Unlocking the Hidden Size Premium: Why Your Portfolio’s Junk is Killing Your Gains (And How to Fix It Fast)

They say the small cap premium is fading into the sunset—yet nearly 34% of the Daedalus Income portfolio rides on systematic active small cap funds. Sounds contradictory, right? The harsh academic truth often tossed around is that while small caps do throw more volatility your way, they don’t exactly pay off for that extra risk you’re taking. Since Rolf Banz first spotlighted size as a factor back in ’81, the Fama-French SMB factor has been clocking an average monthly spread of just 0.17% over six decades. Is that a bankable reward or just noise in the market?

Well, hold your horses. There’s fresh research catching some serious buzz. A November 2025 paper from Bridgeway Capital—championed by Larry Swedroe—suggests that if you cleverly strip out certain “noisy” stocks, this elusive premium stubbornly persists. But what kind of stocks muddy the waters? Think “Fallen Angels”—big names that fell from grace and shrank into small cap territory, dragging down portfolio returns—and the shiny new kids on the block like IPOs and SPACs, which historically don’t charm investors right out of the gate. Interestingly, even though some fret over missing out on the next big unicorn because companies stay private longer, stats show these new entrants don’t deliver in their debut year.

So, can savvy investors still squeeze value from small caps? Turns out, using a one- to three-year “small cap look back” filter and ditching those fresh-off-the-press listings may be the magic wand. Couple that with tuning out speculative “junk” as Clive Asness advocates, and we might just reignite the small cap fire. Strap in, because this journey into the underappreciated corners of the market could revolutionize how you see size as a factor in your portfolio.

img#mv-trellis-img-1::before{padding-top:66.6015625%; }img#mv-trellis-img-1{display:block;}img#mv-trellis-img-2::before{padding-top:54.628422425033%; }img#mv-trellis-img-2{display:block;}img#mv-trellis-img-3::before{padding-top:39.570164348925%; }img#mv-trellis-img-3{display:block;}img#mv-trellis-img-4::before{padding-top:56.99481865285%; }img#mv-trellis-img-4{display:block;}img#mv-trellis-img-5::before{padding-top:92.876712328767%; }img#mv-trellis-img-5{display:block;}img#mv-trellis-img-6::before{padding-top:35.175202156334%; }img#mv-trellis-img-6{display:block;}img#mv-trellis-img-7::before{padding-top:24.043715846995%; }img#mv-trellis-img-7{display:block;}

A lot of people say that the small cap premium is no more. For the record, almost 34% of Daedalus Income is in systematic active small cap funds.

What they academically means is that if you invest in small caps, they are more volatile, but they don’t really reward you for the additional volatility that you undertake by investing in them. Rolf Banz first identify size as a factor in 1981. The Fama-French SMB (Small companies return minus big companies return) monthly averages 0.17% over the past 60 years.

It doesn’t mean no return but that you are not rewarded. There are some distinctions there.

Larry Swedroe highlighted a recent November 2025 paper, I know what you did last summer – Persistent Small Size Delivers Superior return that explains if you eliminate some noisy stuff, the premium still exists. Larry’s commentary is over here.

The paper is written by the people at Bridgeway Capital, which is a small cap investment house.

The general idea is that you can look at the less significant stocks as made up of a few sub basket:

- “Fallen Angels” – stocks that used to be big but got beaten down. Imagine a stock that was a large, well-known company a year ago. Its business deteriorated, investors sold it off, and it shrank into small cap territory. It looks like a small cap now, but it carries all the baggage of a failing large company — weak momentum, declining fundamentals, distressed business. In the small value portfolio, stocks that were small the prior year returned 15.44% per year, while former large caps in the same small value category returned only 8.87% — a gap of more than 6.5 percentage points annually.

- New Entrants – IPOs, SPACs and Spin-offs.These are brand-new companies that have never proven themselves in the market. In five of the six size-and-value portfolio combinations, new entrants underperformed their counterparts, often by 2% to nearly 6% per year. This is consistent with decades of research showing that IPOs tend to disappoint investors for years after listing.

It is quite interesting in that some of us worry that we missed out on new companies because they stay private for longer, but quantitatively they are not so good in the the year they got listed.

