed.

- How the loan to value of REITs would explode up in 2008.

- How e-Commerce would impact REITs.

- How slow returning back from Covid would impact office.

- How Europe would just be shit for so long.

The similarity is its easy to conclude “I made a mistake”, or “This time is different”

The similarity may also be investors learning the wrong lessons.

- Trying to shun discomfort in investing, finding potential instruments or strategy that there is no discomfort.

- Every investment has it’s distress.

- Past human psychology rhymes. How management handles it may rhyme as well.

- You can get the idea right, but not the magnitude and timing over short or even long periods.

What Do the MFIC/AINV Investor in 2013 Actually Earn if They Remain Invested?

I thought I will provide some glimpse if you had invest in a potentially high yield private credit fund today, that mirrors the experience of MFIC/AINV in 2013.

Suppose someone puts in $10,000 in AINV in 2013. Here is the experience:

The investor in 2013 will be attracted to a 9% distribution yield. Eventually, the distribution did dip, and then rose more than 2013.

While the distribution looks good, the investor would have to consider the capital loss on the asset value. Actually I wonder if I calculated correctly since the investor would receive more units due to PIK

All in all, 2% p.a. returns after 12 years.

Probably not what they were expecting when they first invest in private credit.

But who do you blame?

Often, many investors self-psycho themselves that a 6-8% distribution is reasonable and it may be reasonable in reality.

Just that everything has a range of returns if you consider the total returns. Some will enjoy the 14% p.a. after 10 years.

Some will just get 2% p.a.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Fee-only Wealth Advisory Firm Providend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith’s current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

Purina Fancy Feast Gravy Lovers, Poultry & Beef Wet Cat Food, 3oz, 24-Pack | Variety Pack, grilled gourmet texture made with no artificial colors or preservatives, 100 percent complete and balanced

$22.86 (as of August 3, 2026 02:52 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Diet Coke Soda Soft Drink Bottles, 16.9 fl oz, 6 Pack | No sugar, no calories, 64 mg caffeine per bottle

$5.37 (as of August 3, 2026 02:51 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Apple AirPods Max 2 Wireless Over-Ear Headphones, Active Noise Cancellation, Adaptive Audio, Personalized Spatial Audio, Live Translation, Bluetooth Headphones for iPhone – Midnight | H2 chip with noise canceling and Bluetooth for audio recording, translation and music

$449.00 (as of August 3, 2026 03:06 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Automatic Dog Feeder - 8L/34 Cups Large Capacity Automatic Cat Food Dispenser with LCD Screen, Large Food Tray, Battery Operated, Timed Cat Feeder, Up to 50 Portions 6 Meals Per Day, Keeps Fresh

$55.99 (as of August 3, 2026 02:58 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Post Comment