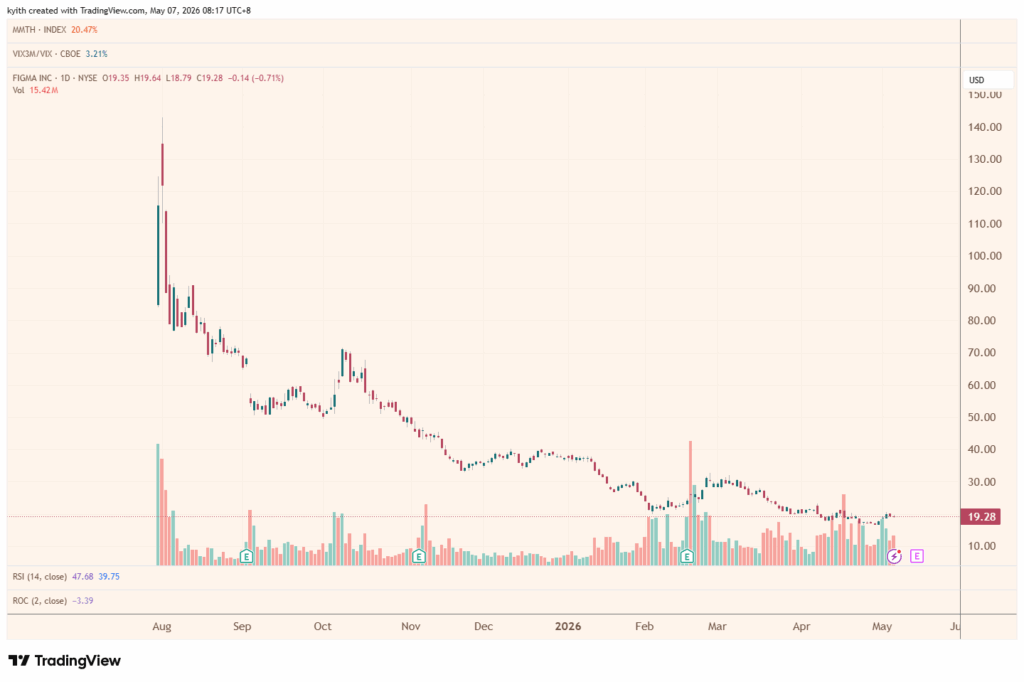

A good example may be Figma. Even after falling the market cap is 10 billion, which is outside of small cap category. I guess what we missed harvesting is the returns in the growth phase that we might harvest had they been public. (Then again very hard to say. If Figma was listed then, would we forced them to not grow so much but be profitable?)

Bridgeway’s research shows that if you eliminate these two groups, your returns would be much higher.

But how do you eliminate them?

- Only consider the small caps if they were still small one year ago (1-year look back). This means if they weren’t small, don’t invest in them.

- If they are small even 2 or 3 years ago, even better!

- Did they just IPO, SPAC or spun off? If yes eliminate them.

The chart above shows how long these small cap remain as small caps. 1 year look back is that they been small cap for at least 1 year and 3 year is they been small for 3 years.

Apparently longer look back has higher return.

This Has Not Include any Factor Tilting Yet

This research is solely focus on just size but they do look into the factor regression analysis.

Larry layers on and explain that if we combine this, together with excluding the most shitty stocks (speculative “junk”) that AQR’s Clive Asness talked about in his paper Size matters, if you control your junk.

In a way, you don’t have to find the most profitable. You would just have to eliminate the not profitable and you can see a different.

By marrying these two, the research shows you can get good returns that can potentially improve returns.

We illustrate some of Clive Asness’ 2018 research. SMBQ long quality and short the low quality in the small company space. That almost 5% is the premium and if you add the grew Market bar, which stands for the equity risk premium, you get a return of about 10.8%.

There are certain 20-year periods where the small cap does not perform so well and the research shows that if you adjust for quality, the performance is actually better.

This table shows the monthly excess return (not return) over risk-free rate, bucket by size and quality.

If you are crafting a portfolio, where would you cluster or target the securities? in the top left corner.

That is what AVGS (Avantis Global Small Cap Value UCITS ETF) and DDGT (Dimensional Global Targeted Value UCITS ETF) tries to do.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

I break down my resources according to these topics:

- All my personal notes about how my philosophy behind my own money and how I manage it.

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I used to work doing research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

- Havend – Where I currently work. We wish to deliver commission-based insurance advice in a better way.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Fee-only Wealth Advisory Firm Providend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith’s current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

Dog Allergy Chews, Dog Allergy Relief for Itching Skin, Paw Licking, Yeast Relief, Hot Spots, Itchy Ears & Seasonal Allergies, Immune Support– with Colostrum, Probiotics – Chicken Flavor (200ct)

(as of July 16, 2026 02:50 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Apple AirPods 4 Wireless Earbuds, Bluetooth Headphones, Personalized Spatial Audio, Sweat and Water Resistant, USB-C Charging Case, H2 Chip, Up to 30 Hours of Battery Life, Effortless Setup for iPhone

(as of July 16, 2026 02:54 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Dog Cone Collar to Stop Licking, Soft Mesh Recovery Collar After Surgery with Liner, Elizabeth Cone Alternative for Medium and Large Dogs, for Surgery, Spay, Neuter, Wound Care,L,Black

(as of July 16, 2026 02:50 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Flea and Tick Prevention for Cats & Kittens, Topical Cat Flea and Tick Treatment – Fast-Acting & Long-Lasting 6-Dose Supply

(as of July 16, 2026 02:50 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Post Comment